MCD reported February global same-restaurant sales growth of -1.5% versus consensus of -1.6% (not adjusting for the calendar shift). While calendar shifts are material for monthly headline numbers, the trend in McDonald’s comparable sales growth is unmistakably negative. In five of the last eight months, McDonald’s has reported flat or down same-restaurants sales growth. This is the longest sustained slowdown in sales trends since the company’s historic “plan-to-win” turnaround.

This begs the question: can McDonald’s maintain its long term system-wide sales and operating income growth targets of 3-5% and 6-7%, respectively?

We remain skeptical that this slowdown is macro-driven; it seems evident that there are company-specific issues that are yet to be addressed by management. Below, we update our thoughts on the various geographies.

Conclusion

There is nothing in the currents sales trends or in management communicated turnaround strategies that would cause us to reverse our negative stance on MCD. We still believe MCD will see flat-to-low single digit EPS growth in 2013. The emphasis on value has boosted MCD SRS growth in recent months, but history has shown that this strategy is not effective over the long term. In fact, it externalities of this approach can impede sustainable earnings growth over time as operational complexity increases.

The macro environment is challenging for a number of companies but the changes in McDonald’s long-term trends suggest that there are company-specific issues at play. The current guidance for food inflation suggests that 2013 will not be as big an issue for MCD as in 2012, but the risk of upward revisions remains high. Operating margins around the world are likely to continue to be pressured by sales deleveraging and incremental development costs.

Our macro team retains its bullish view on the USD which would be a headwind for MCD Earnings, given its FX exposure.

MCD U.S.

February comparable sales growth for the domestic market was -3.3%, or flat excluding the segment’s calendar shift, versus consensus of -3.6%. Sales were better than expected despite choppiness in consumer spending trends. February represented the most difficult comparison for MCD in the U.S.

Detail:

- Fish McBites were introduced

- Heavy focus on the Dollar Menu continued

- Several lower-performing items were dropped from the menu, including the Fruit & Walnut Salad and Chicken Selects. We expect McDonald’s to drop the Angus Burger in the near future

- Monthly SRS have held up on the back of incremental value message promotion, but this is not a sustainable trend

- Extended hours are not driving incremental sales

- The $6-7 casual dining lunch price point of $6-7 is competitive with MCD core menu items at lunch

MCD Europe

Europe comparable sales growth came in at -0.5%, or +2.7% excluding the calendar shift, versus -0.4% consensus.

Detail:

- Russia and the UK continue to generate positive same-restaurant sales on the back of extended day parts and it appears that the horsemeat scandal may not have significantly impacted UK trends

- German and France continue to experience declining sales and traffic trends, despite continuing messaging around value platforms

- Margins in Europe are under pressure and will likely Margins in Europe are under pressure and will likely continue to contract in FY13 as sales growth remains under pressure in the region

- The boost from reimaging is likely to diminish over time as almost all of the interiors and half of exteriors in the region have been completed

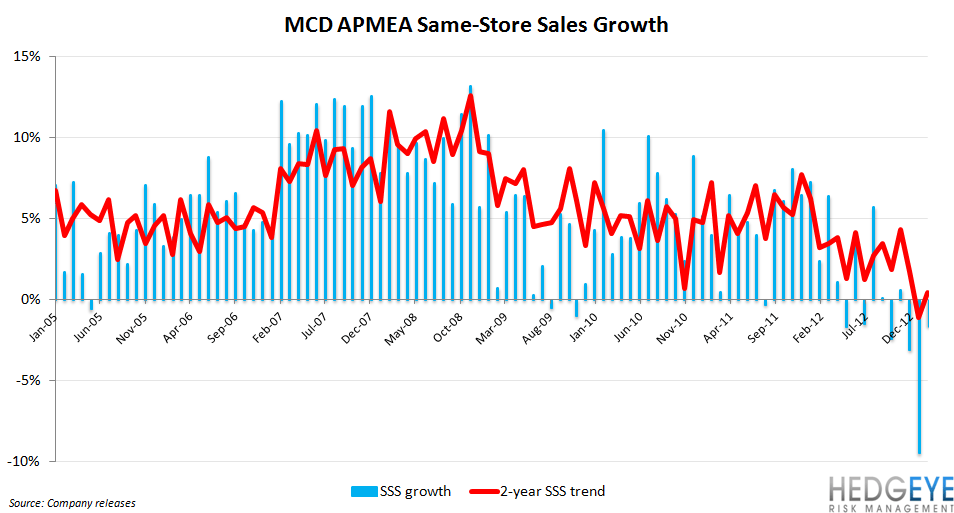

MCD APMEA

Asia/Pacific, Middle East and Africa (APMEA) February comparable sales growth decreased -1.6%, or +1.5% including the segment’s calendar shift, versus consensus of -1.5%.

Detail:

- Australia continues to deliver positive SRS growth, while China benefited from the timing of Chinese New Year

- Japan trends remain soft with February SRS trends of -12.1%

- Average check at MCD Japan improved but traffic continued to decelerate, declining -10.9% year-over-year, versus the -8.1% decline in January.

- Given the seemingly secular deceleration in Japan and the difficult environment in China, APMEA is also likely seeing continued margin pressure

- What ideas, beyond value, are being put forward to improve the APMEA business?

- Almost 2/3 of markets offer extended hours of some form and over half are open 24 hours. This spigot is slowly closing from an incremental sales growth perspective.

Howard Penney

Managing Director

Rory Green

Senior Analyst