This note was originally published at 8am on February 12, 2013 for Hedgeye subscribers.

“Every gun that is made, every warship launched, every rocket fired, signifies in the final sense a theft from those who hunger and are not fed, those who are cold are not clothed.”

-Dwight D. Eisenhower

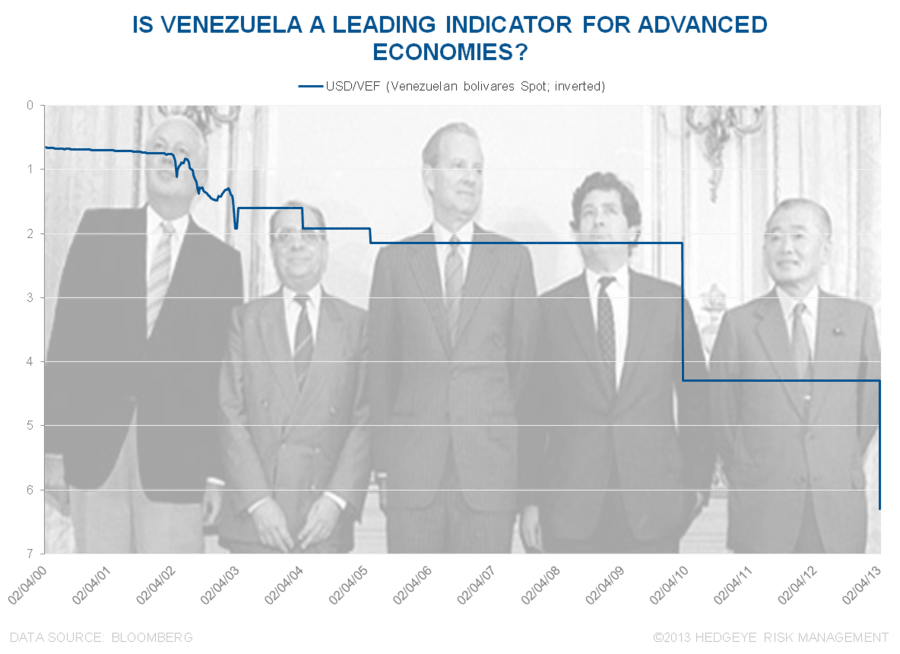

As I was preparing for my week long sojourn over to the United Kingdom, I actually had to think seriously about what type of currency I wanted to bring. After all, in this day and age of the modern currency war, the movement of currencies can be dramatic and shocking. If you don’t believe me, just ask those good folks that were long of Venezuela’s Bolivar going into Friday. In a split second, the government unilaterally devalued the Bolivar by 32% and likely put a few currency traders out of business.

In terms of global economies, according to the CIA Fact Book Venezuela is just the 34th largest economy in the world at just $400BN in annual economic output. Despite this, there were a number of multinational companies that were impacted by the devaluation. Specifically, Colgate-Palmolive and Smurfit Stone have taken charges, with comparable companies like Avon, Proctor and Gamble and Kimberly-Clark certainly at risk of a short term hit to both earnings and assets.

Obviously the popular pushback when we stress currency wars with U.S. focused equity managers is that they are a 3rd world type risk and not a concern or issue that will become broadly prevalent. In fact, this consensus view was verified to me as I opened the Irish Times this morning to an article titled, “Fears of an Imminent Currency War Are Wide Of the Mark.” Of course, many of these money managers have only been managing money for the last 10 – 15 years, so they may have missed this little critter called the Plaza Accord.

Now admittedly, the Plaza Accord was not a unilateral devaluation or war, but rather an agreement by Germany, Japan, France, the United States, and the United Kingdom. The agreement by these five nations was to intervene in global currency markets with an objective of devaluing the U.S. dollar in relation to the Japanese Yen and German Deutsche Mark.

Not surprisingly when the world’s largest central banks gang up to achieve a goal, they succeed, and the U.S. dollar depreciated dramatically over the next two years. In fact, the dollar depreciated versus the yen by almost 50% from 1985 to 1987. By some economists, this devaluation was heralded as a glorious success as the devaluation was controlled and did not lead to a financial panic.

While the last point is true, the strengthening of the Japanese yen was likely a key catalyst for one of the most significant bubbles of the last three decades, if not hundred years – the Japanese real estate bubble. Naturally, given that the U.S. dollar was set to decline, the Japanese that had their assets abroad repatriated and began purchasing Japanese real estate, and purchased more, and purchased more. In fact, at one point choice properties in Tokyo’s Ginza district were trading hands at $20,000 per square foot.

For Japan, the acquiescence to the United States to devalue the U.S. dollar led to an asset bubble of incomparable proportions and then an effective lost decade(s) of economic activity (and then some) as the Japanese economic system de-levered. My point in highlighting this is simply that devaluations, like much of government intervention in the markets, has unintended consequences. In hindsight, the Japanese likely never would have signed up for the Plaza Accord had they understood the unintended consequences. In part, this experience is likely shaping their new policy of going at their currency strategy alone, rather than suffering the beggar thy neighbor option of a Plaza Accord type agreement.

There is obviously a worst case scenario as it relates to currency wars, that scenario in which all nations devalue at once. Not unlike during the Cold War, when both the Soviets and Americans were armed to the hilt with nuclear weapons, this global devaluation is also likely a race to MAD (Mutually Assured Destruction). For lack of a better term, we’ll call it Currency Armageddon.

The broad implications of a massive global currency war actually relate back to the quote from Dwight Eisenhower at the start of this note. In a normal war, goods are taken from the people to create weaponry. As a result, the average person is worse off during a war. On some level, a currency war is no different.

As currencies are devalued, the purchasing power of the average citizen is degraded and as a result so is their ability to purchase basic goods. If you don’t believe me, ask the average citizen of Venezuela whose purchasing power was decimated by this move on Friday. This quote from a recent Bloomberg article about a rush to buy airline tickets was particularly apropos:

“I came because I heard American Airlines is going to raise fares by 100 percent, that’s to say, above the devaluation.”

Interestingly, there is an alternative to Currency Armageddon and its unintended consequences. This is the exchange rate system implemented post World War II called the Bretton Woods system. In this period of semi-fixed exchange rates, competitive devaluation was not an option. Not surprisingly, under Bretton Woods global economic activity thrived and was stable.

This is not to say that Bretton Woods was an ideal system, but what seems less than ideal is the ability of major governments to unilaterally devalue on a whim, which is the nature of the monetary system today. The most recent example of this is of course Japan and the rampant devaluation of the yen. This will last until the average retiree in Japan starts to feel the fiat currency squeeze like the Venezuelans have. Interestingly, Japan is almost half way there with a Yen that is down over -15% in only three months.

Now, on one hand, shorting the yen was an existing idea we re-presented on our Best Ideas call on November 15th and that trade is up ~14% since then, so we are happy about that. But as we contemplate risk managing future economic shocks, the idea of Currency Armageddon is a risk that every day seems less and less like a tail risk and more like a 2013 type event, despite what we might be reading in the Irish newspapers.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, and the SP500 are now $1641-1669, $116.52-118.72, $79.82-80.54, 92.78-94.66, 1.93-2.01%, and 1507-1523, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research