“How do you tell a communist? Well, it’s someone who reads Marx and Lenin. And how do you tell an anti-Communist? It’s someone who understands Marx and Lenin.”

-Ronald Reagan

As Hedgeye has grown over the past five years, we’ve gone from a ramshackle group of less than ten to a team that is fifty or more with a view to a much higher employee count as our growth continues. For those of us that started here near day one, it has been an exciting and fulfilling experience.

Many of you that have started you own businesses know full well the management challenges associated with growth – compensation plans, career paths, titles, HR meetings, committees, and so on. I can’t speak for Keith, but there are certainly times where I wish I could channel my inner Karl Marx and completely control our day-to-day functions. That, of course, would be a disaster because our company, like most companies, benefits greatly from disparate opinions and personalities.

The caveat to that last point of course is China - a country that has seen fabulous growth and development with top down controlled management. In 1978, China was one of the poorest countries on the planet with a GDP of roughly one-fortieth of the United States. As Xiaodong Zhu, a Professor of Economics at the University of Toronto, writes:

“Since then, China’s real per capita GDP has grown at an average rate exceeding 8 percent per year. As a result, China’s per capita GDP is now almost one-fifth the U.S. level and at the same level as Brazil. This rapid and sustained improvement in average living standard has occurred in a country with more than 20 percent of the world’s population so that China is now the second-largest economy in the world.”

If President Ronald Reagan were alive today, it would be interesting to hear his assessment of the Chinese economic miracle. Despite his, and many a dour assessment of Communist economies, China has certainly proven the critics wrong.

In the short term, yesterday certainly provided some fuel to the proverbial fire for those negative on the Chinese economy this year. China’s CSI 300 index was down -4.6%, its biggest drop since November 10th, the Shanghai Composite was down -3.7% (the most since August 11th), and the Shanghai Property index was down -9.3%. The decline in the property index was hit on reports that Beijing has introduced new property curbs calling for higher down-payment requirements, higher interest rates on second home mortgages and a 20% tax on individual profits from property sales.

One of the top ideas in our recently launched Best Ideas product was China, via the closed end fund CAF. Given the performance of Chinese equities noted above, this position is now against us, but our Senior Analyst covering Asia, Darius Dale, addressed this directly yesterday in a note titled, “China Pukes”. As Darius wrote:

“In short, while we think this latest round of tightening measures is definitely impactful, they are not nearly as negative as we initially feared. The heightened concerns mostly stem from the new 20% capital gains tax on existing home sales; prior to Friday’s announcement, existing home transactions were taxed at a rate of 1-2% of the sale price.

To some extent, today’s “puke” instructs us that our initial interpretation of the tightening measures was not bearish enough. That said, however, rather than react to headline-grabbing 1D % change moves, we turn to our quantitative factoring for true guidance.

On this metric, the Shanghai Composite is still healthily bullish from an intermediate-term TREND perspective and continues to support our bullish intermediate-term fundamental bias on Chinese equities. If, however, the now-confirmed immediate-term TRADE breakdown is but a leading indicator for further breakdowns, then we’d happily abandon our bullish bias upon confirmation of that signal.”

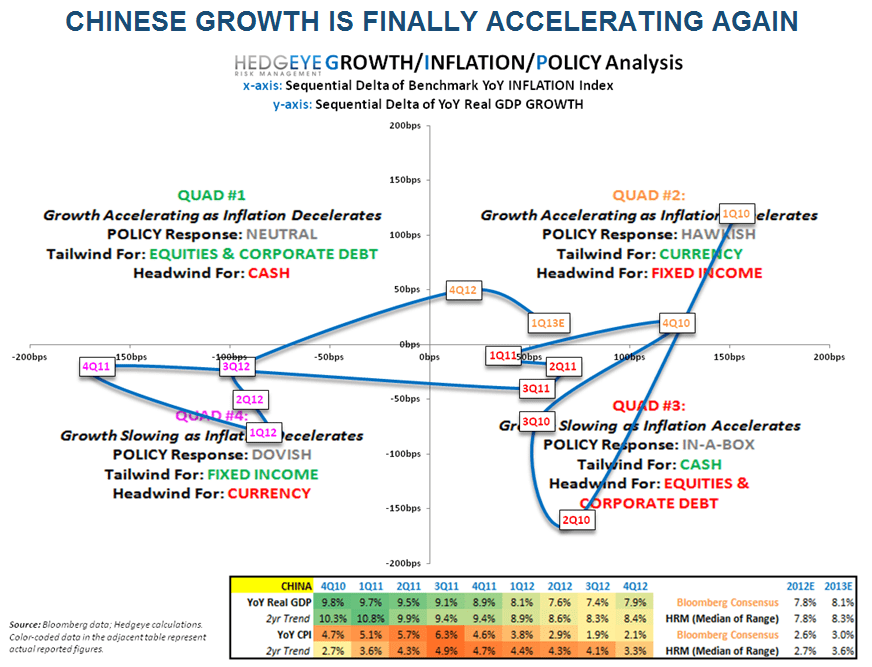

In the Chart of the Day, we highlight our quantitative levels that still support being long of China. In fact, news this morning from China’s Premier Wen last “state of the country address” in which 2013 GDP growth was set at +7.5% and CPI at +3.5% bolsters our thesis. On the latter point, if CPI actually declines from 4.0%, which commodities support, this is positive for our thesis, especially if combined with what we believe will be a sandbagged GDP number.

The other interesting call-out from Wen’s speech is that China intends to raise its budget deficit by 50 percent to boost consumer spending. Longer term structural deficit spending is not something that we find overly appealing, but this is likely supportive for GDP targets in 2013.

Changing gears, from an asset allocation perspective, even as many are starting to call for a rotation into bonds, the U.S. 10-year Treasury is holding its 1.84% line. As a result, we continue to see a rotation out of the “end of the world” trade of long gold and treasuries and into U.S. equities in 2013. There are very large bond investors that disagree with our call, but as always – watch what they do and not what they say.

Since we are on the topic of China, I wanted to end with a quote from Thomas Friedman that on some level summarizes the future:

“When I was growing up, my parents told me, finish your dinner. People in China and India are starving. I tell my daughters, finish your homework. People in Indian and China are starving for your job.”

Indeed.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, USD/YEN, UST10yr Yield, VIX, and the SP500 are now $1, $109.01-112.68, $3.48-3.55, $81.68-82.39, 91.89-94.79, 1.84-1.93%, 12.57-15.61, and 1, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research