I'm a fundamental analyst so I sometimes look to Keith McCullough's multi-factor model when it comes to entry points. Here are some of his comments:

The multi-factor approach:

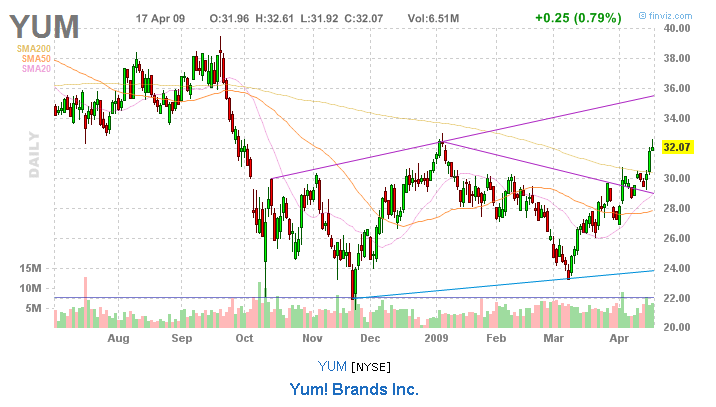

YUM- Stock is getting overbought but is bullish on both TREND ($28.61) and TRADE, with immediate term TRADE momentum building in a support line up at $30.21. Over $33 and it looks like it's worth a shot on the short side, playing for that $30.21 draw down to support. Short interest is very low, so timing here is everything.

The fundamentals:

YUM- As I said last week, I don't expect YUM to miss Q1 numbers but as always the quality of EPS will be low. Domestically, KFC is terminal; Pizza Hut is struggling (along with the category); that leaves Taco Bell to carry the day domestically. With the USA representing more than 40% of operating income, I'm not going to take that to the bank. Given the commentary from MCD and BKC, the international markets have slowed significantly, which suggests that YUM international will post some very punk numbers. That leaves YUM's Holy Grail, China, to save the day; China looks like it will be a challenge, too (please refer to my April 16 post titled "YUM - China, Not Without Issues" and my April 17 post titled "YUM - Lots of Questions" for more details).

Management set the bar low for Q1 expectations so the street is already expecting EPS to decline 4% year-over-year. The street's FY09 EPS consensus estimate, however, also implies 9% growth, which means the street is expecting a recovery in 2H09 as management guided. This growth relies heavily on a U.S. turnaround, particularly at KFC and continued strength out of China on tough comparisons, both of which may be difficult to achieve. Again, I don't necessarily question whether YUM will achieve its targeted 10% FY09 EPS growth goal but more the quality of that earnings growth. As always, YUM will make its numbers through financial engineering; pushing system wide sales and new unit growth through increased capital spending and potentially buying back shares in 2H09.