McDonald’s is a very healthy company, with slowing trends and margin pressure around the world. In summary, this was not a great quarter from MCD. The company reported 1Q09 EPS operating EPS of $0.83 vs. $0.82 and the earnings benefited from a lower tax rate of 28.6% for 1Q09 as compared with 30.6% for 1Q08.

The march comps were basically in line with consensus estimates, but mark a significant slowdown from last year. Globally, McDonald’s reported 4.1% same-store sales with the United States up 5.6%; Europe up 2.9% and APMEA up 5.4%. The calendar shift/trading day adjustment varied by regions, ranging from -1.0% to -1.8% in March 2009. In March, Europe’s comps were negatively impacted by approximately 2% due to the change in timing of Easter-related school and business holidays from March 2008 to April 2009. On a consolidated basis, traffic increased 1.0% in 1Q09 vs. 3.2% for 2008 and was negatively impacted by 1% due to the leap year.

Most notable and relevant to what we may hear from YUM is MCD’s commentary on China. Due to employment issues in Southern China, McDonald’s reduced unit openings for the year from 175 to 150.

McDonald’s also noted that same-store sales in China were negative for 1Q09 and got worse as the quarter ended. Importantly, McDonald’s cut prices by 30% during the quarter to help mitigate the decline in traffic trends. Needless to say this is very painful to McDonald’s margins during the quarter.

McDonald’s management team noted that the decline in menu prices in China was due to signs that Chinese consumers were trading down from Western QSR down to Chinese QSR. According to MCD, Meal prices for Chinese QSRs are close to 30-40% below what a traditional western QSR meal prices are. Western style QSR has more to compete against that Chinese QSR, but food at home too. Western QSR is a luxury for most Chinese consumers. With higher unemployment and slower income growth, the typical consumer is going to look for cheaper alternatives.

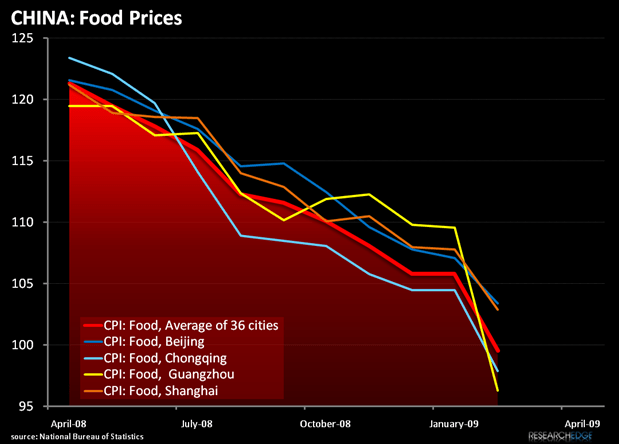

The most recently available CPI data for urban areas showing an average food cost decline of nearly 22% since last April. So McDonald’s 30% menu price cut, is only keeping pace with alternative distribution channels.

A key question now is; does a 30% price cut represent a sufficient inducement to consumers alarmed by economic contraction and job losses to spend money on pricey fast food at the same pace they did during better times?

None of these data points are positive for YUM. Importantly, YUM success is very closely aligned to how its China business performs. Looking to when YUM reports 1Q09, I expect YUM to face similar challenges as YOY commodity pressures will be more severe in 1Q09 (vs. 4Q08) and the company is lapping 12% same-store sales growth and 33% operating profit growth.

Currently, YUM is trading at 8.3x NTM EV/EBITDA and the stock is up 6% in the past week and 18% over the past month. Why? |