This note was originally published March 12, 2013 at 18:27 in Consumer Staples

Looking Back to Look Forward

We are taking a page from our prior experience as a dedicated tobacco analyst, recalling the days when litigation threatened the domestic tobacco business at then Altria (combined international and domestic tobacco as well as Kraft Foods).

The argument was that at some point the market was applying a negative value to the domestic business and that even in a worst case scenario (a bankrupting decision against the U.S. business), the value of the other entities would be preserved on the other side of the corporate veil. Further, structural differences in the legal systems outside the United States made the export of any bankrupting litigation unlikely, preserving the multiple associated with the international assets.

We see the situation with Herbalife is broadly analogous, as the current share price reflects some material degradation of the earnings power of the business – with the US business being the most likely source of the decline. We are somewhat less secure in our belief in the case of HLF that consumer protection litigation/regulation can’t be exported outside the U.S. (versus product liability litigation in the case of the tobacco industry), but we believe that the international assets are likely far more secure than the domestic assets in the case that Pershing Square’s allegations prove to have some merit (an open issue, to be sure).

Recall that it is our belief that the Herbalife debate has become too high profile to be ignored by the powers that be – the FTC, SEC any of the State Attorneys General. We see some sort of investigation as highly likely, an event that the market will not likely treat kindly.

The Math

Consensus EBITDA estimates for 2013 EBITDA are $794 million (7.9% growth versus 2012) – of that number, we estimate that nearly $190 million in EBITDA will be generated in the United States (23.5%). It’s a bit of a chore to get to EBITDA by region and the company’s disclosures could certainly use some improvement – we agree with Pershing Square in that regard.

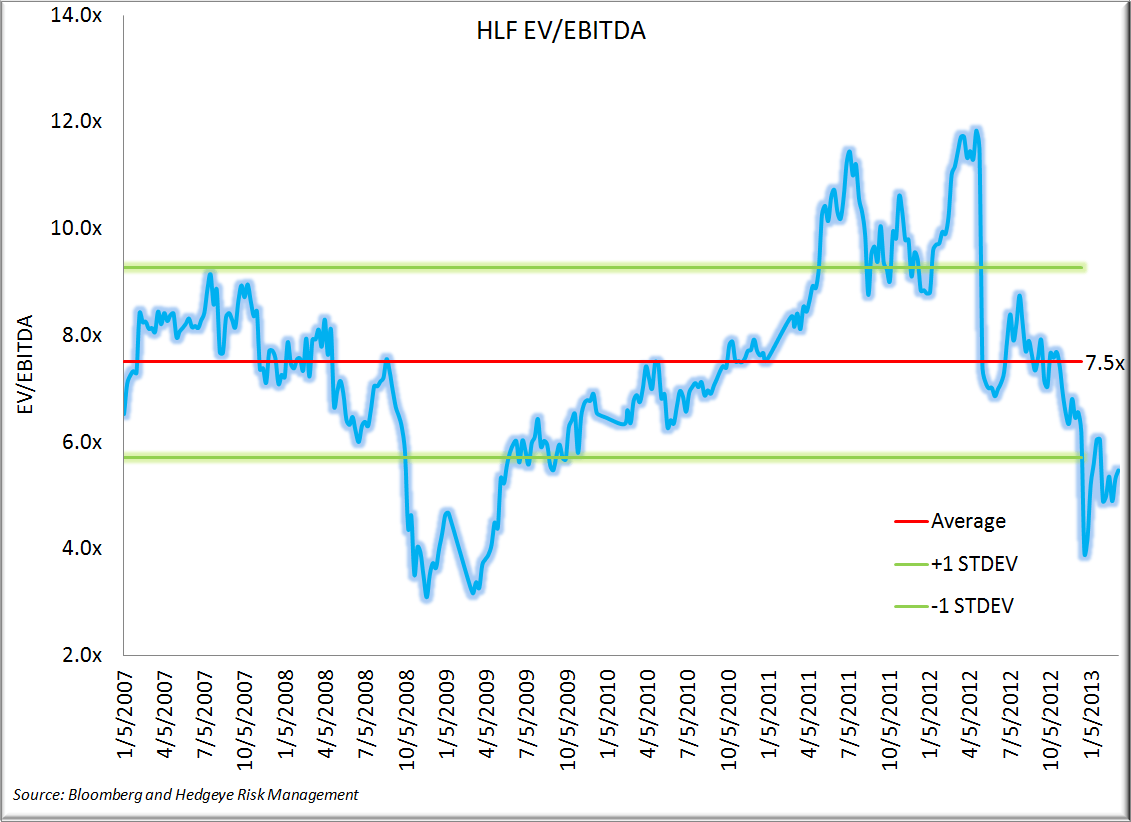

The company’s average forward EV/EBITDA multiple since 2007 is 7.5x – applying that multiple to the EBITDA forecast for the company ex-U.S. ($604 million) gets us to a share price of $42.50 for HLF’s business outside of the US, implying a negative value of $1.70 per share for the US business currently imbedded in the share price. At any multiple greater than 7.1x EV/EBITDA for the rest of the world, the U.S. business is “free” as currently reflected in the stock price. We think a multiple closer to 8.5x EV/EBITDA is more appropriate given peers and the growth profile.

We think replacing fear with math is always a useful exercise, and while emotions can drive stock prices beyond where the math would suggest, we think having some sort of analytical framework to look at what is currently being discounted is the best way to be right more often than not.

-Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

P: 203.562.6500

Matt Hedrick

Senior Analyst