TODAY’S S&P 500 SET-UP – March 12, 2013

As we look at today's setup for the S&P 500, the range is 31 points or 1.43% downside to 1534 and 0.56% upside to 1565.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.78 from 1.80

- VIX closed at 11.56 1 day percent change of -8.18%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB Small Bus. Optimism, Feb., est. 90.0 (prior 88.9)

- 7:45am: ICSC weekly sales

- 8:55am: Johnson/Redbook weekly sales

- 10am: JOLTs Job Openings, Jan. (prior 3.617m)

- 11am: Fed to purchase $1b-$1.5b TIPS due in 2017-2043 sector

- 11:30am: U.S. to sell 4W bills

- 1pm: U.S. to sell $32b 3Y notes

- 4:30pm: API weekly inventories

GOVERNMENT:

- House, Senate in session

- Senate Banking Cmte holds hearing on Cordray, White, 10am

- House Appropriations panel holds oversight hearing on SEC, 3pm

- House Appropriations panel hears from Food Safety, Inspection Service Admin. Alfred Almanza at oversight hearing, 10am

- All FCC commissioners testify at Senate Commerce Cmte’s oversight hearing on FCC, 2:30pm

- National Transportation Safety Board meets to consider 5 Safety Alerts aimed at reducing number of general aviation incidents, 9:30am

- Washington Day Ahead

WHAT TO WATCH

- HP says Serious Fraud Office investigating Autonomy

- SEC nominee White to face conflict questions at hearing

- Cordray nomination at stalemate amid wait for court ruling

- Citigroup added to team advising Dell buyout group: WSJ

- Costco 2Q revenue $24.87b misses est. of $24.95b

- GM share sale brought Treasury $489.9m in February

- Roman Catholic Cardinals to begin election of new pope

- U.S. accuses China of cyber espionage that threatens ties

- Greece in talks with creditors to cut 150,000 civil servants

- Yandex founders, investors to sell up to $607m of shares

- Goldman among banks to get lower fees for Japan Tobacco sale

- Galaxy Securities said to pick Goldman, JPMorgan for $1.5b IPO

- Suntech gets 2-mth forbearance on $541m in bonds

EARNINGS:

- Stage Stores (SSI) 6am, $1.15

- FactSet (FDS) 7am, $1.24

- Empire Co (EMP/A CN) 7:03am, C$1.15

- Laredo Petroleum Holdings (LPI) 7:26am, $0.10

- Raven Industries (RAVN) 9am, $0.25

- Acadia Pharmaceuticals (ACAD) 4:01pm, $(0.09)

- Dole Food (DOLE) 4:06pm, $(0.02)

- Investors Real Estate (IRET) 4:30pm, $0.17

- Kennedy-Wilson Holdings (KW) 4:33pm, $(0.08)

- PetroBakken Energy (PBN CN) After-mkt C$0.13

- Black Diamond (BDI CN) After-mkt C$0.31

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Halts Three-Day Advance on Supply; Chinese Refining Declines

- Gold Sales From Soros Reveal 12-Year Bull Run Decay: Commodities

- Soybeans Drop on Signs Brazil Is Gaining Market Share From U.S.

- Gold Futures Advance to Highest This Month on Technical Buying

- Copper Rises to $7,762 a Ton in London Trading, Erasing Decline

- Europe Copper Premium Seen Dropping for Second Month by Traders

- Oil Supplies Climb to Eight-Month High in Survey: Energy Markets

- Cocoa at 1-Month High as Prices May Have Bottomed; Coffee Slips

- Gold in India Heading to Lowest Since May: Technical Analysis

- Ships Reject Unprofitable Cargo to Halt Slump in Rates: Freight

- Arabica-Coffee Premium Versus Robusta Falls to Lowest Since 2009

- Europe Gas Carnage Shown by EON Closing 3-Year-Old Plant: Energy

- Crop Price Ratios Can Foreshadow Crop Planting Decisions

- Wall Street $100 Million Man Makes Downton Abbey in Vermont Town

CURRENCIES

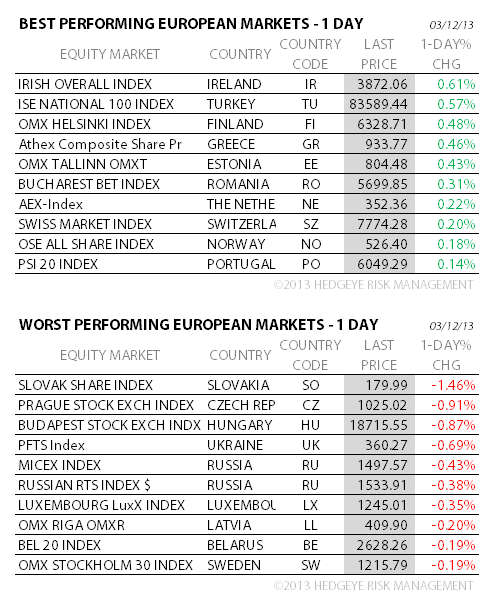

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team