We think the market’s reaction to Cyrus’ bailout is overdone and that these ‘crisis’ conditions will be short lived.

A quick update on the latest development is that parliament has delayed a scheduled vote today on the proposed bailout, namely on the levying of a one-time tax of 9.9% on Cypriot bank deposits of more than €100K and a tax of 6.75% on smaller deposits, until tomorrow.

Internally there’s much pushback on the scheme as the country’s banking system is tied with political and banking corruption that allows a home for Russian money laundering. It is therefore playing out on the streets that “oligarchs” banking in Cyprus should pay disproportionately more versus average deposit holders, if the latter should play at all.

Externally, the move to tax deposit holders for bailout packages (versus for example sovereign bond holders) sets a dangerous precedent that throws fear across Eurozone deposit holders. We expect Eurocrats to rhetorically smooth over the deposit levy and signal that Cyprus is a unique and extreme case given the inner workings of its corrupt banking system.

Note that today is a holiday in Cyprus and there’s talk that a bank holiday will be extended at least to Wednesday to prevent capital flight as the terms around a €10B bailout are voted on this week. This morning the WSJ cited an official that said the new proposal will allow depositors with less than €100K to be taxed at 3%, savers with €100K-€500K taxed at 10%, and those with over €500K taxed at 15%. While we cannot know the accuracy of this citation, it appears likely that the government will tax higher deposits at a higher rate to go after large Russian deposit holders. Depending on the crafting of the levy it would also seem probable that temporary restrictive measure may have to be put in place to prevent the flight of deposits to other countries.

Here are some take-aways to consider as the media runs hard with this story.

- It has been clear for many months that Cyprus would need external assistance to repair the country’s finances, a country with a banking system some eight times larger than the economy.

- Had a flat €17B bailout package been crafted, we would not have expected such a negative market move. We think the market will move past this development as terms around the deposit levy are likely mitigated for smaller deposit holders and the EU PR machine assures Pan-Europe that its deposits would not be considered for future bailouts.

- While Chancellor Merkel was hoping to delay the bailout until after her election in September, this deal is a political win for her. Why?

- Having Cyprus cover a portion of the bailout (~€5.8B) and a loan reduced to €10B instead of an estimated €17B looks good for Merkel’s constituency as Germany is writing the biggest portion of the bailout checks. Further, a bailout of Cyprus now allows the issue to be swept under the rug well before German elections in September.

- Even with an economy the size of less than one half a percent of the 17 nation Eurozone, Eurocrats are incentivized to throw money at the problem to limit fall out. The experience of Greece and Portugal in particular shows that even puny economies can impact economic sentiment. Eurocrats’ biggest incentive remains their own jobs -- they'll continue to squash any fears of contagion with bailout band-aids.

- Cyprus represents, to many, a huge flaw in the Eurozone system – allowing countries like Cyprus to enter the Eurozone in the first place. Again we expect the play from them to be throwing good money at bad, with initial attempts of setting forth banking reforms to limit corruption.

- Russian President Vladimir Putin has criticized the levy saying that the decision, should it be made, would be unfair, unprofessional and dangerous. Maybe Putin has some money in Cyprus too?? It is estimated that Russia has ~ €60B of total exposure to Cyprus on a ~€24B economy. So there’s a real fear of Russians pulling their money and the negative windfall it would have on the banking system and economy. This further suggests that restrictive measure will have to be placed on deposits to prevent flight.

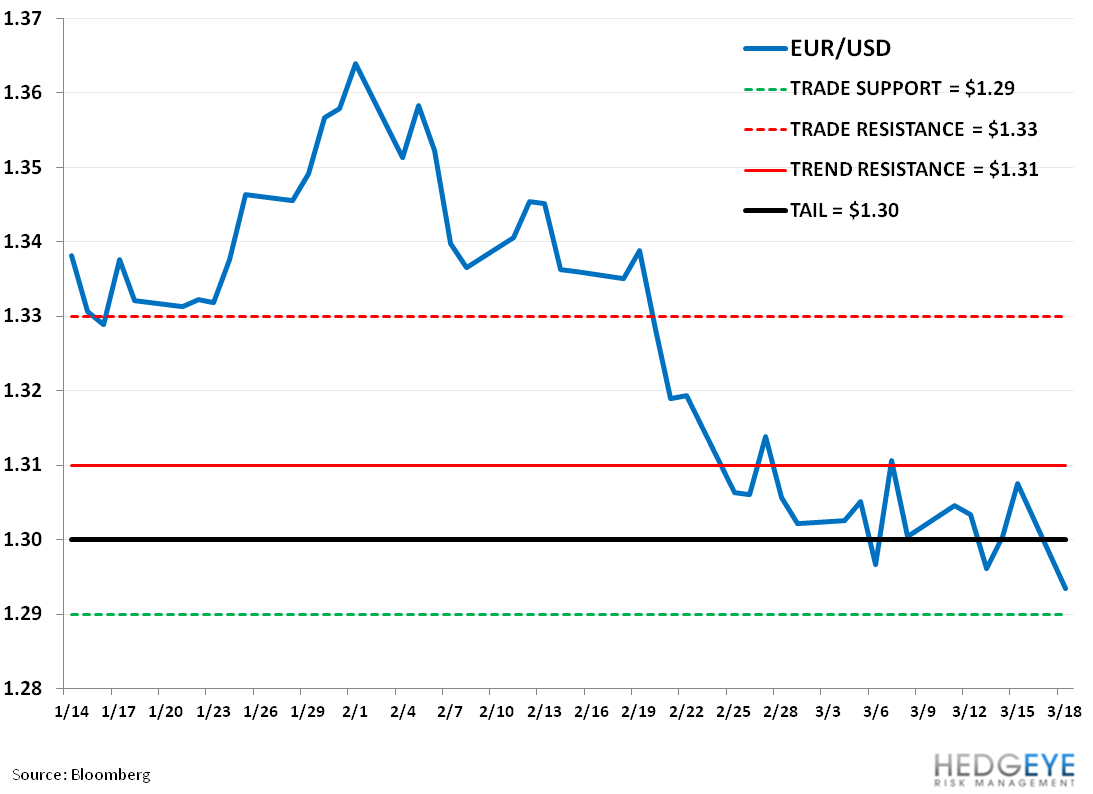

While we think the market will move past Cyprus over the short term, this event along with the Italian elections provide good ammo to put pressure on the EUR/USD.

Nothing like another good crisis to stir up the markets!