Investor conviction remains capricious, two down days do not a bear market make, and known unknowns don’t matter until they do – as evidenced by the resurgent concerns over sequestration and sustainability of consumer demand in the face of rising gas prices and negative tax adjustments.

Below we highlight some of the recent consumer related data points & where we shake out, on balance, from an investment positioning perspective.

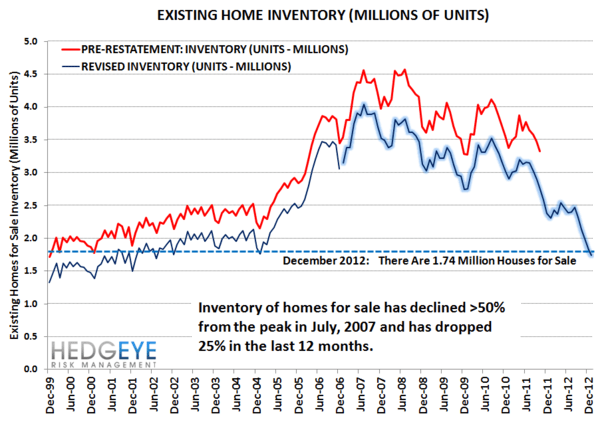

Housing: Yesterday’s Housing Inventory & Price data was decidedly positive. Existing Home Inventory, a primary leading indicator of future prices, declined 24.7% y/y to 1.74M units and now sits some 50% below the 2007 peak. Inclusive of today’s inventory data, our pricing model now points to a 13.2% increase in home prices over the next year.

On the other side of tight supply is pricing and the NAR reported median home prices rose by 12.2% y/y in January, marking a 13th consecutive month of acceleration. To the extent that housing price-demand dynamics are reflexive, which we believe they are, rising prices should drive demand which, in turn, should drive further pricing gains as a virtuous demand-price cycle that characterizes Giffen goods plays itself out.

A continued rise in home prices holds the potential for stimulating a broad based wealth effect with positive impacts for consumer demand. CBO has previously estimated the impact of a 10% decline in home prices to be $55-191B with respect to consumer spending and -0.4 to -1.4 percentage points with respect to GDP growth.

Conversely, realized TTM home price gains and a further continuation of current pricing trends could be expected to contribute +40bps, on the low end, to end consumption over the NTM. Increased housing wealth and the flow through to consumer spending sits as perhaps the largest potential, discrete offset to the -0.45% to -0.55% expected drag on GDP from sequestration.

Source: Hedgeye Financials

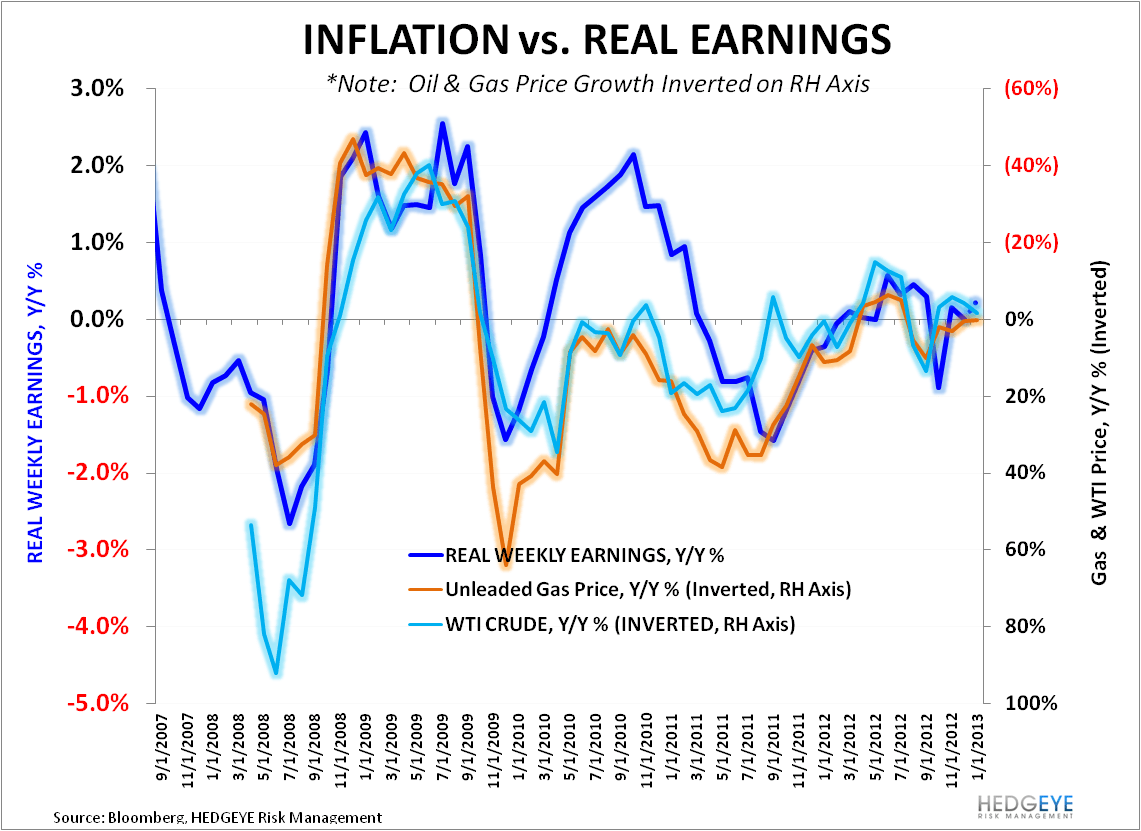

Real Earnings: Yesterday's BLS data showed Real Weekly Earnings accelerated to +0.27% y/y in January. While its hard to pin a bullish thesis on that level of anemic wage growth, on the margin, 3 straight months of positive growth are better than the negative growth in real wages that has characterized the better part of the last two years.

Oil/Gas Prices: Commentary around the consecutive days of rising gas prices streak has showered ubiquitously from financial media sources over the last week. Indeed, Oil prices having been sitting as the largest remaining macro headwind to domestic and global consumption growth, in our view. The last two days, however, have seen energy prices inflect to the downside. From a quantitative perspective Brent Oil has is broken TRADE with immediate term downside to $112.59.

The inverse relationship between USD appreciation and energy and commodity deflation remains pronounced across durations, and with the U.S. dollar still bullish in our model, the balance of risk remains to the downside for Oil prices and, in turn, gas prices on a short lag. Real Earnings growth should benefit by extension as well as the inverse relationship between real earnings growth & commodity inflation over the last 5 years has been distinct.

As a reminder, our most basic US dollar based economic flow model remains:

USD Higher --> Energy/Commodities lower --> Real Earnings/Real Growth Higher

As simplistic as this is, it’s the factor dynamic we’d like to see perpetuate itself for us to remain constructive on sustainable, real growth from here.

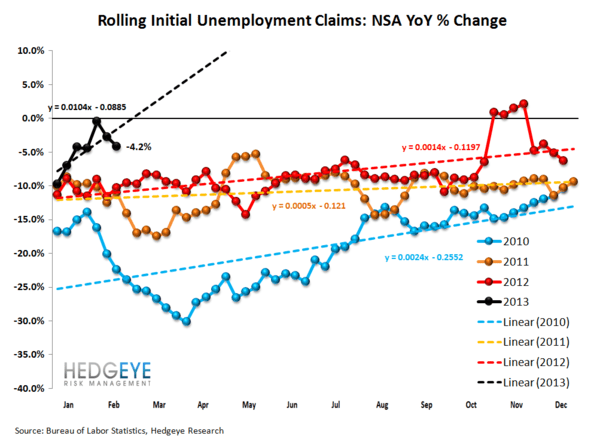

Jobless Claims: Yesterday’s initial Claims data confirmed that labor market trends continue to strengthen as the 4-week rolling average in NSA claims registered further sequential improvement, printing at -4.2% Y/Y vs. -2.7% Y/Y the previous week.

Source: Hedgeye Financials

Income Tax Refunds: The delay in the IRS processing of income tax refunds, and the impact to consumer spending, has been the other favorite media talking point of late. To put some numbers around it, as of the latest treasury data (feb 19th), individual income tax refunds are down $27.26B y/y (down 24.2%) while business tax refunds are essentially flat y/y. The delay in refund processing may be exaggerating any existent weakness stemming from the payroll tax increases, but this is ultimately a timing issue. Any related weakness should resolve itself and reverse over the next few months.

Federal Tax Receipts: Withheld payroll taxes are up greater than 10% fiscal YTD (against a run rate of ~2.5% for most of last year). The move higher is partially explained by a pull-forward in compensation in December ahead of impending tax law changes and partially explained by the actual, enacted tax law changes in January. We’ll have to wait on the February Treasury Statement to get a clearer read on income growth as the confluent impact of these dynamics wane, but Net-net, income tax receipt growth looks like its running 50-100 bps ahead of last year’s pace. We’ll get the February update on 3/12.

On balance, with housing & labor market trends remaining positive and energy prices breaking down alongside a bullish setup for the dollar, we remain positive on domestic consumption.

Christian B. Drake

Senior Analyst