TODAY’S S&P 500 SET-UP – February 28, 2013

As we look at today's setup for the S&P 500, the range is 87 points or 4.42% downside to 1449 and 1.32% upside to 1536.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.64 from 1.66

- VIX closed at 14.73 1 day percent change of -12.69%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:15am: Fed’s Lockhart to speak on banking in Atlanta

- 8:30am: GDP Q/q, 4Q revision, est. 0.5% (prior -0.1%)

- 8:30am: Personal Consumption, 4Q revision, est. 2.3%

- 8:30am: Core PCE Q/q, 4Q revision est. 0.9% (prior 0.9%)

- 8:30am: Init. Jobless Claims, Feb. 24 est. 360k (prior 362k)

- 9am: NAPM-Milwaukee, Feb., est. 52.0 (prior 51.3)

- 9:45am: Chicago Purchasing Mgr, Feb., est. 54.0 (prior 55.6)

- 9:45am: Bloomberg Consumer Comfort, Feb. 24 (prior -33.4)

- 10am: Freddie Mac weekly mortgage-rate survey

- 10:30: EIA natural-gas storage change

- 11am: Kansas City Fed Manf. Activ., Feb., est. -1 (prior -2)

- 11am: New York Fed Executive VP McAndrews holds press briefing on household debt in New York

- 12:30pm: Fed’s Raskin speaks on banking in Atlanta

- 8:00pm: Fed’s Evans speaks in Des Moines, Iowa

GOVERNMENT:

- 9am: House Armed Services subcmte hearing on impact of budget cuts on acquisition, programming

- 10am: Joint Economic Cmte of Congress hearing on state of U.S. economy

- House Judiciary Cmte panel meets on impact of Obama admin regulations on jobs, economy, global competitiveness

WHAT TO WATCH

- Senate plans symbolic votes as $85b budget fight to begin

- Boeing 3-Part fix won’t end 787 grounding quickly, FAA says

- RBS said will sell a stake in Citizens unit in U.S. in ~2 yrs

- Regency to buy Southern Union for $1.5b in shale move

- Wal-Mart U.S. chief administrative officer Tom Mars to leave

- Wal-Mart struggles to restock store shelves as U.S. sales slump

- AOL COO Arthur Minson is said to weigh resignation

- Sierra Nevada, Embraer win U.S. contract with $950m value

- GM said to be targeting up to 20% growth for Volt cars this yr

- Groupon forecast misses ests., raising pressure on CEO Mason

- Ahold to buy back shrs as 4Q profit miss ests.

- Lew confirmed as U.S. Treasury chief plunges into deficit fight

- Tudor said to plan 1st equity funds since Pallotta left in ’09

- J.C. Penney’s lowest sales in decades Show Johnson stumbling

- Abe nominates Haruhiko Kuroda as next Bank of Japan governor

- Draghi says ECB in no rush to tighten policy as inflation slows

- U.S. foreclosure deals drop as lenders approve more short sales

- MGA seeks to revive trade-secret lawsuit claims against Mattel

- MBIA swaps rise as cites “substantial doubt” over unit

EARNINGS:

- Canadian Imperial Bank of Commerce (CM CN) 5:35am, C$2.09

- Catamaran (CCT CN) 6am, $0.35

- Iron Mountain (IRM) 6am, $0.25

- Newcastle Investment (NCT) 6am, $0.27

- Sears Holdings (SHLD) 6am, $0.98

- Valeant Pharmaceuticals (VRX CN) 6am, $1.21

- Visteon (VC) 6am, $0.82

- Royal Bank of Canada (RY CN) 6am, C$1.32

- Toronto-Dominion Bank (TD CN) 6:30am, C$1.93

- Ocwen Financial (OCN) 6:34am, $0.50

- Kohl’s (KSS) 7am, $1.63

- LKQ (LKQ) 7am, $0.23

- WPX Energy (WPX) 7am, $(0.08)

- MGIC Investment (MGIC) 7am, $(1.67)

- ANSYS (ANSS) 7:09am, $0.74

- Chico’s FAS (CHS) 7:15am, $0.20

- AltaGas Ltd (ALA CN) 7:30am, C$0.47

- Domino’s Pizza (DPZ) 7:30am, $0.60

- Halcon Resources (HK) 7:30am, $0.03

- George Weston (WN CN) 8am, C$1.09

- Cablevision Systems (CVC) 8:30am, $0.09

- Rowan (RDC) 8:45am, $0.48

- Deckers Outdoor (DECK) 4pm, $2.58

- Esterline Technologies (ESL) 4pm, $0.61

- Gap (GPS) 4pm, $0.71

- Sotheby’s (BID) 4pm, $1.10

- Kodiak Oil & Gas (KOG) 4:01pm, $0.13

- Molycorp (MCP) 4:01pm, $(0.30)

- New Gold (NGD CN) 4:01pm, $0.13

- Universal Health Services (UHS) 4:01pm, $0.93

- Salesforce.com (CRM) 4:05pm, $0.40

- SandRidge Energy (SD) 4:05pm, $0.00

- Splunk (SPLK) 4:05pm, $0.02

- Medivation (MDVN) 4:09pm, $(0.46)

- McDermott International (MDR) 4:10pm, $0.23

- Mentor Graphics (MENT) 4:10pm, $0.55

- Omnivision (OVTI) 4:18pm, $0.41

- Integrys Energy Group (TEG) 5:07pm, $0.95

- National Bank of Canada (NA CN) 6pm, C$2.02

- Endo Health Solutions (ENDP) Post-Mkt, $1.55

- Great Plains Energy (GXP) Post-Mkt, $0.02

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

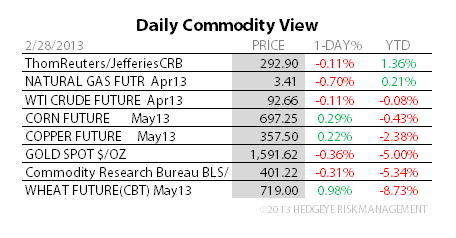

- Gold Heads for Biggest Monthly Drop Since May as ETPs Slide

- Rhodium Beating Platinum to Palladium on Car Sales: Commodities

- Wheat Rises as U.S. Export Demand May Increase After Price Drop

- WTI Oil Set for First Monthly Drop Since October as Supply Rises

- Copper Swings Between Gains and Declines Amid Lack of Demand

- Coffee Extends Gains in London on Reduced Sales; Sugar Advances

- Palm Seen Dropping to Four-Year Low on MACD: Technical Analysis

- Gold Demand in India Seen Rebounding After Import Tax Maintained

- Coffee Exports From Indonesia Dropping Even With Record Crop

- Mongolia Plans to Charge Rio’s Oyu Tolgoi Interest on Tax

- Shell Sees Solar as Biggest Energy Source After Exiting Industry

- India Left Gold Taxes Unchanged as Imports Continue, Group Says

- Investors Dumping Gold Means Slump to $1,400: Chart of the Day

- Palm Drops to Six-Week Low as Malaysian Inventories to Stay High

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team