February comparable sales grew +2% in Yum!’s China division. Consensus was expecting -8.8%. This release is spurring optimism that the worst of the fallout from the chicken supply scandal in YUM’s largest market may be in the rear view mirror.

Sequential Improvement

Yum! Brands reported 1Q China comps of -20% versus consensus -24%, including KFC -24% and Pizza Hut -2%. February was a driver of sales growth with comps growing 2% versus consensus -8.8%, suggesting sequential improvement through the quarter. A timing shift related to the Chinese New Year had a positive impact in the mid-teens. KFC comps were flat in February while Pizza Hut comps grew 13%.

Full-Year View

We stepped back from our bullish stance on the immediate- and intermediate-term durations on February 4th, publishing a note titled, “YUM GUIDE DOWN A GAME CHANGER”, citing a lack of visibility on same-restaurant sales growth. The long-term growth story has remained intact through all of the volatility. Yesterday’s release suggests that the fallout from the chicken supply scandal may be abating with time as YUM’s PR machine has gone into overdrive to regain consumer trust. We will wait for further confirmation on the near-term duration, but this gives us confidence that the long-term upside for YUM shares represents an attractive opportunity for investors willing to look through near-term issues.

Our Sum-of-the-Parts valuation that we published late last year, as part of our Black Book titled, “YUM: BEST LARGE CAP OUTLOOK FOR 2013”, suggested a twelve month upside to the 11/29/12 share price of 20% to $89. While not for the faint of heart, we believe that YUM still represents compelling value over the long-term TAIL duration.

Please reply to this email for a copy of this Black Book.

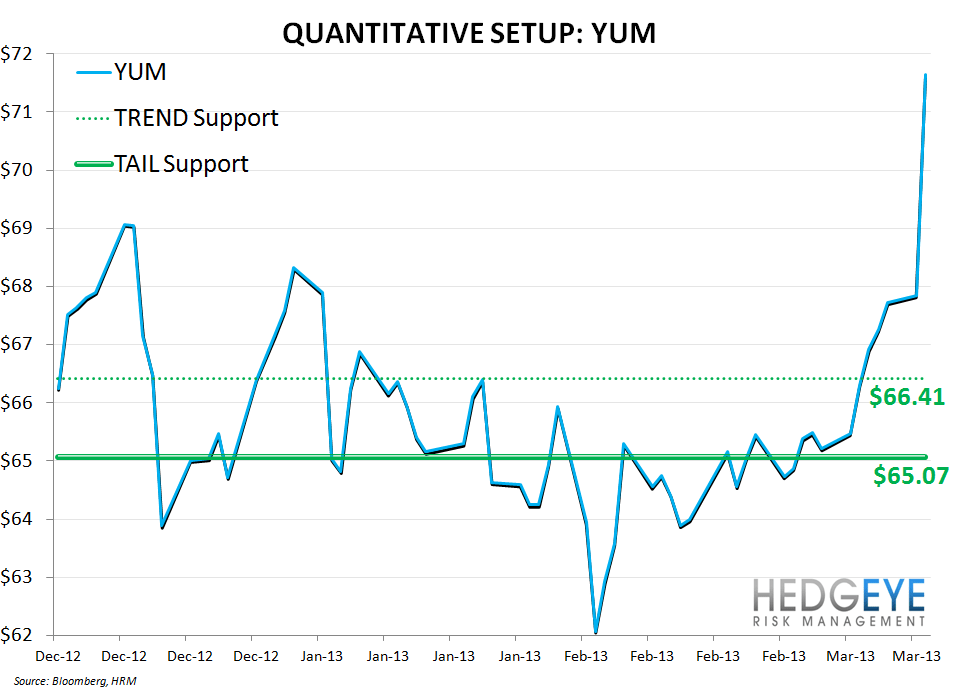

Quantitative Setup

Our CEO, Keith McCullough, sees the stock as breaking out of an important base. Intermediate-term TREND and long-term TAIL levels of support are at $66.41 and $65.07, respectively.

Howard Penney

Managing Director

Rory Green

Senior Analyst