In preparation for CCL's F1Q 2013 earnings release tomorrow, we’ve put together the recent pertinent forward looking company commentary.

CARNIVAL DREAM POWER PROBLEMS 3/14/2013

CARNIVAL TRIUMPH FIRE 2/10/2013

CARNIVAL CORPORATION REPORTS FINANCIAL IMPACT OF VOYAGE DISRUPTIONS IN THE 1H 2013 2/13/2013

- $0.08-$0.10 reduction in EPS

CARNIVAL RE-ESTABLISHES $1 BILLION REPURCHASE PROGRAM; DECLARES QUARTERLY DIVIDEND 1/17/2013

- Renewed its authorization for the repurchase of up to $1 billion of its common stock and declared a quarterly dividend of $0.25 per share.

- The company has repurchased two million shares of Carnival Corporation common stock valued at $78 million since the start of fiscal 2013

- The board approved a record date for the quarterly dividend of February 22, 2013 with a payment date of March 15, 2013.

YOUTUBE FROM F4Q 2012 CONFERENCE CALL

- "There are a few unique items in 2013 that will be difficult to totally overcome which will push our unit costs higher. To begin with, we are expecting that Costa will fill their ships in 2013, which will lead to higher food and other unit costs associated with this higher occupancy. Also, as I have previously indicated, our insurance costs will be higher in 2013. Furthermore, we are anticipating a charge from a closed pension plan for certain British officers. Finally, we are investing in new market development initiatives in Japan, China and Australia including deployment decisions not yet announced. These unique factors alone in 2013 will drive up unit costs 2%."

- "We expect in 2013 to use 24% less fuel per berth than we did in 2005....Just to be clear, the price of Brent was just under $110 a barrel when we determined our guidance."

- "A 10% change in the current price of fuel excluding the impact of fuel derivatives represents a $0.30 per share impact for the full year. Please note that the impact of a 10% change obviously moves along with the price of fuel. Just to be clear, the price of Brent was just under $110 a barrel when we determined our guidance."

- "For 2013, our protection begins when the price of Brent goes above $127 per barrel, and we begin to pay on our fuel derivatives when the price of Brent falls below $100 per barrel. With respect to FX movement, a 10% change in all relevant currencies related to the U.S. dollar would impact our P&L by approximately $158 million or $0.20 a share for the full year."

- "We have two ships scheduled for delivery in 2013. The first is the 2,200 little berth, AID Astella, which will be delivered in March to our very successful AIDA brand in the German-speaking market. And the next one will be the new generation Royal Princess with 3,600 lower berths, which will be delivered sometime towards the end of May. These two ships together with three ships delivered during this past year 2012 will drive a 3.6% increase in cruise capacity in 2013."

- "In Europe where we have a strong market presence, we anticipate continuing struggling economies during 2013, much as we experienced during 2012."

- "In April 2013, Princess Cruises will introduce the Sun Princess to the Japanese market, and we have recently established a Carnival Japan sales and reservations office in Tokyo. With the announcement of the Sun Princess Japanese deployment, response from the market in Japan has been very strong and early signs are quite encouraging."

- "In 2013, operating plan forecasts a nice increase in Costa Asia's profitability."

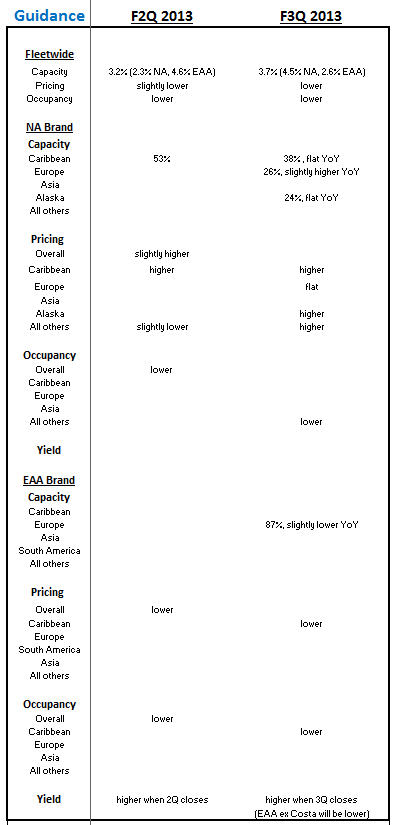

- "During the last 13 weeks, fleet-wide bookings and pricing excluding Costa for the first three quarters of 2013, are at the same levels against the very strong booking volumes we experienced last year. Not surprisingly, Costa's pricing is still running behind last year's pricing, but we expect that to change once we lap January of 2012."

- "For our North American brands, during the 13-week period, bookings are running slightly behind with slightly higher pricing. For EAA brands, the bookings excluding Costa are running at higher levels than last year at lower pricing. We are encouraged by the recent North American booking pattern, especially given consumer distraction from the elections and post-election consumer nervousness about the pending fiscal cliff, and the recent pattern excludes some negative impact on bookings from the Northeast resulting from the Hurricane Sandy. So we are hopeful that once the fiscal cliff issue is resolved and we get into January, and the wave season begins, consumers will start to turn their attention getting on with their lives and booking their cruise vacations."

- "For the full year, from a revenue yield forecast standpoint, we are forecasting a constant currency increase in yield in the range of 1% to 2%. North American revenue yields are forecasted to come in higher year-over-year, EAA yields are forecasted to be higher when we include Costa, which will have easier comps versus last year, but excluding Costa, EAA yields are forecasted to be lower on a year-over-year basis."

- "Recovery of Costa is not a one-year issue, it's going to be multiple years; and we're forecasting a recovery of about half the yield deterioration, that's one item. Two is it's important to understand that we don't cycle through this until the second quarter because the first quarter was done, and the timing of first quarter in this instant versus competitors is very important because it did happen in the middle of our first quarter when the first quarter was done."

- "If you start the first quarter being down in pricing for the Costa brand then the recovery in the back half for the year is a little bit heavier pricing."

- "Caribbean looks strong now."

- [Yield] "We do expect the second quarter to be up, but when you look at the full year guidance of 1% to 2%, that does imply let's say 2% to 3% yield increase in the back half of the year."

- "We're starting to have – to see some effect of a weaker economy both in the UK and Germany, which we really didn't see a whole lot in 2012. So if there's anything different, I'd say we're a little bit more concerned. Although those brands are performing well, we are a little bit concerned going forward as the booking curve has tightened in those countries."

- "The other thing that I haven't seen a lot of focus on is some of our competitors have talked about reducing capacity in Europe. But in reality, our two largest competitors together have increased the Northern Europe capacity by over 20% next year. So, the Northern Europe itineraries have tended to be the highest yielding itineraries in the European market, and that capacity increase will be interesting to see how that all plays out."

- "All of our capacity increase in Europe next year is in Germany."

- [2013 cost assumption] "And if you take into account the prior year's ship incident cost, we would've been flat year-over-year."

- "Our onboard trend overall around the globe for 2013 is very similar to 2012. 2012 we were up like a little over 2% and our guidance for 2013 is in the similar range with increases in all the major categories. Our operating companies have done a great job with some new initiatives and so we're expecting those to be driven higher as well."