TODAY’S S&P 500 SET-UP – March 19, 2013

As we look at today's setup for the S&P 500, the range is 27 points or 0.84% downside to 1539 and 0.90% upside to 1566.

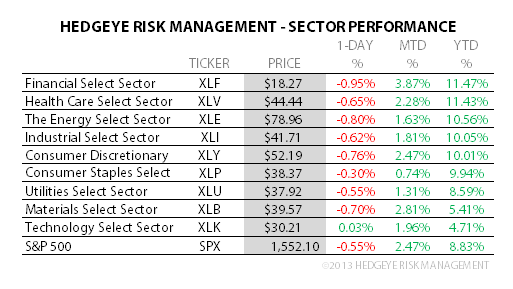

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.70 from 1.71

- VIX closed at 13.36 1 day percent change of 18.23%

MACRO DATA POINTS (Bloomberg Estimates):

- Federal Reserve’s FOMC starts two-day meeting

- Lagarde, Weidmann, Schaeuble speak at Frankfurt Finance Summit

- ESM to sell as much as EU2b 182D bills

- 7:45am: ICSC weekly sales

- 8:30am: Housing Starts, Feb., est. 915k (prior 890k)

- 8:30am: Housing Starts M/m, Feb., est. 2.8% (prior -8.5%)

- 8:30am: Building Permits, Feb., est. 925k (prior 904k)

- 8:30am: Building Permits M/m, Feb., est. 2.3% (prior 1.8%)

- 8:55am: Johnson/Redbook weekly sales

- 11am: Fed to purchase $2.75b-$3.50b notes in 2020-2023 sector

- 11:30am: U.S. Treasury to sell 4W bills

- 4:30pm: API Energy Inventories

GOVERNMENT:

- Obama departs on trip to Israel, Middle East

- VP Biden in Rome to attend installation of Pope Francis

- Senate Armed Svcs Cmte hearing on authorization requests for FY2014, Future Years Defense Program, 9:30am

- US Airways CEO Douglas Parker, AMR CEO Thomas Horton, Consumers Union consultant Diana Moss testify on US Airways-American Airlines merger at Senate Judiciary Cmte panel, 10am

- House Ways and Means Cmte holds hearing on tax laws, provisions affecting state, local govts, 10am

- House Financial Svcs Cmte hears from Fed Housing Finance Agency on GSE conservatorships, 10am

- Senate Banking, Housing and Urban Affairs Cmte votes on Cordray for CFPB, White for SEC, 10am

- Treasury’s Lew in China for talks w/ President Xi Jinping

- Senate Finance Cmte holds hearing on President Obama’s trade agenda, 10:30am

- DOJ’s Elana Tyrangiel, Google’s Richard Salgado testify before House Judiciary hearing on Electronic Communications Privacy Act, 10am

WHAT TO WATCH

- Blackstone said to mull outbidding Silver Lake for Dell LBO

- Samsung preparing wristwatch as it races Apple for new market

- Ryanair places $15.6b order for 175 Boeing 737-800 planes

- BlackRock to cut ~300 jobs as Fink extends reorganization

- JPMorgan Chase won’t face revived suit over silver manipulation

- Citigroup to pay $730m in crisis bond-lawsuit settlement

- Home construction starts in U.S. probably climbed in Feb.

- BofA said to cut head of equities role in Australia

- Affymax fires 75% of workforce; considers sale, bankruptcy

- European Feb. car sales decline 10% on deepening recession

- BMW forecasts unchanged 2013 pretax profit on Europe mkt drop

- Boeing avoids strike threat; technical workers accept contract

- Weight Watchers said to set rate on $2.4b bank financing

- NPS buys back global Gattex rights from Takeda for $50m

- Corvex asks judge to halt arbitration in CommonWealth suit

- NFL, Providence plan to have ~$300m to invest in start-ups: WSJ

EARNINGS:

- DSW (DSW) 7am, $0.72

- Rentech Nitrogen Partners (RNF) 7am, $0.55

- FactSet Research Systems (FDS) 7am, $1.24

- Alimentation Couche Tard (ATD/B CN) 11am, $0.89

- Francesca’s Holdings (FRAN) 4:01pm, $0.30

- Adobe Systems (ADBE) 4:03pm, $0.31

- Williams-Sonoma (WSM) 4:05pm, $1.29

- Cintas (CTAS) 4:15pm, $0.62

- Tourmaline Oil (TOU CN) 5pm, C$0.06

- Franco-Nevada (FNV CN) Aft-mkt, $0.34

- Element Financial (EFN CN) Aft-mkt, C$0.07

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Crude Falls to Shrink Premium to WTI Before Cyprus Vote

- Wheat Crop Seen Near Record as U.S. Drought Recedes: Commodities

- Indonesia, Third-Biggest Cocoa Grower, Poised to Turn Net Buyer

- Copper Swings Between Gains and Drops Before U.S. Housing Data

- Soybeans Advance on Speculation U.S. Farmers to Withhold Crops

- Gold Falls After Three-Day Gain as Stronger Dollar Curbs Demand

- Robusta Coffee Falls as Vietnam Crop Concern May Be ‘Premature’

- Rio Tinto Sees Supply Weighing on Iron Ore Prices in Second Half

- Top Rubber Producers Must Control Output, Indonesian Group Says

- Consumers to Pay $13 Billion Price as Ethanol Upends Refiners

- SPDR Gold Trust Holdings Decline to Lowest Level Since July 2011

- Billionaire Fredriksen Almost Doubles Ship Orders Amid Glut

- Crude Inventories Climb a Ninth Week in Survey: Energy Markets

- Thailand to Propose Extending Rubber Export Cut Another Year

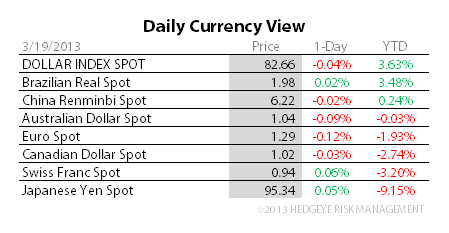

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team