Conclusion: Shorting UnderArmour is one of our top ideas at current levels. Revenue and profit growth should decouple, and the market is likely to care. Timing matters on this one, as the company set itself up for a 1Q beat. Then we think the story should start to unfold.

This type of idea definitely gives us initial pause given that we are such big believers in the UnderArmour Brand. But the reality is that a Brand ≠ Company ≠ Stock. And in this instance, we think that the Company is at a critical crossroads to get the Brand to the next level, and that will come at the expense of the stock – at least over the intermediate term.

Since the inception of UnderArmour, the company has grown Operating Profit about in line with sales. But we think that in order to capture the three areas of growth that are critical to maintaining UA’s top line trajectory – specifically a) women, b) International, and c) footwear – it needs to step up capital investment (specifically SG&A) and dilute margins.

Let’s be clear about something, this is perfectly normal for a company going through different stages of maturation. It’s not the result of gross mismanagement in the past. Nonetheless, it is a growing pain that is apparent to us. Even if the margin dilution is only temporary, history shows us that a meaningful gap between revenue and EBIT growth creates clear multiple risk from current levels.

Let’s take a brief look at each of the three areas of growth:

1) Women: Even though less than a third of UA apparel sales go to women, the brand has arguably done a good job in marketing to female consumers compared to Nike – which took the better part of 25-years to get to where it is today (still not perfect). But the challenge with women is that the level of competition in the athletic space has stepped up so severely. Brands like Lululemon highlight not only the product quality differences that women want, but also the different way women like to shop. Go into a Dick’s Sporting Goods (where the average dude shops) versus a Lululemon (nice atmosphere, great attention to color and fit, free alterations, complimentary yoga classes). We’re not saying that UA needs to become LULU. But are simply pointing out that more brands that already have wallet share for the average women – like Victoria’s Secret – are staking their claim in this space.

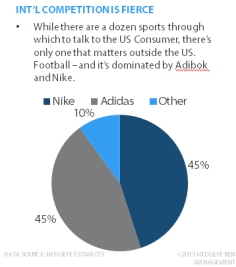

2) International: About 7% of UA sales come outside of the US today, but about half of that is from Canada. As it relates to success outside the US we’re most interested in gauging sales outside of North America. While that’s not disclosed, we think that it is around 2-3% of total sales at best. There are a few things that make growing in Europe and Asia difficult.

- Sports Differences: First off, in the US, there are around a dozen sports an athletic brand can use with which to establish a link to the consumer. There’s Football, Basketball, Baseball, Hockey, Golf, NASCAR, Soccer, UFC, Boxing , Track, Tennis, and Extreme Sports. Outside of the US, there’s pretty much one – Soccer/Football. The problem there is that Nike and Adidas absolutely dominate this sport, with up to 90% of the market fairly evenly divided between them. There are brands like Puma and Umbro that are players in the market. But breaking in here is absolutely fierce. Nike and Adidas will defend their share – violently if necessary.

- No Attachment Product: It’s difficult to establish credibility in apparel in Europe and Asia without being equally as credible in footwear (like Nike) or in Fashion apparel (like Adidas). UA has neither.

- Lack of Homogeneous Markets: In the US, it’s pretty much the same experience for both the Consumer, the Retailer, and the Brand’s Salesforce for a shopping experience in LA, NY, Miami, or Chicago. That makes the US relatively easy to sell into. But in Europe, every country is absolutely different, and even countries are vastly different based on region (think Northern vs. Southern Italy). Throw China into the mix, and it gets even more complex. The simple point is that the cost of building this business is steep.

One might argue that this means that there are growth opportunities to go along with the higher costs. We’re the first to agree. But unfortunately, costs need to come 1-2 years before the revenue is realized. That’s where we think we are today.

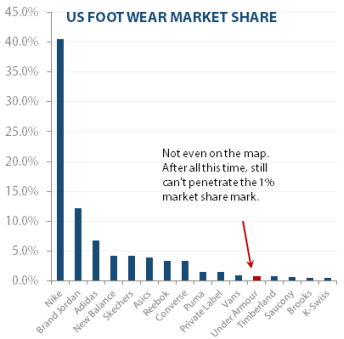

3) Footwear: For the past 3.5 years UA has had Gene McCarthy, one of the most decorated brand builders in the footwear business, running its footwear operation. But after all this time, look at the chart below…It shows US athletic footwear market share. Do you see that little red bar a couple notches behind Private Label? That’s Under Armour. After all this time, UA still cannot pierce the 1% share mark in footwear.

The problem here is that if we were to ask ten people what the single greatest opportunity is for UA over the next 3-5 years, we think that nine of them would say ‘footwear’. The bigger problem is that we asked this question 3 years ago and people still said ‘footwear’. This category has been a perennial opportunity for UA. Our sense is that only two things can unlock an opportunity. 1) leadership, or 2) capital.

We don’t think that there’s been a leadership problem under McCarthy. That leads us to think that there’s been a capital problem, and that if UA wants to succeed in this category it will need to step up its capital commitment to this area and realize a Reebok-ish 8-9% EBIT margin (leading up to the Adibok merger Reebok had share between 6-10% in any given year – and a perennial goal of 20%).

What If We’re Wrong?

A major caveat here is that our fundamental call on the margins (or decelerating top line growth) needs to be right in order for this stock call to play out. The stock is sitting at about 33x the consensus estimate for 2013. While that’s still lofty, it’s far from unreasonable for a great Brand with no debt and blue sky opportunity if it can execute on its growth plan with no hiccups (which would sustain 20%+ EBIT growth). If it is able to accelerate growth in these businesses, a 35-40x multiple on $2.00 in EPS power would not be unheard of. That’s a $70-$80 stock over 2-3 years. Definitely a nice return from its current $50. We don't think it will happen without a correction. But we need to be cognizant of plan B.

If We’re Right

If we’re right, and the market realizes that margins need to come down to sustain growth, then we could see estimates pushed back by a year, and a re-rating to something in the neighborhood of 20x EPS on $1.50. That gets us to about a $30 stock, or 40% downside, over a more compressed time frame.

A VERY Important Point On Timing

We think that UA has the wind at its back headed into 1Q (March) earnings. The company managed to get the consensus down to $0.03 in the seasonally-weakest quarter – which compares to $0.14 last year and our estimate of $0.09. We don’t want to be pressing a short into a beat – even if it is an insignificant quarter. We’d either wait until the 1Q print, or until the trading factors change and tell us to get involved sooner.