Summary: 3 Ways the USD Wins

- Fiscal Consolidation: After a multi-decade run of federal fiscal profligacy,any manner of budgetary restraint is dollar supportive on the margin.

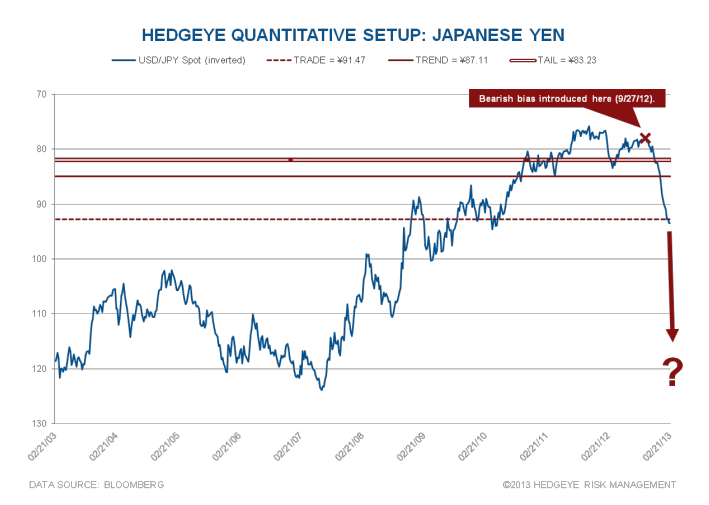

- Taro Aso being Taro Aso: With the dovish actors in place (Aso/Kuroda), the political will supportive, and the appetite there for increasingly aggressive policy initiatives we think the Yen is poised to return to ¥100+ per USD.

- U.S. Growth Stabilizing: Economic fundamentals are USD supportive, on balance, with Housing, Labor Market & Manufacturing activity data all stable to improving. Further Economic weakness across G7 economies should support a relative bid for the dollar also.

- Positioning: Short Yen, Short Basic Materials, Long Consumption

“Why is broad commodity deflation a bullish setup?” – we’ve been fielding some version of that question with greater frequency over the last few weeks as market prices have continued to offer positive confirmation of our strong dollar - strong consumption view, a key underpinning of our #GrowthStabilizing investment theme.

Below we provide a summary recap of our view on the dollar-growth connection, our bullish view on the dollar and why we think there is further upside in the immediate/intermediate term.

THE THINKING:

The Strong Dollar = Strong America mantra continues to anchor our view on sustainable, real GDP growth both domestically and globally. Central to the view is the fact that a stronger dollar drives commodity & energy deflation, serving as a real-time tax cut to consumers and an input cost reduction for business with a flow-through benefit to earnings on a lag.

Because most global commodity transactions settle in dollars, the USD-Commodity Price relationship is rather direct, and the impacts of commodity deflation are felt globally as share of wallet occupied by food and energy declines. The cost deflation and purchasing power impacts are further pronounced for economies with some measure of a currency peg to the U.S. Dollar – fundamentally, we continue to like Hong Kong, China, and Singapore, in part, for that reason.

Persistent central bank policy intervention with the explicit goal of devaluing the currency to drive (financial) asset price re-flation has been a discrete headwind to sustainable dollar strength over the last five years. Investors, on balance, have bought into the policy regime with a primary follow-on effect being that equity and commodity price correlations to the dollar have been strongly and inversely correlated over that same time.

While policy initiatives supported equity valuations (via lower discount rates & a lower dollar) and provided some measure of economic stimulation, commodities and inflation hedge assets generally outperformed other asset classes. With repeated rounds of easing, the investor response became pavlovian with commodity and energy price inflation and lower real, inflation adjusted growth on the other side of those policy initiatives.

As we’ve stated repeatedly, big government policy intervention and the perpetuation of the temporal, Dollar Down --> commodity Inflation Up --> Real Growth down, dynamic has served to:

1. Shorten Economic Cycles, and

2. Amplify Market Volatility.

As a result, we’ve been beholden to compressed economic oscillations and fleeting, episodic periods of growth, while real, sustainable, demand growth has remained elusive.

Can we break the cycle as Bernanke's last Bubble (commodities) deflates?

With QE-infinity on the table, the capacity & appetite for further Fed balance sheet acceleration declining, and domestic growth stabilizing, the potential to break free of the prevailing, policy-inflation-growth cycle that has characterized the better part of the last five years is increasing – with the prospects for sustained USD appreciation gaining concomitantly.

Indeed, at present, intermediate term dollar correlations to the S&P500 are positive while holding negative across the larger commodity basket. Dollar Up, Stocks Up, Commodities Down is the relationship dynamic we’d like to continue to see perpetuate itself with respect to sustainable end demand.

Mother Nature likes redundant systems and we feel comfortable taking an anti-fragile cue from one whose traversed a global cycle or two. Currently, we think the strong dollar thesis can win in 3 ways.

THE FACTORS & HOW TO POSITION:

1. Fiscal Consolidation: After a multi-decade run of debt financed consumption and federal profligacy, Sequestration, or any manner of fiscal restraint & consolidation, on the fiscal policy side is dollar favorable on the margin. Further, given the diminishing return of fed policy action and the reduced appetite for further QE initiatives, QE now appears rearview as a discrete bearish catalyst for the dollar in the near-term.

2. Taro Aso being Taro Aso: We’ve detailed our Short Yen case via our #QUADRILL-YEN 1Q13 Investment theme and on our recent best ideas call (email us if you would like a copy of the presentations). In short, with the dovish actors in place (Aso/Kuroda), the political will supportive, and the appetite there for increasingly aggressive policy initiatives we think the Yen is poised to return to ¥100+ per USD. A weak Yen with an explicit and comparatively dovish policy outlook for Japan vs the U.S. is supportive of dollar strength.

- Positioning: We continue to like the short Yen position on the other side of the long dollar call.

3. U.S. Growth Stabilizing: Economic fundamentals are USD supportive, on balance, with Housing, Labor Market & Manufacturing activity data all stable to improving. Further Economic weakness across G7 economies, particularly across the EU, UK & Japan, should support a relative bid for the dollar in the immediate/intermediate term as well.

- Positioning:

- Short Basic Materials: Materials is the worst looking sector across the S&P from a quantitative perspective and has direct negative leverage to commodity deflation

- Long Consumption: A Real-time tax cut via energy deflation is positive for real earnings growth and discretionary income. We like Consumption oriented/Consumer Facing equities in the U.S. and select Asian equity markets (China, Hong Kong)

- Short Gold: To the extent that U.S. dollar strength is reflective of growth and interest rate expectations (or just the expectation for a cessation in easing) we think gold holds further downside over the intermediate term.

4. Quant: The USD remains bullish and is breaking out from a quantitative perspective. TRADE & TREND Support sit lower at $80.65 and $80.12, respectively.

Christian B. Drake

Senior Analyst