One would be hard pressed to find a segment of the consumer economy performing worse than regional gaming. The stocks have been a different story.

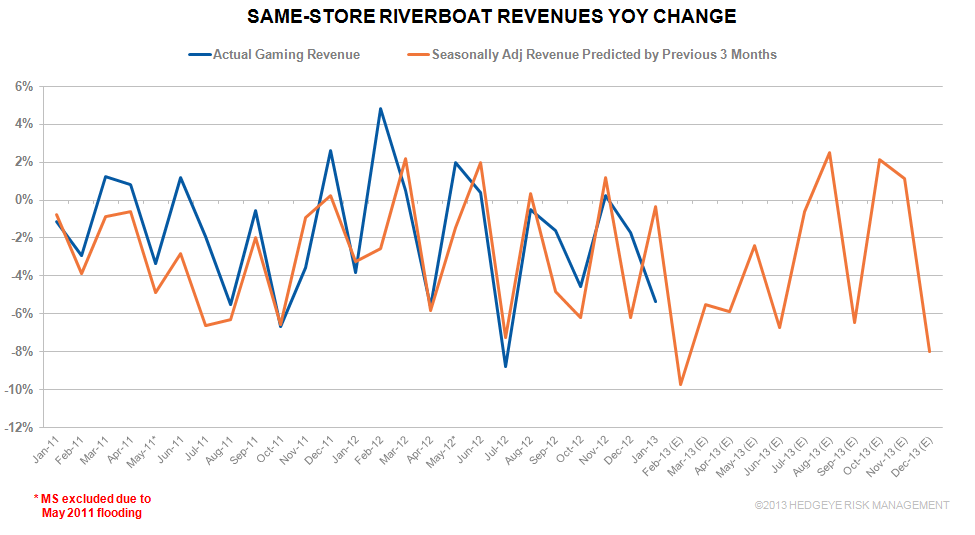

Mature regional gaming markets should post a combined gross gaming revenues (GGR) decline of close to 10% in February (still waiting on Louisiana/Mississippi to report). This ugly performance follows a very disappointing 6% decline in January. January was even more surprising based on our model which predicts monthly GGR based on sequential trends adjusted for seasonality and other factors such as the calendar, weather, and one-time events. As can be seen in the following chart, January should’ve been close to flat YoY.

It’s not like the companies can make up for it in margin; costs have already been cut to the bone and the casinos are highly fixed cost businesses. Combine the operating leverage with very high financial leverage and the stocks should be getting creamed in a declining demand environment, right? The chart below tells a different story. Regional gaming stocks have outperformed the market since mid-November. So what gives?

For the most part, it comes down to corporate finance:

- PENN announced a conversion to a REIT on 11/16/13. Through the real estate lens, all regional stocks suddenly looked cheap.

- PNK announced the agreement to acquire ASCA which boosted both stocks. Nothing like M&A to get investors excited.

- BYD reached an agreement to sell the Echelon project to Genting and Jai Lai Dania, allowing the company to de-lever by jettisoning non-EBITDA producing assets. The transactions lowered the stock’s valuation considerably.

The question is what happens now. We think the rest of 2013 will mark the return of focus on fundamentals. This will not be good for the stocks. Our EBITDA estimates for Q1 and 2013 fall below the Street for each regional company with the surprising exception of BYD. We’re in-line with BYD probably because everyone hates the company and it was the most recent to announce earnings.

- PNK/ASCA – PNK looks the most vulnerable because they are doubling down on regional gaming with added leverage. The upside of the deal – huge cash flow and EPS accretion – has already been recognized in the stock. ASCA’s properties were among the best run in the industry so operating upside is limited. We think investors may be disappointed with corporate cost reductions since ASCA allocated a significant amount of property-related costs to corporate which contributed to industry leading property margins but also industry leading corporate costs as a percent of revenues. PNK’s valuation of 7.6x next year’s EV/EBITDA doesn’t leave a lot of room for upside. Investors may be increasingly uncomfortable with post deal leverage of 6.6x in this type of environment.

- PENN – At this point, we think the stock is fairly valued considering numbers still need to come down and analysts seem to be giving an aggressive multiple of 6-7x EBITDA for OpCo. Offsetting those two factors is a fairly low cap rate ascribed to the REIT. We think that the value of the REIT will rise as real estate investors become comfortable with the concept of a gaming REIT. We’ll stay on the sidelines until the Street reduces estimates.

- BYD – With the sale of Dania and the Echelon project factored in, BYD’s EV/EBITDA multiple next year declines to an industry low of 6x. More importantly, we think the Street actually has the numbers right for Q1 and 2013. There is no stock in our universe with worse investor sentiment (not even CCL) than BYD. Sell side ratings are almost universally Holds and Sells. Assuming we’re right on the numbers, a simple half turn in the multiple represents a 50% move in the stock price. Just meeting expectations should get BYD there.