IGT spent $130 million more in 2008 on SG&A and R&D than it did in 2006, on a big slot revenue decline and flat total revenues. Why can't IGT revert back to its 2006 cost structure? The answer: IGT needs a push. We don't yet know if Patti Hart is the right person although she certainly brings a fresh and more importantly, unemotional perspective.

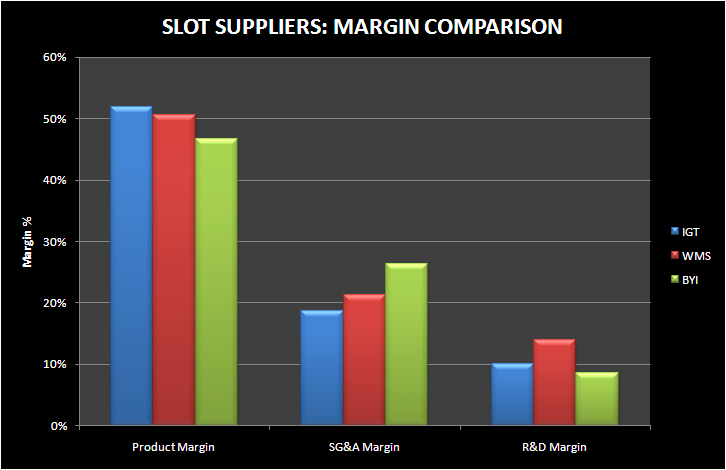

The following chart compares various margins for IGT, WMS, and BYI. On the surface, it appears that IGT's margins are reasonable and the company's cost structure is not necessarily bloated.

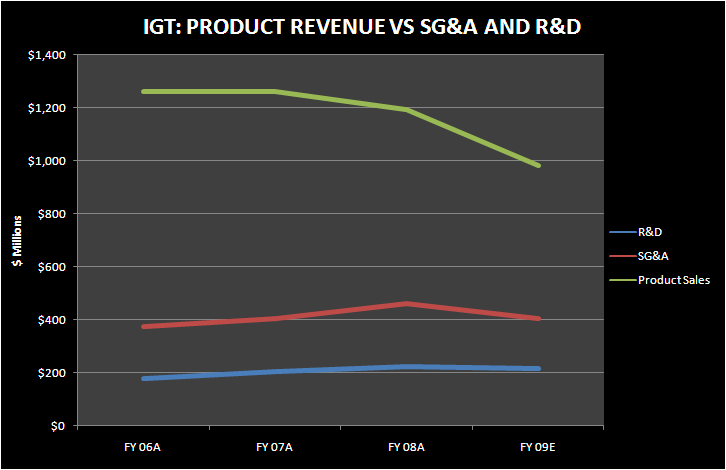

However, the next chart shows that SG&A and R&D spend is up 23% and 26%, respectively, in just 2 years on a big decline in product sales.

IGT indicated that it has already cut $115 million in costs in the past year so the obvious question is how much more is left? Fortunately, those cuts were made at the production level and more than offset the usual margin decline associated with declining volumes. Gross margin would've otherwise cratered with sharp decline in units. Instead, product margins have expanded in the face of dismal sales as can be seen in the following chart. Some of that is increased non-box sales (higher margin conversions, software, etc) and higher pricing, but also reflects the $115 million in cost cuts. IGT's manufacturing is running at about 35% capacity, leaving a lot of margin on the table until replacement demand reaccelerates. Since IGT owns its manufacturing plant and has made the production cuts, margins are likely to follow volume from here on out.

It is in SG&A and R&D where the real opportunity lies but management needs to be aggressive. We think it is reasonable to expect $100-130 million more in cost savings out of these areas:

- $75MM gets them back to 07 levels, $130MM back to 06

- Should take 6 quarters to achieve the cuts, seems like they know where some will come from, and are feeling their way around the others - the new CEO could expedite this

- $15MM of the $100MM will show up this quarter, and it should be visible in SG&A and perhaps R&D

- New R&D projects will now require demonstrable ROI

- First round of cuts are in place and are a kind of "restructuring" - cleaning house to do things better rather than just get across a goal line

The bottom line here for IGT is that the cost cuts will offset some of the top line pain but earnings are likely going lower. Slot sales will be abysmal with new and expansion units for the industry down 53% and 49% in calendar 2009 and 2010, respectively. Replacement demand probably won't improve until 2H 2010 at the earliest. The upshot for IGT is by that time the cost structure should hopefully be very lean and more appropriate for a 40% share company versus the historical 60-70%. IGT will be in good shape in terms of flow through when replacement demand finally "normalizes".