With no one party receiving a true majority across both houses of parliament in yesterday’s vote, it appears we’re set for either another round of elections or the initial days to formulate a grand coalition. We give the latter significantly less probability because we believe the strong voting results for the Berlusconi and Grillo parties across the upper and lower houses will create more polar factions (particular on the fiscal agenda) and therefore less opportunity for fruitful coalition building, that is to say a coalition not hampered by political gridlock. Remember the party platform of Grillo’s Five Star Movement has been one to not form a coalition.

Below we refresh a number of charts to highlight the broader, challenged economic fundamentals of the country. Our call here is that the uncertainty around the election (another vote or a grand coalition), especially with the likely prospect of Berlusconi renewing his political powerbroker license, should add further downside pressures to many of the charts.

Given that coalition talks are officially not supposed to take place until the presidents of the lower and upper houses have been elected on March 15, there’s a good runway of political uncertainty ahead that we expect should lead to more downside across Italian capital markets and put pressure on the EUR/USD.

----

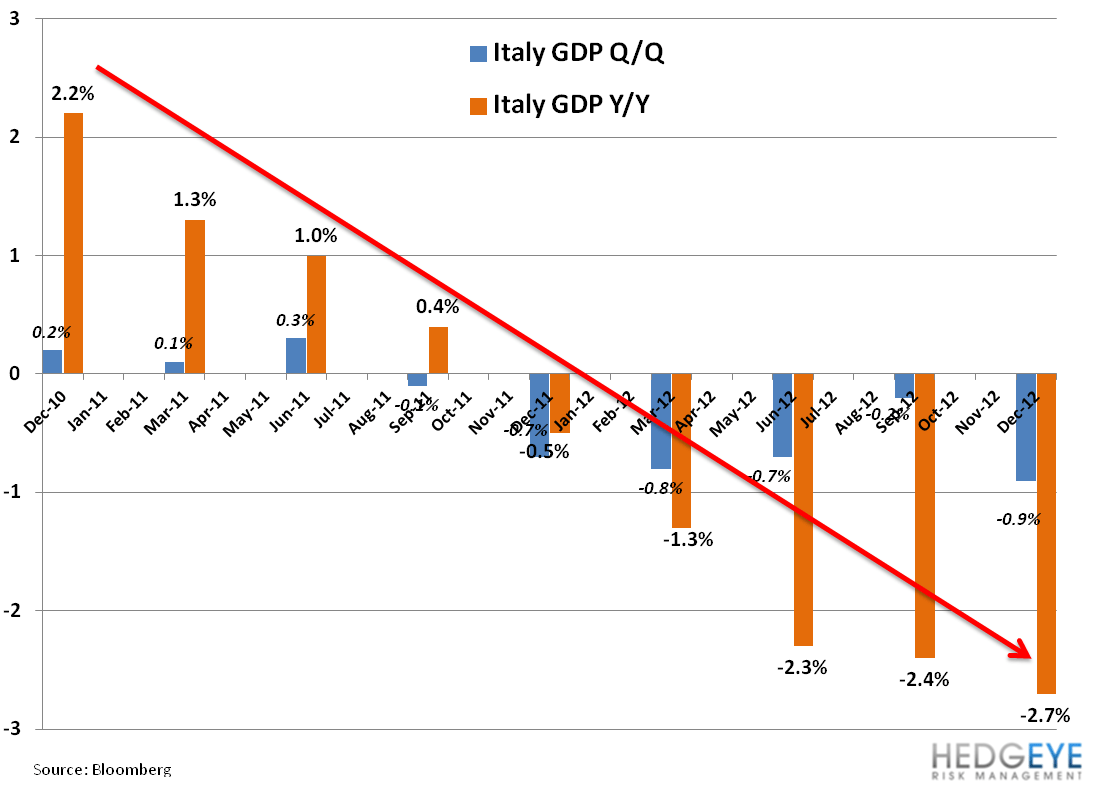

Growth Slowing - As the data from Reinhart and Rogoff shows, when a country’s sovereign debt load exceeds 90% (of GDP) growth is dramatically impaired. We think the market will continue to punish Italy at 120% via higher servicing costs. Interestingly Italian yields have ticked lower since ECB President Mario Draghi called to buy “unlimited” sovereign debt via the OMT program on 9/6/12. We think the political uncertainty should boost yields and may materially challenge investors’ perception that Europe is 'healed'.

Hockey Stick Risky Profile – Yields and CDS have popped since the election results became more clear yesterday (2/25). The 10YR yield is at 4.90% and the spread over German Bunds is up 57bps since Friday (2/22).

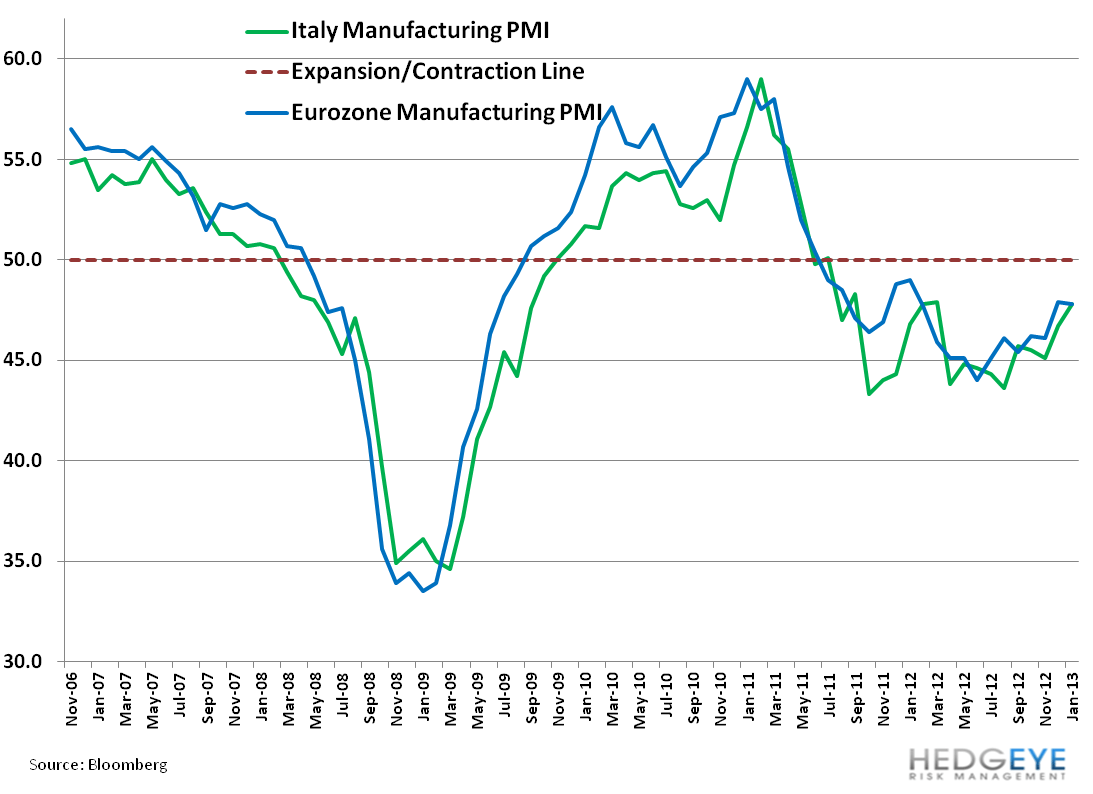

Underperforming Growth - A major leading indicator for growth is derived from PMI surveys. As the two charts below indicate, Services PMIs are well under the Eurozone averages and along with Manufacturing have been under the 50 line that divides expansion (above) and contraction (below) for 13 and 18 straight months, respectively.

Labor Cost Inefficiencies - A major factor behind Italy’s slower growth profile is stagnation in its productivity, witnessed by higher unit labor casts, while wages, despite declines, have yet to turn negative.

Industrial Production – Slowing and underperforming continued. In a European Commission paper reviewing Italy, the report noted that stagnation in production is the key factor behind Italy’s loss of cost competitiveness since the euro adoption.

Unemployment Hooking - Another grave dynamic is the underemployment across Italian youths at 37%. While short of the 52% for Spanish youth, combine “a lost generation” with Italy’s demographic headwinds of an aging population (near oldest in Europe) and you have a cocktail that puts great pressure on social services, and the debt and deficit loads in the years ahead.

Smashed Piggy Banks - The Italian household savings rate moved from a high of 17.8% in mid 2002 down to 11.6% as of Q3 2011. The chart shows that Italians leveraged their savings in the upturn and in the downturn. The tapping of savings in the last three years demonstrates to pay off debt and the resilience of the Italian consumer to maintain previous spending levels.

Confidence Down - Italian economic sentiment has trended lower since mid-2011.

Retail Sales Down - decidedly down.

New Car Registrations Down - Yet another metric we follow. Here again, no surprise, underperformance vs the EU average.

Square Stagflation - While we expect inflation to moderate in 2013, but currently at +2.4% Y/Y, sticky stagflation continues to be a tax on a citizenry already feeling crushed by austerity.

Matthew Hedrick

Senior Analyst