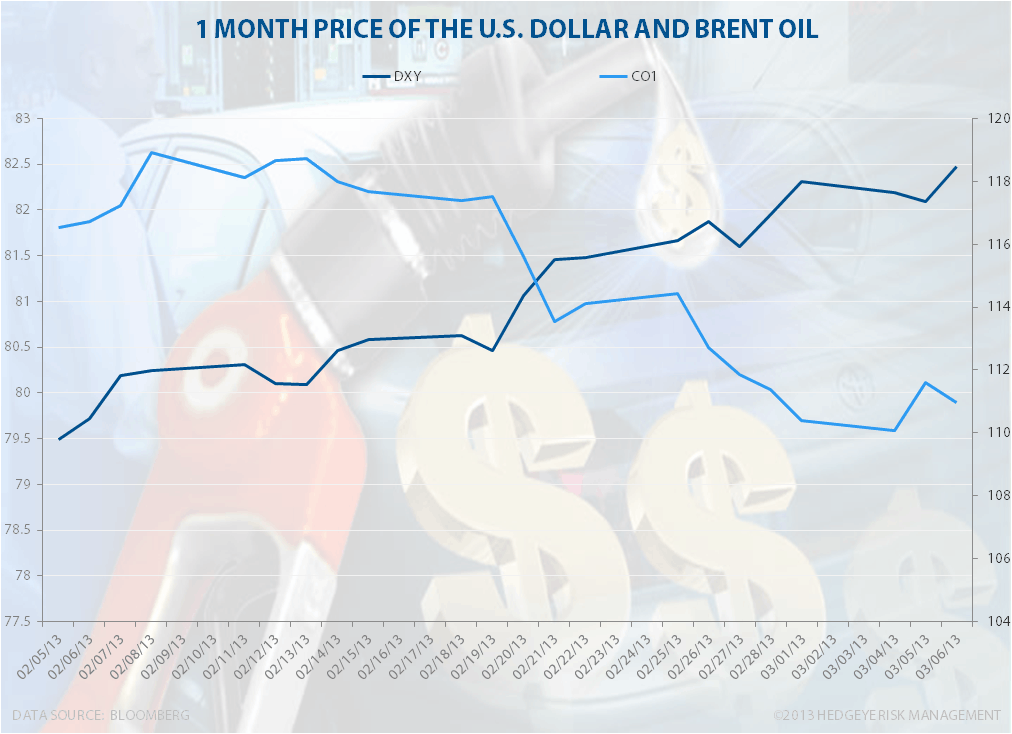

Over the last month, the US dollar has strengthened considerably, which in turn has helped deflate the great commodity bubble brought on by the policies of the Federal Reserve. Over the last month, Brent Crude oil has fallen from $119 to nearly $110 a barrel. Lower oil prices are a tailwind to recovery in the economy and help increase consumption. More consumption is a boon for stocks as consumers spend more instead of worrying about the price at the pump.