I recently read a BYD valuation downgrade by a sell side analyst based on a high relative valuation. The valuation analysis was performed using EV/EBITDA, the industry standard, and concluded that BYD's multiple of 7.6x was too high relative to the competitors at around 6.5X. This superficial analysis fails to take into account that BYD's free cash flow yield is more than twice that of its nearest competitor, when normalized for true ongoing interest cost.

EV/EBITDA fails to capture the big disparity in true borrowing costs. ASCA and PNK face refinancing risk due to maturities of credit facilities and/or bonds over the next 1-2 years. BYD, on the other hand, has no maturities until 2013. BYD's average interest rate should stay at 2% above LIBOR (assuming no covenant breaches) while the other companies will experience rates 2-3 times that rate. This is a phenomenal asset that EV/EBITDA cannot capture. ISLE is in a very similar position to BYD with no large maturities until 2013.

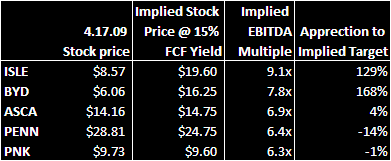

In the table below, we've calculated the implied EV/EBITDA multiple assuming a constant 15% free cash flow yield across the sector. Additionally, we've included implied target prices at those multiples. Our analysis considers true interest cost assuming credit facility amendments and extensions based on reasonable comps.

Other factors to consider:

- BYD - This FCF yield is too attractive to pass up unless you believe the company will trip its leverage covenant this year. In that scenario, BYD's interest cost would rise and its $2bn in borrowing capacity would be sharply reduced. If BYD can get through 2009, as we think it will, the likelihood of a covenant breach diminishes greatly due to the quarterly step up (a quarter turn per quarter through the end of 2010) in the maximum leverage ratio beginning in Q1 2010. BYD has a lot of levers to pull, however, including maintenance capex cuts and deleveraging bond buybacks. Based on valuation, BYD looks like the most attractive long-term play in gaming.

- ASCA - The stock looks fairly valued on FCF yield when considering the likely higher interest cost associated with refinancing its credit facility due in November 2010. ASCA is likely to hit the high yield market sometime this year and we estimate a 15% coupon. However, Q1 is likely to be a blow-out quarter and estimates should go higher. We continue to like ASCA into the Q1 earnings announcement on 4/29.

- ISLE - ISLE looks very attractive on a FCF yield basis. While the company maintains the highest leverage (7.5x) among the regionals and its competitive positioning is the weakest, ISLE does not have any material maturities until 2013. Next to BYD, ISLE may be the most attractive long-term gaming stock.

- PNK - PNK looks very similar to ASCA. Reasonable leverage but fairly valued on a FCF basis. PNK will likely be in the market to amend its credit facility which means interest cost will rise. This is reflected in our projection. The positive catalyst for PNK is also the Q1 earnings announcement. In addition to very strong earnings, PNK may scale back or delay development due to the rising cost of capital. This should be taken positively by investors.

- PENN - PENN looks fairly valued based on FCF yield. To be fair, we are assuming PENN makes an acquisition to utilize its borrowing capacity at its current bank rate. PENN is underleveraged which penalizes its current free cash flow yield. We assume almost 20% accretion to free cash flow on a $1.25bn acquisition at 6.5x EBITDA. Under this assumption, PENN's yield rises to 13%, still below our industry target of 15%. PENN is a terrific company with a great management team. However, it is the Wall Street darling of gaming right now and the valuation looks full.