This note was originally published March 12, 2013 at 15:47 in Macro

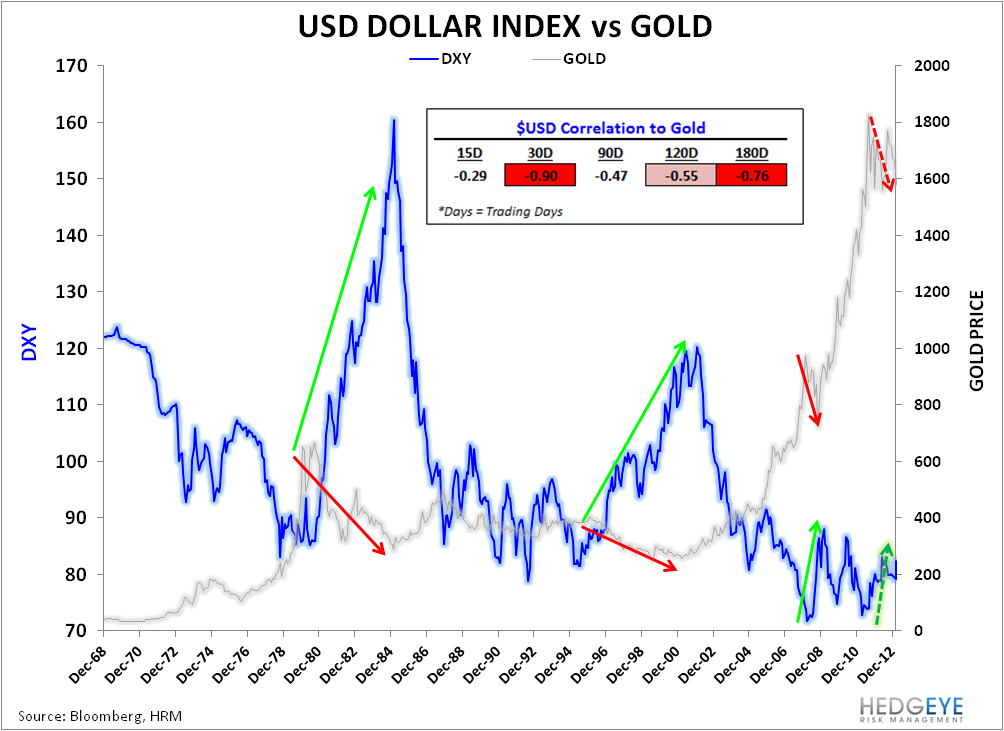

On the other side of our #GrowthStabilzing theme and our bullish TREND view on the Dollar and consumption oriented equities has been a bearish view on Treasuries, Commodities, and Gold.

We’re not self-proclaimed gold experts but we’d argue the fiat currency devaluation hedge underpinning the parabolic gold trade over the last five years has been fairly discrete. In short form, the Gold bug thesis can be adequately described as:

Economic growth stagnates/decelerates further --> Expectations for further QE initiatives rise --> $USD Depreciates --> Gold rises as investors discount erosion in the currency value and prospective future inflation and seek hard asset stores of value.

Within this framework, both the dollar and Gold become a function of the interplay between reported/expected economic conditions and expectations around monetary policy. When it plays out on a global level, as it has in the wake of the Great Recession, the variable mapping gets more complex and the price action exaggerated but the idea framework is still the same.

Its also important to note strength of the growth-policy-USD/Gold connection is stage or cycle dependent. For example, in the throes of economic or market distress the correlation between the USD & Gold tends to be positive as the safe haven trade plays itself out. However, outside of crisis conditions, fundamentals (growth, interest rates, policy, etc) become the prevailing drivers and moderate-to-strong inverse correlations between Gold and the Dollar have predominated, empirically.

So, as straightforward as we think the bullish case for gold has been is as simple as we think the bearish case that has been playing out currently in gold is. If you buy into the idea that weak growth, unconventionally easy monetary policy initiatives, and investor expectations around forward policy have been the principle drivers of gold price appreciation since 2008, then a reversal in these factors – stable/accelerating growth, a cessation & eventual unwinding of easing initiatives, a strong dollar, & rising interest rates - should serve to drive a correction in Gold prices.

What does the anatomy of that correction look like?

Summarily, it looks like more of what we’ve been seeing in Gold Prices, Dollar-Gold correlations, CFTC data, and gold ETF flows over the last four months – trends we’ve seen accelerate over the last five weeks as the economic data has flashed some upside and the dollar has begun to break out.

Consider the chart below which shows physical gold outflows from the GLD (SPDR Gold Trust) vs. the dollar.

Looking across a host of relevant factors, all of the charts (unsurprisingly) reflect a similar dynamic:

Gold vs Fed Balance Sheet: The correlation between Gold and the Fed’s Balance Sheet is strong across durations with an R^2 = 0.92 over the last 14 years. If you think this relationship makes common and economic sense (we do), a deceleration and unwind of policy intitiatives (or the expectation for) on the back of an improving growth outlook is a decidedly bearish catalyst for gold.

Gold vs. Dollar: Gold’s Inverse correlation to the dollar has been moderate-to-strong across durations. Gold is levered to the USD directly given that gold generally settles in dollars, and indirectly via expected inflation & policy impacts on fiat currency value. Correlations aren’t perpetual – they build and decay - but when they start to tighten alongside other relevant/corroborating factors, it’s generally worth paying attention. Gold’s 30D correlation to the dollar is currently -0.90.

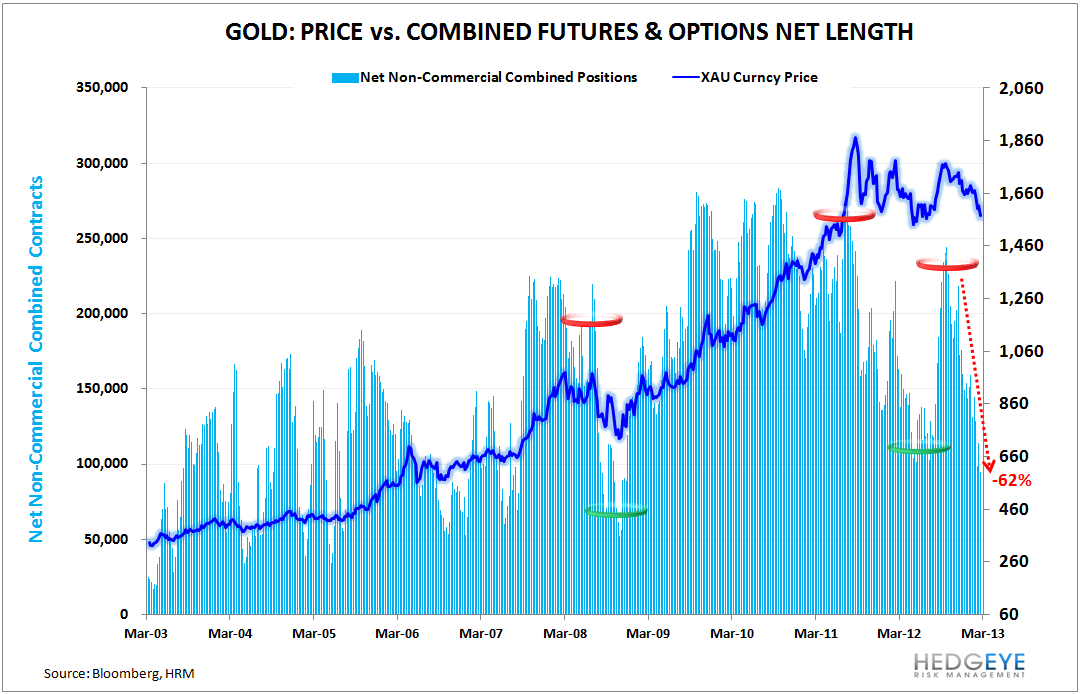

Gold - CFTC Data: Bullish Speculative positioning looks like its capitulating as net length in combined non-commercial futures & options contracts has collapsed since November. It hasn’t paid to speculate on the end of the world (again) as extremes in bullish positioning (>1STDEV) have been followed by negative subsequent price performance in gold 100% of the time over the last year. Net length is currently down ~62% from the late 2012 highs.

Gold ETF Flows: Gold flows to the GLD and ETF’s in aggregate, have rolled over since the beginning of the year and have accelerated to the downside over the last month. For example, total Gold Holdings in the SPDR Gold Trust (GLD) are down ~114 Tonnes (-8%) from peak 2012 levels according to bloomberg data.

This weekend, my brother, a sharp guy and passive retail investor, made the following rhetorical comment (paraphrased) “that jobs number was pretty good….who will be the marginal buyer of gold?”. Good Question.

The bull case for Gold was straightforward and price was reflexive on the way up. Reflexivity, by definition, works both ways and big crowds and small doorways still don't make great bedfellows.

If the growth data can continue to confirm, the USD remains in bullish formation and policy makers (Congress & the Fed) can stay out of the way, we think gold continues to hold some further downside.

In the more immediate term, equities are overbought and Gold/Treasuries oversold. From a quantitative perspective, Trade Resistance for Gold sits ~1.3% higher at $1612 with TAIL resistance up at $1681. If gold fails to recapture those lines on the bounce, and domestic housing and labor market trends remain positive, we’d be interested in playing any strength from the short side. We currently hold no position in gold in our Real-time alerts.

Christian B. Drake

Senior Analyst