Key Takeaways:

* We'll buy fear for now. It remains to be seen what impact Cyprus will have on EU deposit perceptions. We think the lesson of the last 15 months has been that the ECB will do everything in its power to prevent interbank counterparty problems, reinforcing the too-big-to-fail dynamic among Europe's largest banks. Deposit safety fear, should it grow, should ultimately benefit the large EU banks as they'll be seen as relative safe havens. This should, in turn, minimize counterparty risk for the U.S. global banks seen as at risk from Cyprus contagion woes. The ECB's success thus far is evident in the move from 100 bps to 13 bps in Euribor-OIS, the measure of European interbank counterparty risk. While we would expect a nominal backup in this key risk indicator, we'll be focused on whether this Cyprus news results in a sustained rise in the Euribor-OIS spread over the coming weeks.

* XLF Macro Quantitative Setup – Based on this morning's open, the XLF is sitting just above trade support of $18.23.

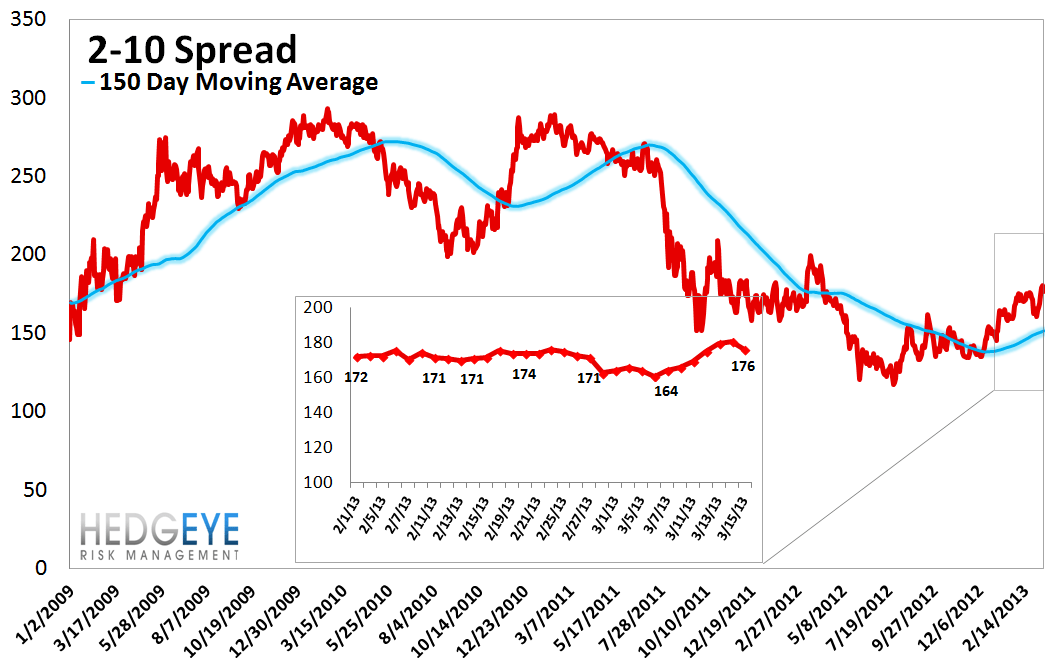

* 2-10 Spread – Last week the 2-10 spread widened 10 bps to 176 bps.

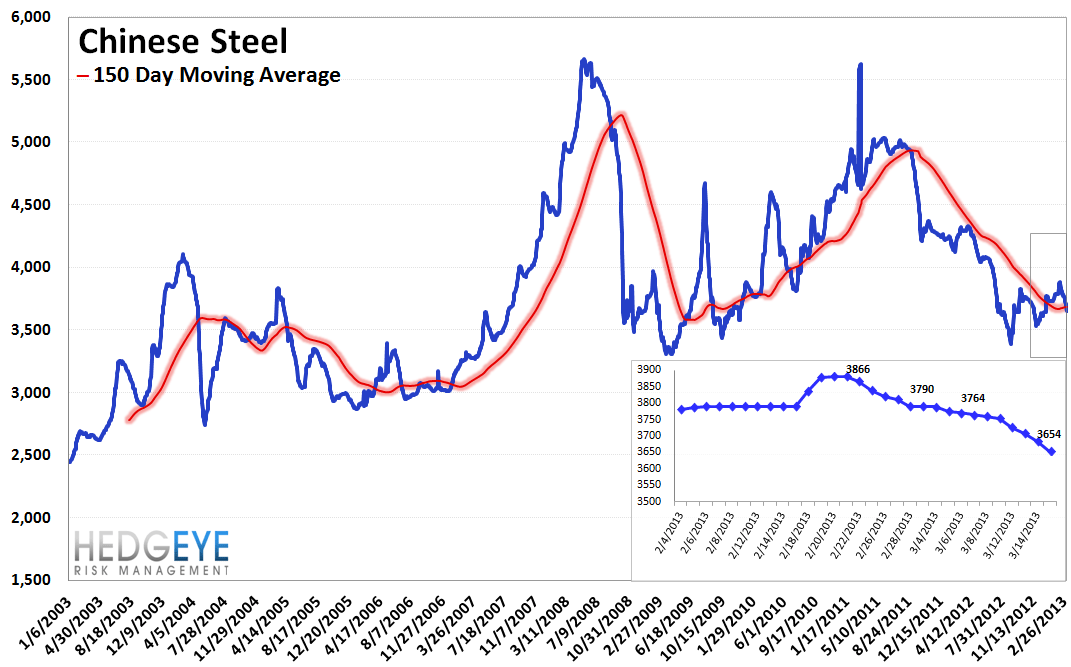

* Chinese Steel – Steel prices in China fell 2.8% last week, or 105 yuan/ton, to 3654 yuan/ton. This brings the month-over-month change to -3.6%. Weakening Chinese steel prices are reflecting slowing demand for new construction.

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 6 of 12 improved / 2 out of 12 worsened / 5 of 12 unchanged

• Intermediate-term(WoW): Positive / 6 of 12 improved / 2 out of 12 worsened / 5 of 12 unchanged

• Long-term(WoW): Positive / 11 of 12 improved / 0 out of 12 worsened / 2 of 12 unchanged

1. U.S. Financial CDS - Large cap U.S. financials were notably tighter last week. In fact, it was a perfect week in that 27 out of 27 institutions improved week-over-week. We'll see how much of those gains are retraced this week on Cyprus.

Tightened the most WoW: C, AGO, MS

Tightened the least WoW: PRU, UNM, ALL

Tightened the most WoW: MTG, RDN, MBI

Widened the most/ tightened the least MoM: AON, MMC, PRU

2. European Financial CDS - Unfortunately, these quotes are all as of Friday night. Clearly, that renders them rather stale. If we rewind to before Cyprus, what we see is a very uneventful week (last week) for EU financials across the board. Italian banks were slightly wider WoW, but otherwise it was extremely quiet.

3. Asian Financial CDS - Last week was uneventful for Asian banks, with most narrowly tighter. The biggest move of the week came from Nomura, which tightened by 8 bps.

4. Sovereign CDS – The European periphery continues to move wider, while the core tightens further. The U.S., Germany and France were all tighter last week, while Spain, Italy, Ireland and Japan all widened.

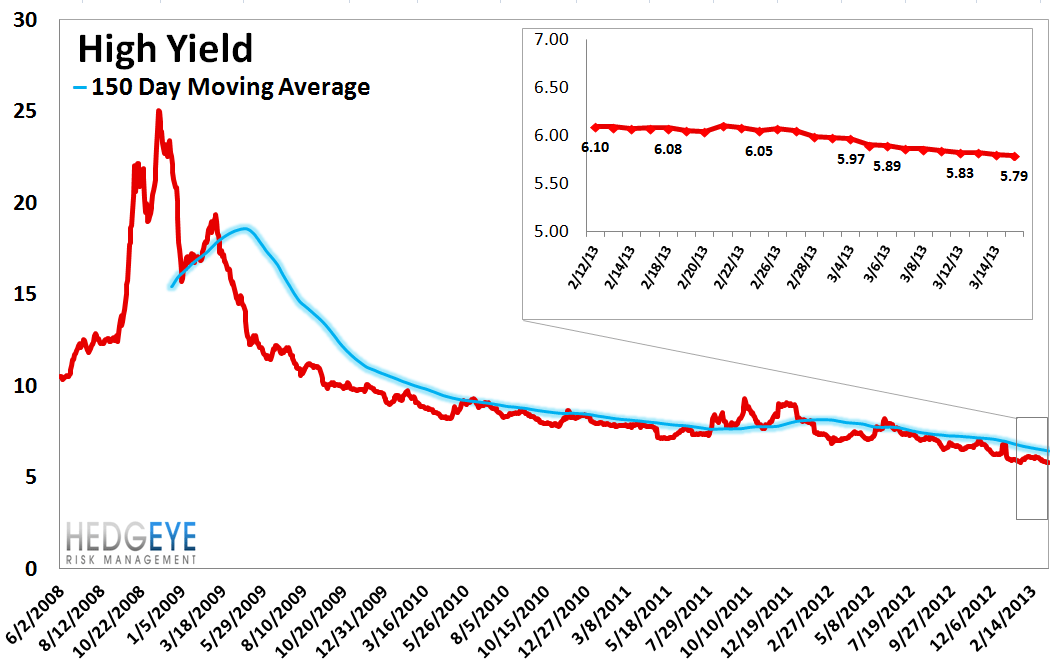

5. High Yield (YTM) Monitor – High Yield rates fell 6.7 bps last week, ending the week at 5.79% versus 5.86% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 5.4 points last week, ending at 1781.69.

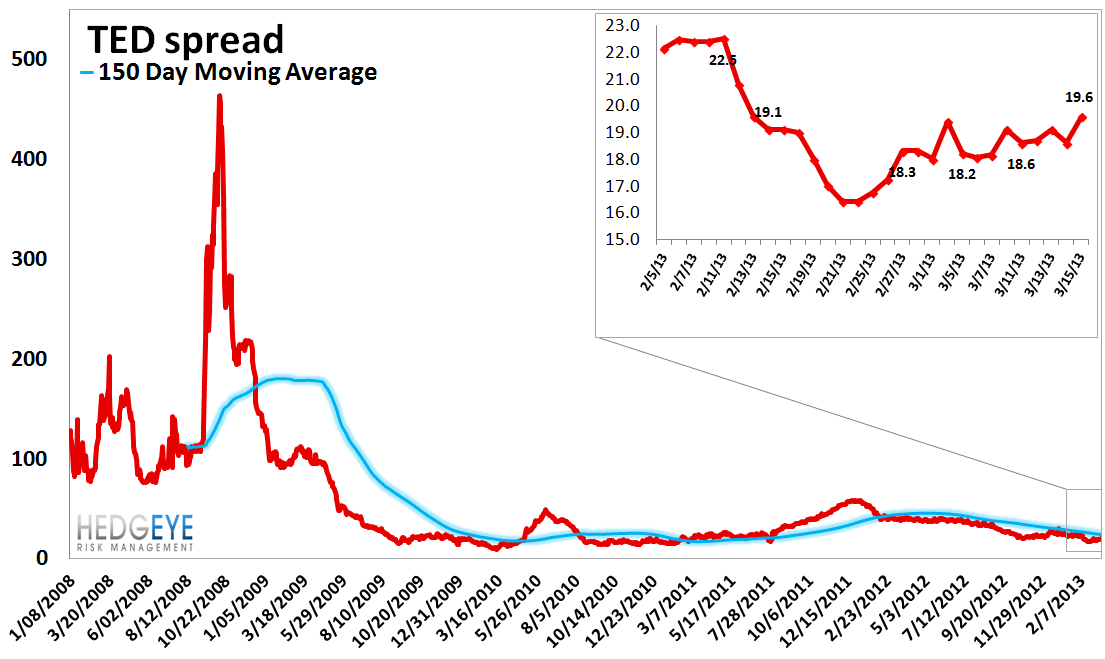

7. TED Spread Monitor – The TED spread rose 0.5 basis points last week, ending the week at 19.61 bps this week versus last week’s print of 19.11 bps.

8. Journal of Commerce Commodity Price Index – The JOC index rose 2.4 points, ending the week at 9.86 versus 7.5 the prior week.

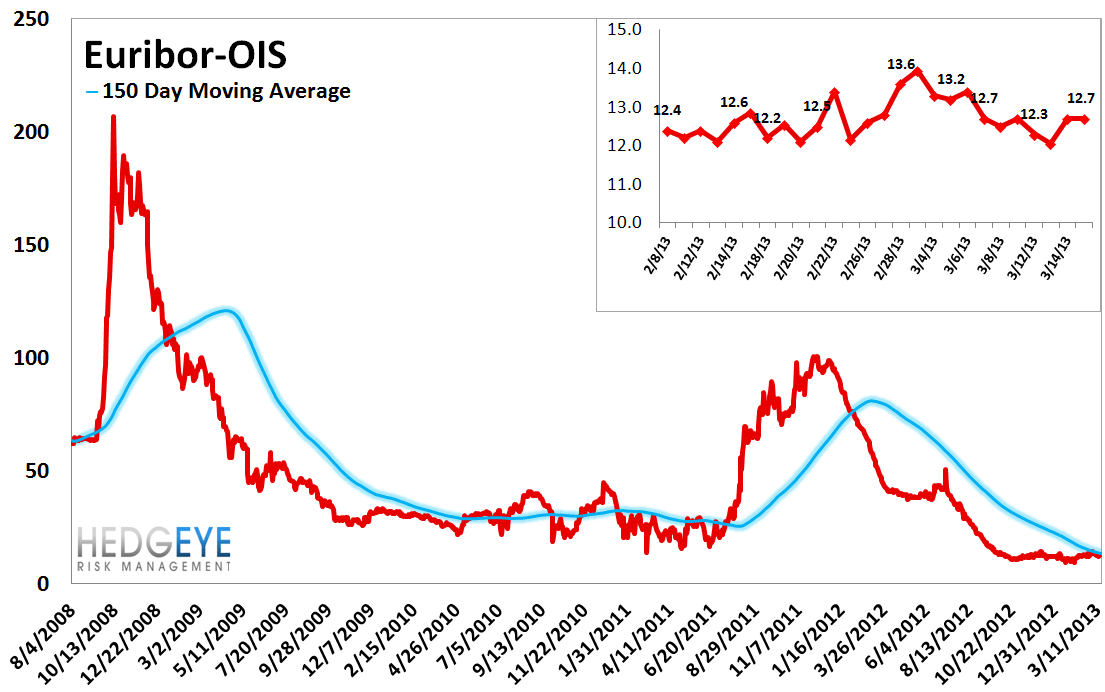

9. Euribor-OIS Spread – As of Friday's close, the The Euribor-OIS spread was flat week-over-week at 13 bps. We'll stay tuned for an update as of the close today. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

10. ECB Liquidity Recourse to the Deposit Facility – Deposits at the ECB continued to decline in the latest week, albeit this data is through Friday. It remains to be seen how the Cyprus deposit tax will impact things. The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

11. Markit MCDX Index Monitor – Last week spreads were narrowly tighter, ending the week at 88.2 bps versus 91 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China fell 2.8% last week, or 105 yuan/ton, to 3654 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread widened to 176 bps, 10 bps wider than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Based on this morning's open, the XLF is sitting just above trade support of $18.23.

Joshua Steiner, CFA