In 2009, at the height of the financial crisis, the theme of the Darden Analyst Meeting was “Riding Out The Storm”. The company could recycle that theme for this year’s Analyst Meeting but the company’s recent troubles have been self-inflicted.

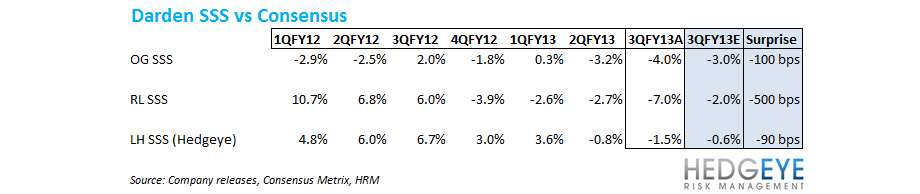

This morning, Darden guided to 3Q EPS of $1.00-1.02 versus the Street at $1.12. We continue to expect EPS of $3.00 for FY13 versus $3.39 consensus. The table below highlights the shortfall, in terms of consensus, of the pre-released same-restaurant sales results released by Darden this morning.

Capital Allocation

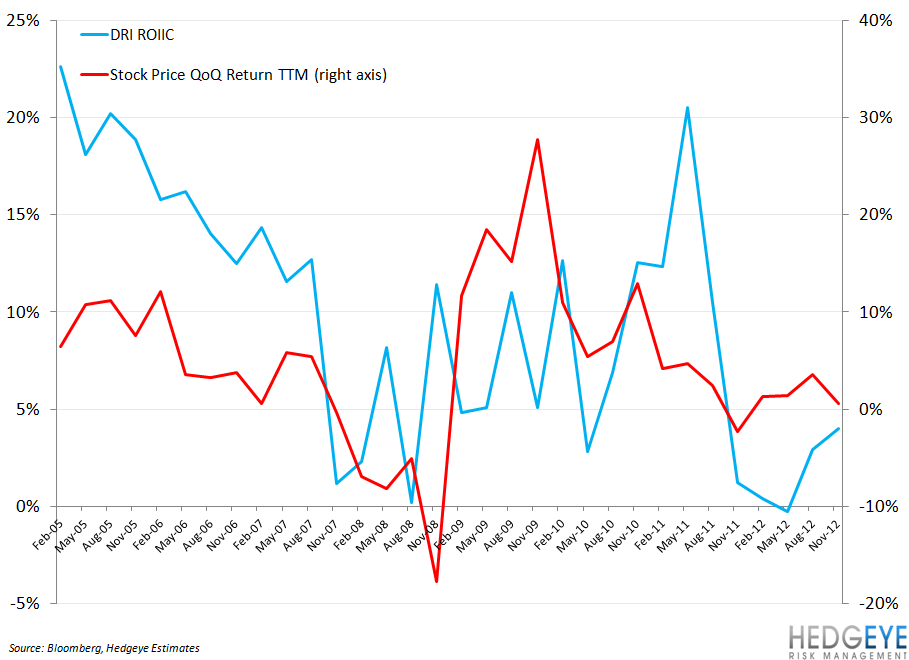

For a company of Darden’s size, following a growth mandate, it’s important for the company’s shareholders that the Return on Incremental Invested Capital metric is not declining steadily over time. As the chart below illustrates, that has been the case. For our position on the stock to change, we would need to see a stop to the growth of The Olive Garden and Red Lobster concepts and a slowing of the growth of LongHorn Steakhouse. This will enable management to improve operations and restaurant-level performance. We estimate that, since the end of 2009, Darden has spent over $2.35 billion in CapEx to generate only $198 million in incremental EBITDA. That is not sustainable and shareholders should be seeking a change in philosophy from management: from “growth” to “prudent capital allocation”.

Cutting the Fat

Darden has a hefty corporate structure, which is appropriate given that it manages over 2,000 restaurants within eight different concepts. In trying to gauge whether or not the company is run efficiently, we have considered SG&A spending per store versus other operators within the industry. While the G&A of Brinker may not be completely comparable to the SG&A line item of Darden, it is interesting to note that the aforementioned line item of Darden’s, on a per store basis, is almost twice that of Brinker, also on a per store basis. If Darden can approach the efficiency level of Brinker in terms of its SG&A spending, we estimate that the benefit could be as much as $400 or $2.25 per share.

Whale Hunting Private Equity Firms

If difficult decisions are not made, it is likely that this company ends up in the hands of private equity with the company being broken into two pieces: Olive Garden and Seasons 52 (Italian) and Red Lobster, Eddie V’s and LongHorn (Steak and Seafood). The other brands would likely be sold with Yardhouse going public. To-date, there has been little pressure on management from shareholders to make any difficult decisions but, as the stock price goes lower, pressure is sure to follow.

The Upcoming Analyst Day

We are expecting management to stick with the party line during the Darden Analyst Meeting next week:

- New Menus at Red Lobster and The Olive Garden

- Remodel initiatives at The Olive Garden

- Discounting

- New leadership at the brand level

- Inflation expectations

- Growth initiatives

- Supply chain efficiencies

We will know more about management’s vision for the future next week. Unfortunately for those that own the shares, we don’t anticipate an increased focus on the core business and the issues therein. We expect $3.00 in EPS for FY13 versus consensus of $3.39. The road to recovery is not going to be easy for Darden but getting serious about fixing the core business is the sign that they are on the way.

Howard Penney

Managing Director

Rory Green

Senior Analyst