This note was originally published March 15, 2013 at 07:55 in Early Look

“Study history, study history. In history lies all the secrets of statecraft.”

-Winston Churchill

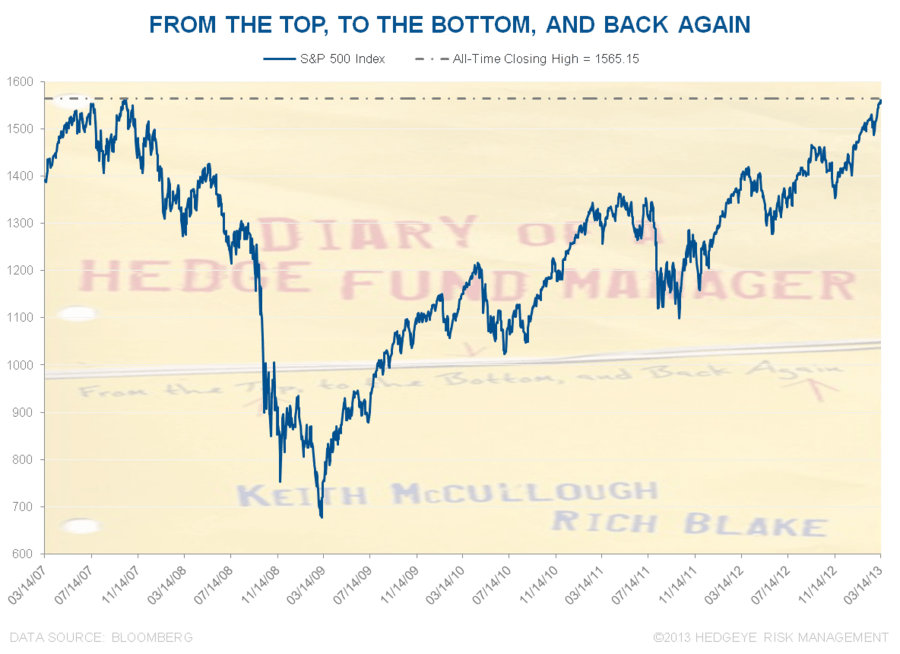

The last time we hit these levels in the SP500 was the worst time of my career. It was October 2007, and most of my big (bearish) macro ideas weren’t working yet. Our credit guys were blowing up our fund – and the performance pressure at Carlyle was palatable.

I’ll never forget. Whenever the market tells me I am wrong, I remind myself what it felt like to stay wrong for months at a time. It’s not personal. It’s just the score – and you have to find it within yourself to either change your mind, or live with the consequences.

Hedgeye’s history starts from my professional lows (I got fired in November 2007). I’ve been writing about every market move I make since. Rich Blake and I wrote a book in 2010 called Diary of a Hedge Fund Manager - From the Top, to the Bottom, and Back Again. Oh how history sides with charts that look just like that. The US stock market is back again, and (thank God) this time I didn’t get run over.

Back to the Global Macro Grind…

“History will assign a neat set of circumstances for this past crash – the popping of the housing bubble, one created in large part by the US government-sponsored entities, Freddie and Fannie, exacerbated by an overindulgent credit derivatives market. Sounds right.”

“If history has proven anything, it’s that patterns repeat, again and again. Greed takes over and the self-fulfilling groupthink of the herd trumps rational process.” (pages 175-176, Diary Of a Hedge Fund Manager)

Rich and I wrote that then, but after 5 long years of making mistakes, I’m not sure what “rational” means. Isn’t rational what we call something after it plays out in full? It’s very rear-view looking.

Here’s what I used to think was rational:

- Every positioning that was working

Here’s what I thought was irrational:

- Every position that wasn’t working

I thought wrong.

Now that every mistake I make is made out loud for everyone to see (over 2,000 long/short positions #timestamped since 2008). What’s rational has a new definition. It’s called the score. And my team is accountable to you on that front, every day.

I’ve been on the road seeing a lot of clients so far this year. That really humbles me. Sitting across the table from money managers gives me a keen sense of performance pressures, positioning anxieties - really all the things that used to dominate my day. This is an extremely difficult profession to perform in over long periods of time. That’s why we call it the grind.

Today, my day isn’t like it was when the SP500 was last testing 1565. Today, I have many different pressures. I have my wife and kids to provide for. I have 46 employees and their families that I am responsible for – and I have you.

So keeping it shorter today, I just wanted to thank you – every one of you who has taken the time to read my rants for the last half decade; every one of you who is a new relationship; everyone who has both challenged and supported me in making this happen.

While markets may not always seem “rational” relative to your positioning, you can always believe in some very core principles in sports, business, and in life. It’s important to define what’s rational to you on that front. Then surround yourself with more of that.

Our founding principles: Transparency, Accountability, and Trust. These aren’t principles I give lip-service to. They aren’t the secret to modern day #PoliticalClass statecraft either. They are a rational recipe for a team’s long-term success.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST10yr Yield, VIX, Russell2000, and the SP500 are now $1568-1595, $107.98-110.04, $82.05-83.12, 94.12-97.26, 1.99-2.11%, 10.72-13.41, 937-959, and 1546-1569, respectively.

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer