Let's start with the bad news. Street estimates for 2010 are too high. Our database of new casinos and expansions shows that industry slots into this market will decline almost 50% in 2010 from a down 2009. Moreover, IGT's credit facility expires in November, 2010 and we believe the company will refinance by the end of this year at higher rates. These two factors lead us to a 2010 EPS estimate significantly below the Street, $0.82 versus $1.09, respectively. Lower EBITDA drives approximately $0.05-0.10 of the lower estimate with the remaining $0.17-0.22 generated mostly by higher interest expense.

The good news is that IGT has taken out $115 million in costs out of production (see our note from earlier today "IGT: COST CUTTING POTENTIAL") and could reduce SG&A and R&D by a total of $130 million if you believe they can revert back to 2006 levels. IGT is manufacturing at about 35% capacity and with the leaner cost structure, the incremental flow through on accelerating replacement sale should be huge. The question is when will replacement demand accelerate? The North American slot floor is as old as it's been in 10 years. Casino operators' balance sheets need to improve and distressed assets need to be turned over to better capitalized owners before demand picks back up. We believe that won't happen until 2011. By that time, pent up demand could generate huge increases in box sales.

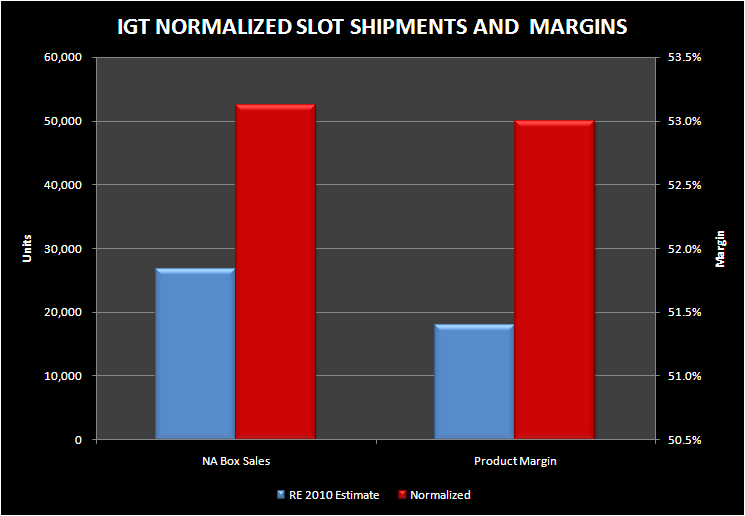

In the following analysis, we attempt to provide a core earnings power estimate for IGT assuming:

- 1) the leaner SG&A/R&D cost structure

- 2) the $100 million of production cost cuts is sustainable

- 3) "normalized" replacement demand

- 4) IGT's market share normalizes at 40%

- 5) IGT refinances its credit facility at an all in rate of 6.5% and raises $500 million in new notes at 8.5%

As can be seen from the analysis, IGT has quite a bit of earnings power. Given the pent up demand, IGT has the potential to "over earn" above the $1.40 for a couple of years should there be a v-shaped recovery.

Investors playing the long-term recovery card could be handsomely rewarded but they may have to be patient. Our 2010 estimate of $0.82 is well below the Street at $1.09. Numbers need to come down before they go up.