Anything less than double digit growth would be a disappointment

Based on the last 3 months of actual growth and factoring in seasonality, we’re projecting 10-15% YoY growth for March. Excluding the impact of low hold, investors should be disappointed with growth less than double digits.

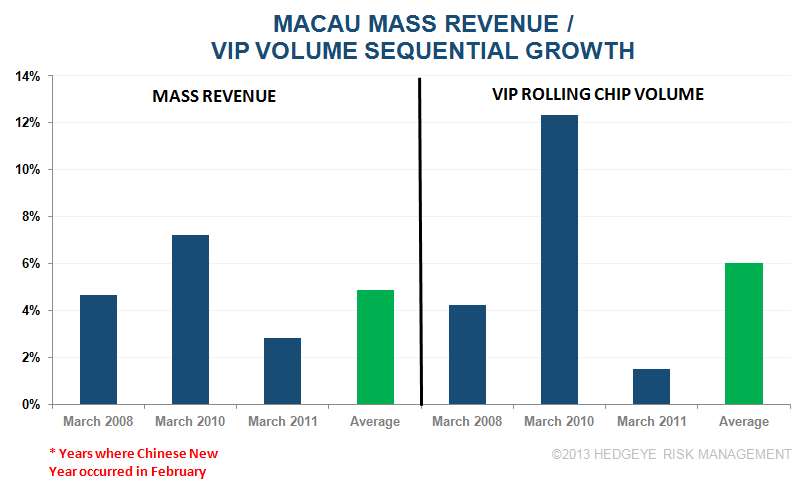

Why should we be disappointed with even high single digit growth? For one, the hold comp is very easy. March 2012 VIP hold was the lowest of 2012. Moreover, March VIP volumes and Mass revenues have historically averaged 6% and 5% sequential growth over February in years when Chinese New Year occurred in February. A simple calculation using these sequential growth rates yields 15% YoY growth for March, at the high end of our projection.

Even with flat MoM revenues, March would still exceed last year by 8%. Our projection methodology is more comprehensive than these simple sequential analyses but we find them useful as a reasonableness check. Any way we look at it, March YoY growth should be strong and an acceleration from January and February. A non-hold related miss from our projection could be indicative of a slowdown in the underlying fundamental trends or the impact from the China corruption crackdown.