This note was originally published at 8am on February 20, 2013 for Hedgeye subscribers.

“Let’s not make our mistakes in a hurry.”

-Dwight D. Eisenhower

The 34th President of the United States was a process guy. He was also a world class Risk Manager. Getting the US out of Korea, averting the French invitation to Vietnam (1953), and avoiding the ongoing threat of engaging China or Russia in nuclear war is his legacy now. If you are a Portfolio Manager in this game, your legacy is your track record – and it’ll be the mistakes you don’t make that matter most.

But what kind of team culture should you foster to ensure you aren’t missing something? Do you accept the blame for your team’s mistakes, or do you point fingers? Is there an open forum for people who report to you to disagree with your position? If they do so and have sloppy reasoning, do they expect to be taken to task in front of their peers in kind?

I’m an athlete who believes in transparency, accountability, and trust. I have biases. But they are based on experience. There are a lot of great players – and even more good teams. But only few Championship Teams can repeat. To do that, your players can’t be scared to make a mistake. At the same time, they have to be disciplined so that their mistakes don’t blow up everything the team has worked for.

Back to the Global Macro Grind…

Particularly when a market is in a Bullish Formation (Bullish on all 3 of our core risk management durations: TRADE, TREND, and TAIL), not getting squeezed (on the short side) can save the team from having a lot of losses.

If you accept that bullish and bearish formations (Gold is in a Bearish Formation, so is the Japanese Yen) can get immediate-term TRADE overbought and oversold, at a bare minimum you won’t be making the same mistakes over and over again in a hurry. You’ll wait.

It’s taken me at least 13-15 years to learn this the hard way. Getting squeezed is part of a short seller’s life. And guess what, I still have to re-learn the same lesson, weekly. This game isn’t easy. That’s why I try my best to make decisions on the signal now, instead of the noise.

To simplify what I mean by making high-probability decisions:

- Don’t be in a hurry to sell something until you get an immediate-term TRADE overbought signal

- Don’t be in a hurry to buy something until you get an immediate-term TRADE oversold signal

- Don’t eat yellow snow

Or, as President Eisenhower used to tell his brother Milton, “Never get in a pissing match with the skunk.” (Ike’s Bluff, pg 57)

Yes, I am sure there are some really smart people out there who have found a way to not have to deal with process, real-time decision making , etc. But I can almost guarantee you that what they do ends up having a higher realized level of volatility than what we do.

To put some meat on this bone, here are some immediate-term TRADE overbought signals in our models this morning:

- SP500 is immediate-term TRADE overbought at 1533

- Russell2000 is immediate-term TRADE overbought at 934

- Consumer Staples Sector ETF is immediate-term TRADE overbought at $38.06

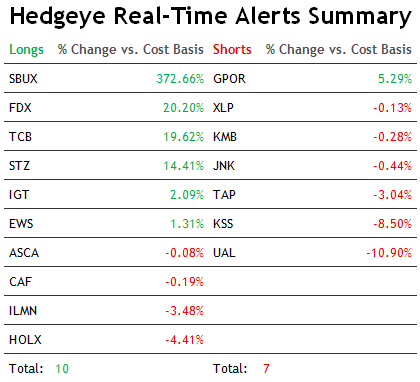

- Kimberly Clark (KMB) is immediate-term TRADE overbought at $92.31

- Fedex (FDX) is immediate-term TRADE overbought at $107.39

First, note that I have no immediate-term TRADE overbought signals to act on in any of our long Asian Equities positions. Singapore (EWS) has immediate-term upside, and so does China (which we bought via CAF on an immediate-term TRADE oversold signal yesterday).

Second, I am agnostic on the direction of the signal. It works the same way for both my longs and shorts. Yes, we like and are long of Fedex (FDX), but A) that’s not new (we bought it when we went bullish on US Equities in late November) and B) what is new is that it gave me its first immediate-term TRADE overbought signal in at least the last few weeks.

Third, using immediate-term TRADE overbought signals is another way to hedge market (beta) risk. So, I can be bullish on US Equities on my intermediate-term TREND duration and A) realize I might get an overbought signal in SPY this morning but B) not force myself to short something consensus like SPY, and stock and sector pick on a better signal instead (shorting XLP and KMB into yesterday’s close).

I am certain that there are better ways to do this – and I assure you that before I retire, I will find better ways. But for now, this is how my team rolls because this process is both repeatable and helping us not hurry mistakes.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, and the SP500 are now $1596-1617 (Gold remains in a Bearish Formation but is immediate-term TRADE oversold), $116.51-118.71, $80.25-80.83, 92.63-94.49, 1.97-2.05% and 1518-1533, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer