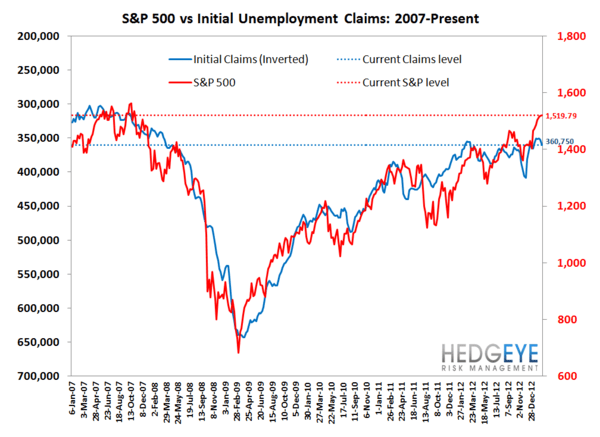

For the second week in a row, the Department of Labor has put out data that shows underlying improvement in the labor market. The 4-week rolling average of non-seasonally adjusted claims, which we consider to be a more accurate representation of the state of the labor market, were down -4.2% year-over-year which is a sequential improvement versus the previous week's YoY change of -2.7%. This is good news, as it signals that the real labor market is, in fact, still strengthening.

Last week’s data was distorted by the incorporation of estimates for Connecticut and Illinois as both state offices were closed due to the snowstorm and unable to report official figures - meaning we had to wait for this week's data for a true update on the underlying labor market trend. All in all, the labor market shows solid signs of improvement