With the equity market making new highs and our domestic-centric 1Q13 Macro Investment themes of #GrowthStabilizing and #HousingsHammer continuing to play out, the relevant risk management question at hand is whether the data is credibly signaling a hand-off from #Growthstabilizing to #GrowthAccelerating.

Across some of the more recent higher frequency economic data, the new orders component within the ISM Mfg, ISM Services, and PMI mfg survey’s all accelerated sequentially in February while yesterday’s Corelogic Home Price data saw January home prices rise +9.7% y/y (up from the prelim estimate of 7.9%) with the preliminary February estimate coming in at +9.7% as well – the second strongest February print in the last 20 years.

If the current slope in the rate of price appreciation in the non-distressed market continues, pricing growth could see an incremental 500bps of upside over the NTM. With demand rising (Pending, New, & Existing Home sales data) and supply falling (months-inventory making new lows) we think the dynamics are in place to support further pricing strength.

In addition the positive housing & economic activity data, Yesterday’s higher than expected ADP number and this morning’s jobless claims data offer confirmation of accelerating improvement in labor market trends. Today's SA Initial claims print of 340K was a headline positive, while the improvement in the NSA initial claims data accelerated to +9.5% y/y vs. +8.0% in the prior week.

Below is the weekly detailed analysis of the claims data from our head of Financials, Josh Steiner. If you would like to setup a call with Josh or trial his research, please contact

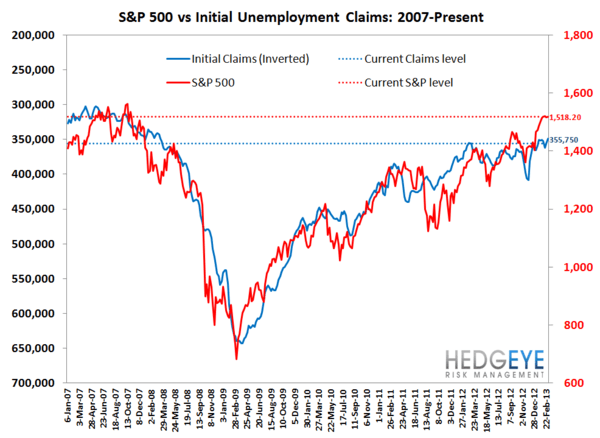

Labor Market Strengthens Further

This past week's NSA (Non-seasonally adjusted) initial jobless claims were better YoY by 9.5%, which is from the 8.0% YoY improvement in the previous week. This print reflects data through March 2, so next week should be the first week that sheds light on whether the sequester is actually having an impact. On a rolling basis (4-wk moving average), NSA claims were better YoY by 4.3%, which was improved from 2.6% in the previous week. These two measures, the YoY change in NSA and rolling NSA claims, are the better indicators of what's really happening in the labor market, and they both indicate the labor market is strengthening.

On the SA (seasonally-adjusted) front, the numbers look great. This is what the market is paying attention to. As a reminder, last week was the final week of tailwind for the series and we'll now be gradually shifting from tailwind to headwind over the coming six months. The first chart in the note tells the story well.

The Data

Prior to revision, initial jobless claims fell 4k to 340k from 344k WoW, as the prior week's number was revised up by 3k to 347k. The headline (unrevised) number shows claims were lower by 7k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -7k WoW to 348.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -4.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -2.6%

Joshua Steiner, CFA

Christian B. Drake