I can drive a truck through the bull case and the bear case on this name. The bulls are winning today on the ‘better than toxic’ results. We’re the first to respect the premise that going from ‘toxic to bad’ is a positive event. And from a modeling standpoint, I think that COH has much in its favor for the next year. But I have too many concerns and questions that still need to be answered before I can get bulled-up over the long-haul. If I gain such confidence, I certainly won’t regret having missed out on another 10-20% move in the stock, so long as it’s clear to me that it will not be cut in half.

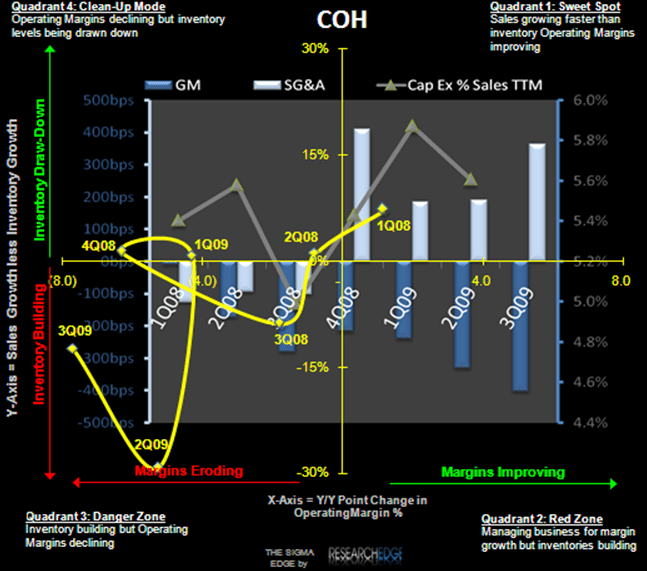

Bull Case: Coach is perceived to be one of the best brands in retail, with meaningful growth opportunity on a global scale. North American comps are getting less bad, with the latest quarter down only 4% yy in a horrible high end retail climate. That’s happening at the same time where we’re seeing a ‘financial’ trifecta on the P&L and balance sheet. Check out the SIGMA chart below, it shows how Gross Margins have been dropping like a stone as SG&A has gone right up in each of the past four quarters. This is at the same time both working capital was squeezed AND capex headed higher. Now each of those factors gets better on the margin for the next year barring a massive stumble by the company. Tack on the new dividend announcement and accelerated stock repo and the stock looks cheapish at 6x EBITDA.

Bear Case: Comps getting ‘less bad’ will only take the company so far given a secularly challenged wholesale business, and the fact that the company is stepping up its efforts to cut costs out of the system. Yes, this helps ’09 optically, but will it be at the expense of ‘10/’11 revenue and Gross Margins? Maybe, maybe not. But the risk will certainly remain, and with margins still at a lofty 30%, there’s no structural support that would preclude them from going much lower. The kicker there is that COH generates 26% of sales in Japan. While many people like the US diversification and the exposure to the Japanese luxury consumer, I’m not in the camp that likes such heavy exposure to an economy that is terminally ill. And this all comes from a management team that does not ‘do macro,’ and has argued in the past that women still need six handbags apiece regardless of the economy. That part of the narrative scares the heck out of me. Has management changed its tune and embraced the cyclicality of its business? Yes. But I have zero evidence or confidence that they are proactively managing it.

Brian McGough