“Not this week, thank God.”

-Dwight D. Eisenhower

That’s what the President of The United States said to one of his senior advisors “with beads of sweat on Eisenhower’s forehead during the tense debate over whether and when to intervene” in Vietnam in 1954. (Ike’s Bluff, pg 131)

As many of you know from your risk management experiences, it’s what you don’t do under pressure that often defines your performance. “Eisenhower was an expert in finding reasons for not doing things recalled Andrew Goodpaster.” (pg 130)

That’s why I study the history of great leadership. It helps me empathize with and learn from what Teddy Roosevelt called “the struggle” of other men and women when they were under pressure. It also gives me confidence in making decisions. That doesn’t always mean I’ll make the right call. It just means I’ll have known why I made it.

Back to the Global Macro Grind…

Eisenhower’s legacy is that he didn’t let the French suck US casualties into Vietnam in 1954. He also avoided playing the end of the world card (releasing the bomb) during a time when plenty of Americans had US politicians (LBJ) freaking them out about outer space.

If the world ended this morning, I am pretty sure A) I wouldn’t be writing this and B) you wouldn’t be reading anything else. So, with that in mind, and the entire manic media focused on what is so 2010-2011 (Italian Bond auctions), what happened?

- Italian Bond Auction was better than “expected”, so bond yields fell, making another lower long-term high

- Italian Equities stopped going down right at our immediate-term TRADE oversold signal of 15,511 (MIB Index)

- US Equity Futures held onto yesterday’s gains; the 2nd up day in the last 3 (+4.9% YTD)

I’m not trying to be complacent about Italy’s economic risks (just don’t be long Italy, and get over it). I’m well aware of what Eisenhower himself coined as The Domino Theory. We made this call on Europe around this time in Q1 of 2010 don’t forget. It’s 2013, and we don’t see Italy being the domino that knocks down our bull case for Asian and US Equities right now.

That could change. The plan is always changing. And when it does, I’ll be the first to let you know. But, for now, let’s focus on doing more of what we did when people were freaking out about Congress at the end of December:

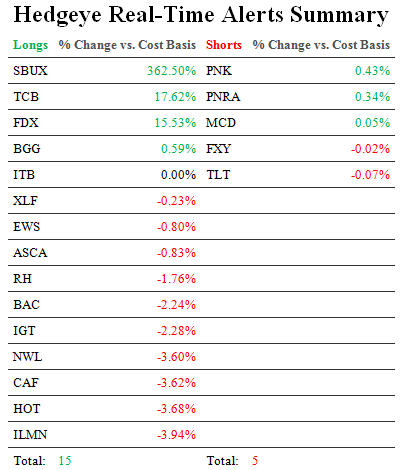

- Buy Asian (China and Singapore) and US Stocks (EWS, CAF, XLF)

- Short US Treasuries (TLT)

- Short Japanese Yen (FXY)

Why buy American instead of Italian?

- US #Housing is ripping (New Home Sales shocked the bears to the upside yesterday with inventory falling, again!)

- US Employment #GrowthStabilizing (our rolling non-seasonally adjusted jobless claims model continues to be bullish)

- If you have to choose between a criminal, comedian, and Congress, I’d actually choose Congress

Yep, that’s how sad and embarrassing Italy’s #PoliticalClass has become. And neither France nor Japan are too far behind them.

So, if you are shorting Treasuries, can’t buy European or Japanese Sovereign Debt, and have to buy something else, why not Asian or American stocks? To be clear, I don’t have to buy anything. But when I do buy something, both the signal and research back it.

The last point I want to make this morning is about volatility expectations. I get the front-month VIX is different than the term-structure of volatility’s curve. Looking at expectations, across durations, will amplify my point:

- VIX (front-month) TREND resistance = 17.18, and that was only violated to the upside for ½ a day

- VIX topped on Monday at another lower long-term-high (on DEC28, 2012 the lower-high = 22.72)

- VIX was at 40 in Q1 of 2010 after we were legitimately concerned about European Dominos

As you can see in the Darius Dale’s Chart of The Day, front-month Volatility (VIX) continues to make a series of long-term lower highs as the volume of the manic media’s freak-outs make higher-highs. Think they’ll make the call on the end of the world, together?

If this is just a mini-mania of what you saw in November-December (substitute Italy for US Congress), what is it, specifically, that you have a as a catalyst that would stop the VIX from going straight back down to 12 from here?

It’s not going to 12 this week. I get that. But the VIX is probably not going back to 22.72 or 42.96 (the SEP2011 freak-out) this week either. If I see anything real developing that changes my view on this, I’ll just change my mind. I don’t have to do that yet, thank God.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST10yr, Shanghai Composite, and the SP500 are now $1, $112.55-116.12, $81.12-82.23, 91.55-94.49, 1.84-1.96%, 2, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer