Is this the start of something big?

The question we have received most in the wake of Heinz being acquired by 3G with financing provided by Berkshire Hathaway is “who is next?” We attempted to answer that question specifically in a prior analysis that highlighted some of the characteristics of Heinz that might have made it attractive to a cost-minded acquirer such as 3G. Here, we attempt to answer the question behind the question which is whether or not we are poised for a wave of acquisitions across staples, specifically packaged food.

We are of the opinion that merger waves are a consequence of industry “disruptions”. These disruptions don’t have to be single events, but can be built up over a longer duration and comprised of multiple smaller events, rather than a single significant event. There isn’t a great deal of academic research to fall back on with respect to this topic – Mitchell and Mulherin (1996) argued that industry-specific merger waves occur as a “common response to regulatory, technological and economic shock.” The new competitive dynamic requires a reallocation of capital within in an industry.

Interestingly, most “waves” occur during strong, broader markets with varying theories for this – access to capital or perhaps a desire on the part of managers to trade “expensive” paper for “real” assets - Maksimovic and Phillips (2001) and Jovanovic and Rousseau (2001). Interestingly, research suggests (unsurprisingly) that engaging in merger activity in strong markets and subsequent to prior deals in the same industry may not necessarily be a recipe for creating shareholder value.

Looking back at the wave of consolidation in packaged food in 2000 (see below), it appears that it was in response to a shift in the balance of power between manufacturers and retailers brought about by a prior wave of consolidation within food retail. From 1996 to 2000, assets representing nearly $75 billion of retail sales were consolidated in US food retail, including two of the biggest combinations in history (Albertson’s/American Stores and Kroger/Fred Meyer).

Packaged food manufacturers were faced with a sea change in terms of relative power versus retail counterparts (recall that Wal-Mart was becoming an increasingly more significant participant in food retail at this time as well). Scale mattered again, and, in fact, became an imperative versus larger retail partners. The packaged food industry responded in kind.

2000 Was a Huge Year for Packaged Food M&A

Unilever approached Best Foods in May of 2000, with the deal price ultimately agreed to in June (approximately 10% higher than the original offer, total consideration of $24.3 billion). Later that same month (June), Philip Morris (at that point still the tobacco/food conglomerate) agreed to acquire Nabisco for $15.5 billion. The bidding for Nabisco was robust, with Danone and Cadbury as other engaged parties.

Though not the purchase of a public company, General Mills agreed to purchase Pillsbury from Diageo at the end of July for $10.5 billion.

In a smaller transaction relative to the food deals in 2000, Kellogg acquired Keebler Foods for $3.9 billion in October. The year wasn’t quite over, as Pepsi acquired Quaker Oats in December for $13.4 billion.

Does the same imperative exist now?

We would argue, no. If anything, we believe that food retail’s relative position has only weakened over the last decade. Channel blurring is a familiar term for most investors and we have seen data that suggests that fully ¾ of consumers shop more than 5 CPG channels regularly. Fewer trips and smaller tickets per trip to each retail channel has “spread the wealth” among various retailers and retail concepts to the point where conventional grocers (the catalyst for the last wave of packaged food consolidation) continue to struggle. Certainly Wal-Mart’s importance continues to grow, but we see an acquisition that could successfully balance a supplier against Wal-Mart as being highly unlikely, if at all possible.

Further, since 2000, an entirely new channel has emerged – the natural and organic store. The trend toward health and wellness has certainly represented a “shock” in some sense of the word. Capital has been reallocated by the packaged food manufacturers to address this competitive disruption, but the size of the channel doesn’t allow for “mega” deals, so we don’t see this trend, while certainly powerful and ongoing, as a catalyst for large scale M&A.

Is age a factor?

There is some work that suggests that the age of CEO’s within a particular industry might be a catalyst for merger activity. We only mention this because, Bill Johnson of Heinz, at age 64, was the oldest of the CEO’s in large cap packaged food. Denise Morrison at Campbell Soup and Irene Rosenfeld at Mondelez are “next in line” at age 59, with Ken Powell of General Mills close behind.

Where does this leave us?

It appears that some conditions have been met for a “wave” of merger activity – a strong market, access to liquidity and perhaps the age of the relevant CEOs. However, we are simply not seeing the “shock” to the system that forces companies to pursue acquisitions in an environment where current valuations make the creation of shareholder value through mega deals an uncertain prospect at best.

If no more deals, what’s next?

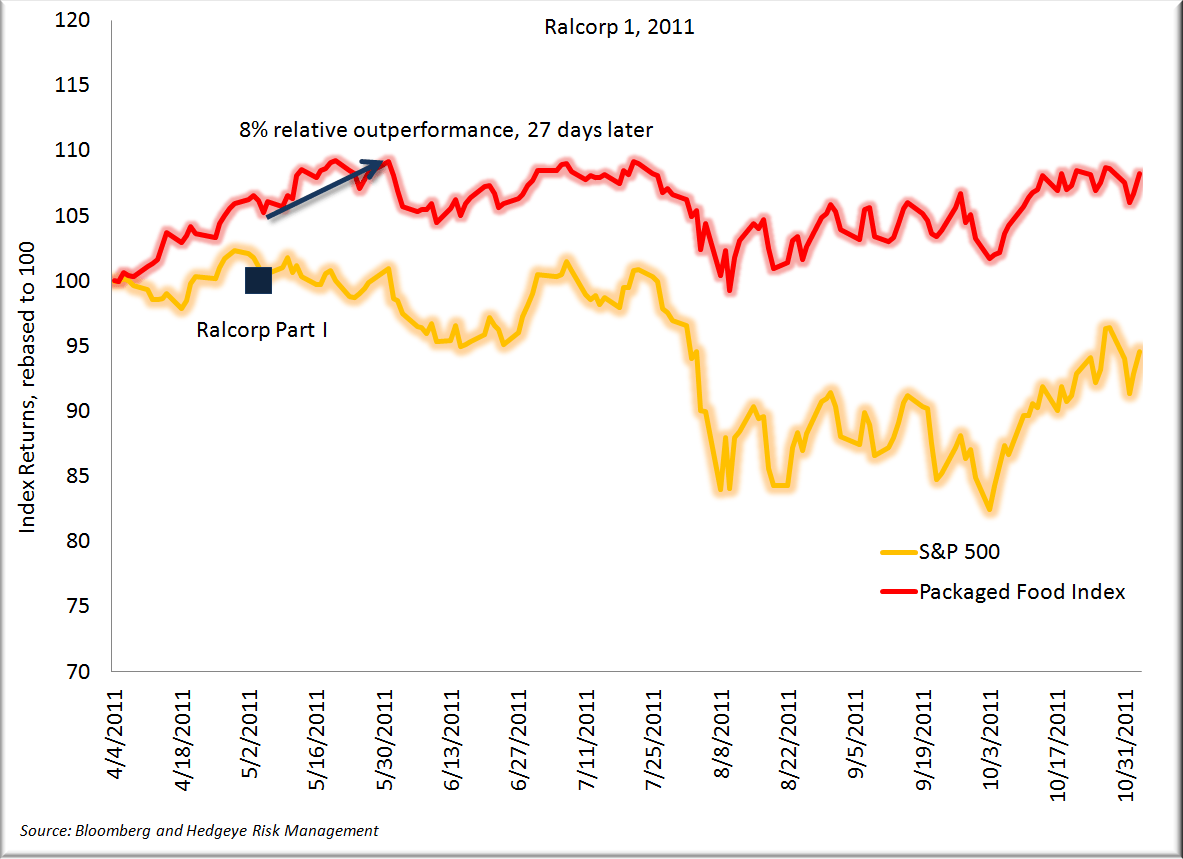

We decided to take a look at the performance of the S&P Packaged Food Index into and subsequent to some recent, large transactions, as well as the performance of the indices in 2000. No question, if we are at the start of a wave of consolidation within packaged food, there is room to run – trough to peak relative performance in 2000 for the index was +46%. Wrigley in 2008 as a “one off” event represented far less compelling relative performance, but as everyone is well aware, ’08 is a difficult year to which one can (or should) draw analogies given market conditions. Ralcorp (the first time around) is useful - +8% relative performance; 27 days later (call it a month). Right now, with Heinz, the numbers stand at +6% relative performance, 14 trading days post-deal. That suggests to us, using Ralcorp as an example, that we have some more time and price before it becomes “safe” to short packaged food stocks again.

Call with questions,

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst