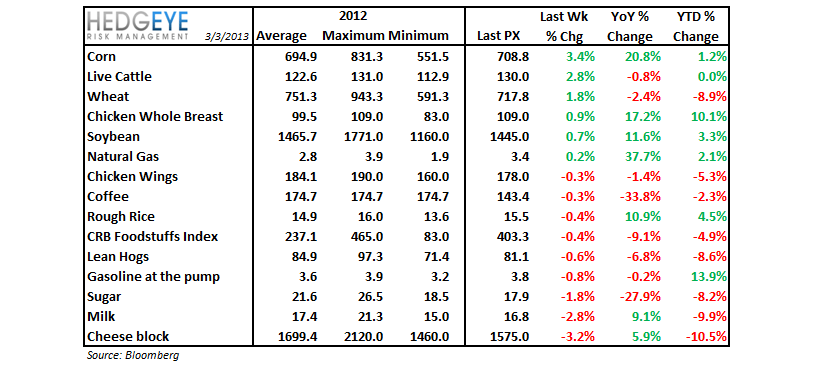

In light of the recent earnings results from the restaurant space, we thought it would be useful to take stock of the commentary on commodity price trends from some of the management teams that, to-date, have reported 4QCY12 results.

DNKN: Franchisees seeing the benefit of lower coffee costs but higher wheat costs persist and could stick around for 2013.

CMG: Company is optimistic that food inflation will be relatively modest over next few quarters. Made no decision on pricing as of 2/5, but said that inflation during the year up to that date made it likely that price would be taken in 2013. Beef and dairy prices were headwinds in the latter months of 2012. Food costs increased faster than expected in the fourth quarter but leveled off in December.

PNRA: Management said on 2/6 that wheat is locked 90% a year in advance. The company is expecting 2-3% inflation. We believe that, on the pricing side of things, achieving significant mix growth (implied in guidance) will be a stretch versus last year’s comparisons.

BWLD: The company is hoping that moderating wing prices will allow it to keep menu price increases to a minimum.

BKW: Commodity inflation is not a crucial issue for this heavily-franchised business model, but the company is expecting 3% inflation in food and paper driven primarily by beef. There were some concerns that elevated beef prices may pressure franchisee profitability, coming alongside some significant capital investment from the franchisee community. The horsemeat scandal has brought beef prices down but, to the extent that the scandal hurts demand in the US, that would be negative for BKW.

BLMN: Bloomin’s management team is expecting FY13 beef inflation in the range of 10-12%, which should be offset, in part, by favorable pricing on seafood. The company is contracted for 72% of its buy for 2013, as of 2/22.

TXRH: Management is expecting beef costs to be up by 15% this year but has 80% of its needs locked in. On the earnings call, continuing tight cattle supplies and the high percentage of corn being used in ethanol production were highlighted as continuing tailwinds for beef prices.

JACK: Management is expecting beef and corn to be up roughly 4% for the year, with chicken up 6%. The company’s overall basket is expected to be up 2-3% for the fiscal year. Beef and corn, according to the company, have the potential to be most volatile.

PZZA: Management is expecting overall commodity costs to be up in 2013, with cheese prices expected to increase throughout the year. Corporate locations tend to hedge on cheese while franchisees tend to be less conservative.

WEN: Management is expecting an increase in the cost of its commodity basket in the range of 3-4% with beef (20% of spend) and chicken (20% of spend) driving the increase.

Howard Penney

Managing Director

Rory Green

Senior Analyst