The Cheesecake Factory should continue to outperform its peer group in casual dining. The stock has underperformed the market of late as broader industry concerns have weighed on sentiment but we continue to see this as the best long opportunity in the category.

Macro Challenging But Company Performing

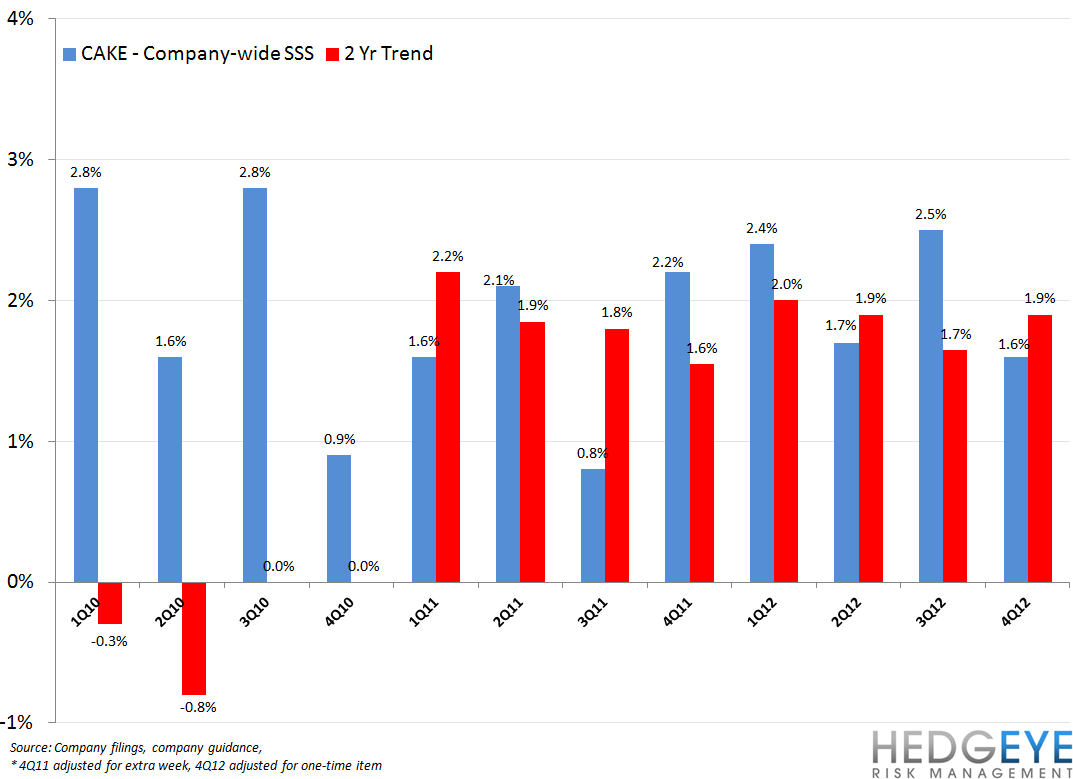

While the macro environment remains difficult, The Cheesecake Factory continues to perform strongly from a top-line perspective. 4Q12 same-restaurant sales grew 1.3% at The Cheesecake Factory and declined -3.2% at Grand Lux Cafe. Consensus was looking for +1.7% and -1.6%, respectively. Overall comps grew 0.9% but there was a -60bps impact from Hurricane Sandy. The consolidated comp, excluding the impact of Sandy, is estimated by management to have been 1.5%. The Street was looking for 1.5% system same-restaurant sales in 4Q. We believe the strong performance in 1Q, while facing strong macro headwinds, is a positive indication of the strength of CAKE’s business.

Showing Resilience in Difficult Macro

While the stock price reacted negatively to the company guiding below Street expectations, the same-restaurant sales performance versus the Knapp Track industry benchmark was approximately +160bps. The company guided to 0-1% comparable sales growth in 1Q13, including one-time items impact of 95bps. Our expectation, based on casual dining trends in 1Q to-date, is for that outperformance versus Knapp to sequentially expand in 1Q by 0-50bps. Over the last few quarters, CAKE has established strong outperformance versus the industry and we expect that to continue in 1H13.

The management team faced down three questions on the earnings call on current sales trends. Despite the noise in the 4Q12 results and difficult comparisons versus a 53rd week in 2011, the underlying business trends of this company have been in line with our expectations.

International development should continue to drive a greater portion of earnings growth, expanding margins over time. The company announced a new international development agreement yesterday while reporting that the sales performance of the international restaurants is exceeding expectations.

Margin Expansion Story Intact

Restaurant-level margins expanded by 90bps in the fourth quarter and we expect continuing margin expansion throughout 2013 as food cost inflation expectations are declining. International growth, as we mentioned above, should also add to the growth of operating margins this year.

Attractive FCF Yield

Cash flow from operations was $195 million in 2012. The company allocated roughly $86 million to capital expenditure, implying free cash flow of $109 million for the year. We estimate that 2013 free cash flow will come in at roughly $100 million, which implies a FCF yield of ~6%.

Outlook

For 1Q13, comparable sales growth is being guided to as 0-1%, including the closure of a Hawaii location due to fire and snowstorm Nemo in the Northeast. The combined impact is estimated to be 95bps. Adjusting for the impact of the storm, underlying trends at The Cheesecake Factory seem to be accelerating on a two-year average basis.

1Q13 earnings guidance is $0.40-0.43 per share. The storm has cost the company roughly $0.01 in EPS. FY13 EPS guidance is for 12-15% growth, or a range of $2.10-2.18, based on an annual comparable sales range of 1.5-2.5%.

Commodity inflation is expected to be 3%, lower than prior expectations of 3-5%.

The company plans to develop between 8-10 new stores in 2013, or 5% growth, having opened 10 new locations over the last 15 months.

Howard Penney

Managing Director

Rory Green

Senior Analyst