This note was originally published March 03, 2013 at 13:14 in Consumer Staples

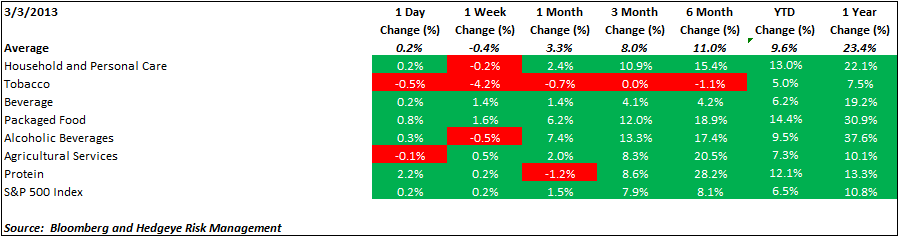

February saw 4/7 sectors in our universe outperform the broader market (non-alcoholic beverages just underperformed the S&P 500 during the month). Tobacco lagged on regulatory concerns and the protein sector suffered when TSN suggested that trends in the current quarter were weaker than originally anticipated.

This month we added something new - we took a look at the sector’s performance by P/E quartile – unsurprisingly, the 3rd quartile (P/E ratios between 16-20.7xs) had the strongest monthly performance (HNZ was in this quartile). The HNZ transaction drove multiples broadly higher in large cap staples name, several of which traded in the same P/E range – CL, CLX, PEP. MDLZ was the weakest performer during the month and the only negative performance within that P/E quartile.

Similarly, within the 2nd P/E quartile (P/E ratios between 13.3 and 16.0x), HNZ appeared to have been the primary driver of monthly performance – CPB was the best performer in that quartile (+12.1%). The quartile’s performance also benefitted from KMB (+5.3%) and GIS (+10.3%).

The 1st P/E quartile (P/E ratios less than 13.3xs) was all about STZ (+36.7%) – the quartile would have been up 1.7% but for STZ. A second of our preferred names, (STZ, at the time, being the first) ADM, was a significant contributor to the quartile’s performance, +12.4% on the month.

Higher multiple names in the sector had a good month was well, with SAM (+10.8%) and BNNY (+17.0%) the best performers. Multiples expanded across all quartiles as prices continued to move higher and estimates for 2013 were lower to unchanged coming out of Q4 earnings season for most sectors (protein being the notable exception).

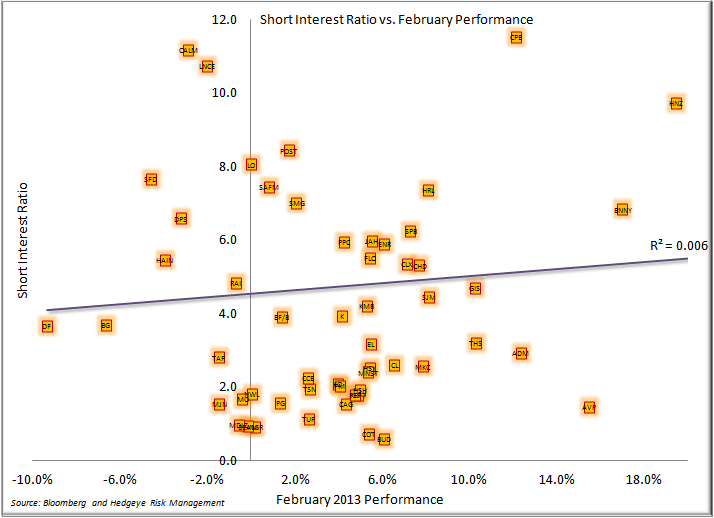

Consistent with a broad-based rally in the consumer staples sector, there hasn't been a significant divergence between high and low beta names. If anything, lower beta names have outperformed in the wake of the HNZ acquisition, likely setting the stage for some mean reversion in lower beta names as the takeout speculation wanes.

This is a familiar chart for those of you who have been following our work - it is also the chart that keeps us broadly cautious across the sector.

The anomalous relationship between the XLP and the 10 year that has existed since 2009 persists...

...despite the fact that the yield of the XLP has become marginally less attractive (combination of the yield on the 10 year creeping up and the price performance of the XLP).

Some clients have suggested to us that the move up in the group post-HNZ has been short-covering - the data doesn't appear to bear that out.

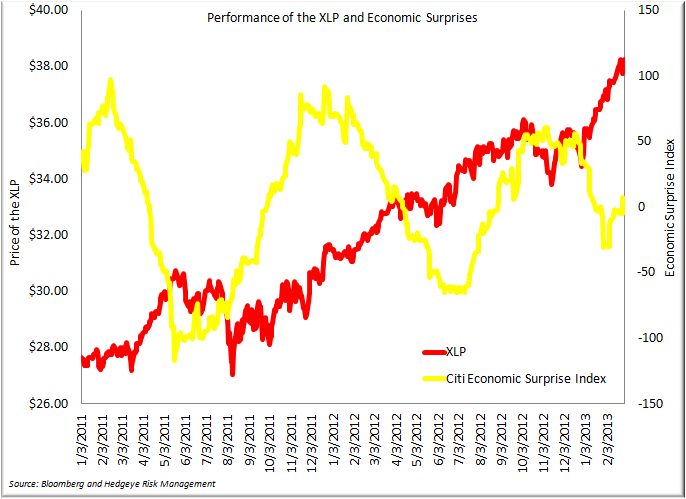

Finally, our "XLP vs. Economic Surprise" chart suggests that continued strength in the economic surprise index could signal a pause for the staples sector.

Where does that leave us?

We are going to focus on three charts - overall sector valuation, "beta chase" and economic surprise. These suggest to us that we could see a pause in the staples sector as sentiment surrounding the broader economy improves, valuation becomes more relevant and takeover speculation recedes. We would look for relative underperformance in the lower quality, lower beta names that have seen a move up in the wake of HNZ (TAP, GIS, CPB). Our most/least preferred list remains relatively unchanged:

Most preferred

- ADM - play on upcoming crop year (BG should work as well)

- BUD - least expensive large cap staples name (replaces STZ on our preferred list due to unfavorable risk/reward)

- CAG - valuation remains compelling, estimates remain too low

- NWL - valuation + stealth housing play

Least preferred

- KMB - robust valuation plus deteriorating earnings quality (CL works here as well)

- TAP - valuation support but zero business momentum

- GIS - run up post-HNZ is unwarranted (CPB eventually, but not yet).