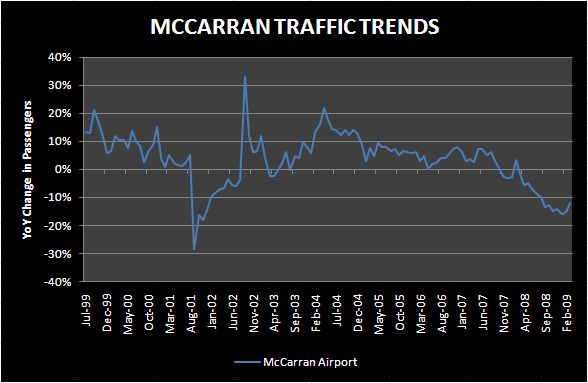

Despite one less Saturday, air passenger traffic through Las Vegas's McCarran Airport declined "only" 11.8%. I say only because this is the smallest decline since August of 2008. Are we calling a turn? Not yet, but a positive second derivative is a start. The real takeaway here is that lower room rates are having an impact. Demand is elastic and only time will tell if the incremental customer swayed by rate will gamble enough to be profitable.

Based on our regression analysis and assumptions regarding drive-in traffic and table and slot spend per visitor, we think total gaming revenue may decline by "only" 12%. The last drop smaller than 12% occurred way back in September of 2008. Similar to February, slot win should outpace table win, assuming normal hold percentages.

LVS will likely be the first Vegas centric casino company to report EPS. We continue to believe LVS was the standout in Las Vegas. We are less confident in the MGM and WYNN Q1 performance.