This note was originally published February 14, 2013 at 12:17 in Macro

We’ve long had a skeptical eye on Socialist President François Hollande since he entered the stage in May 2012, beginning with his very loud “tax the rich” campaign slogan and lack of focus on reducing France's fiscal fat. With fears now decidedly marginalized on the dissolution of the Eurozone; no imminent threat of a sovereign needing a bailout; and Draghi’s OMT bazooka still calming markets, we return to France, the region’s second largest economy, for a closer look at the risks we see developing that may be overlooked.

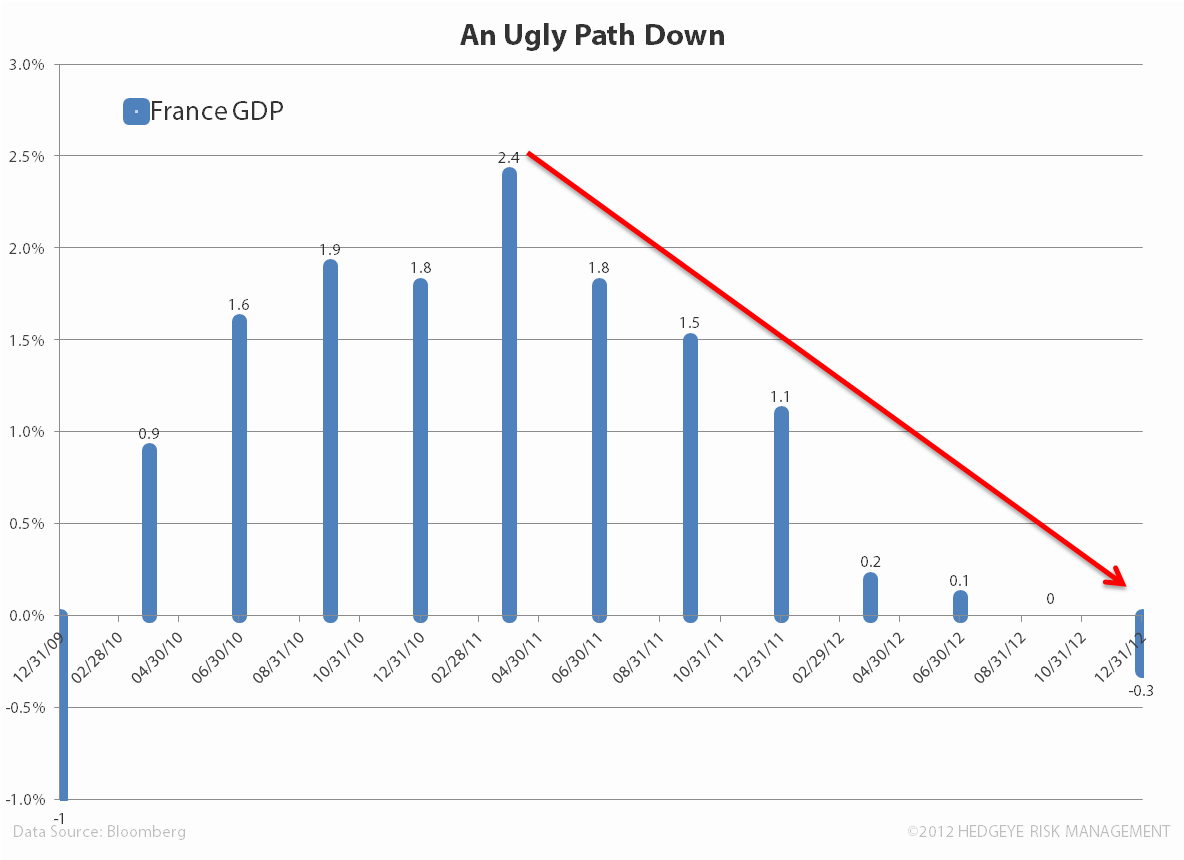

What’s mattered greatly to many investors at the country level since the “crisis” began is countries meeting or exceeding their growth targets and reducing their debt and deficit levels. France, not unlike what we’ve seen from peripheral countries since 2009, looks to miss its 2013 GDP and deficit targets. In recent days President Hollande has hinted at a willingness to change the growth forecast from +0.8% to +0.3%-0.4%, however has not backed off the deficit target of 3% of GDP. We think a revision to both is a question of when, not if.

Interestingly, the sticking point on when this change in forecast could result may have to do directly with the timing of a European Commission’s economic report on the Eurozone. It is expected to come out in late February and show that French growth should be in the +0.3%-0.4% range and that France is projected to undershoot its deficit reduction target. A recent state audit should also influence Hollande – it revealed that in a scenario of +0.3% growth, inline with current IMF projections, the deficit would be 25bps over the target, or 3.25%, and added that the state has relied too much on tax increases and needs to focus on spending cuts to attain its targets.

Beyond the Deficit Are Storm Clouds

While a miss of its deficit target may not cripple confidence in France, it adds to a perfect storm of negative trending risks, which include:

- Public debt – pushing 91% (as a % of GDP) - France is above the level of 90% that economists Reinhart and Rogoff have indicated as destructive to growth.

- Credit Rating – Fitch is the only main agency to maintain its AAA status. S&P is at AA and Moody’s at Aa1. We expect all three to be lined up at AA in 2013 and for this reduction in credit standing to weigh on its public finances, and put upward pressure on yields. Note: The 10YR is currently trading at 2.26% (versus 1.64% in Germany), and has remained stubbornly low over the intermediate term despite the risk premiums we see, a development that we believe has a high probability of inflecting in 2013.

- Competitiveness Drag – Hollande’s policy to tax the rich (75% on those making €1MM or more) is not only driving out his countrymen but sending negative investment signals to the business community. Hollande has moved the top rate of capital gains tax from 34.5% to 62.2%. For reference these levels compare with 21% in Spain, 26.4% in Germany and 28% in Britain.

- Hamstrung Spending – we believe that Hollande will not be able to issue additional spending cuts due to push back on the street against austerity. Politically, Hollande also doesn’t have the popular support to make an estimated €5B in additional cuts to attain the deficit target.

- Bank Leverage – French banks remain an outside concern due to their leverage to the periphery. While we expect Draghi and Co. to keep the union together at all costs, the weight of a still imbalanced financial sector could sway sovereign sentiment.

Economic Misses

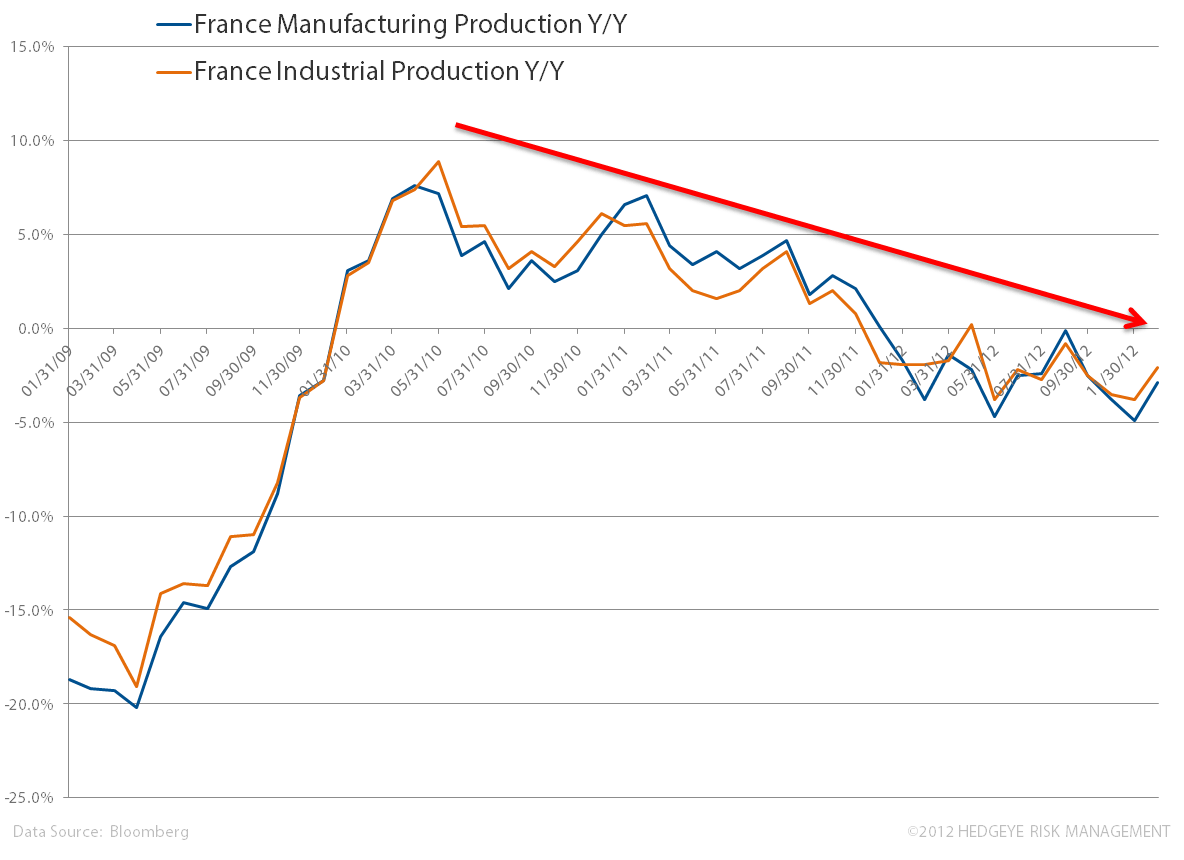

Today Eurostat reported initial GDP figures for Q4 2012. France’s Q4 GDP came in at -0.3% Q/Q versus expectations of -0.2% and +0.1% in Q3. While France outperformed the Eurozone aggregate of -0.6% Q/Q (versus expectations of -0.4%), the high frequency data that we track continues to paint a negative trend for France, one that inflects versus the larger peer economies of Germany and the UK.

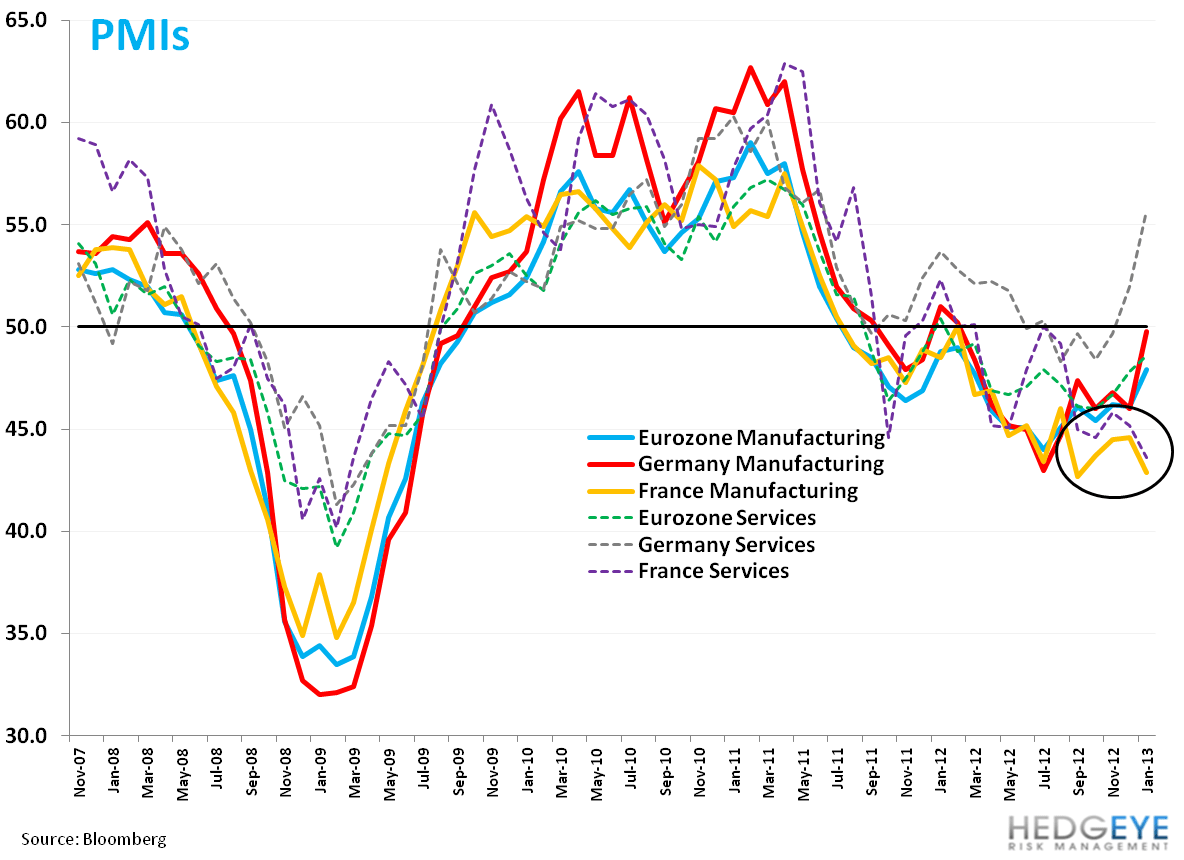

France’s PMI Services number for JAN was 43.6 JAN vs 45.2 in DEC and Manufacturing fell to 42.9 in JAN vs 44.6 in DEC, both decidedly under the 50 line representing contraction.

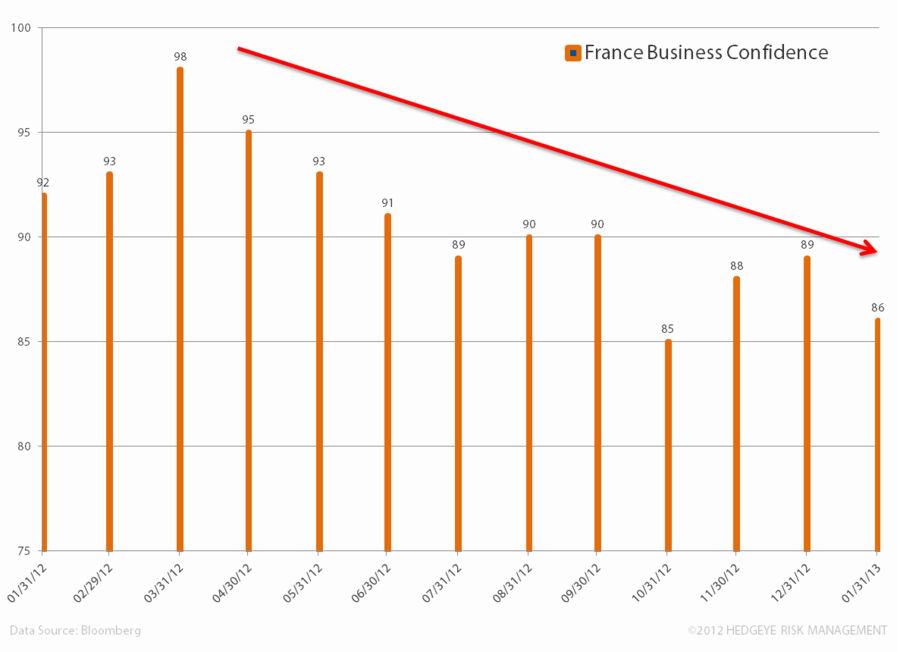

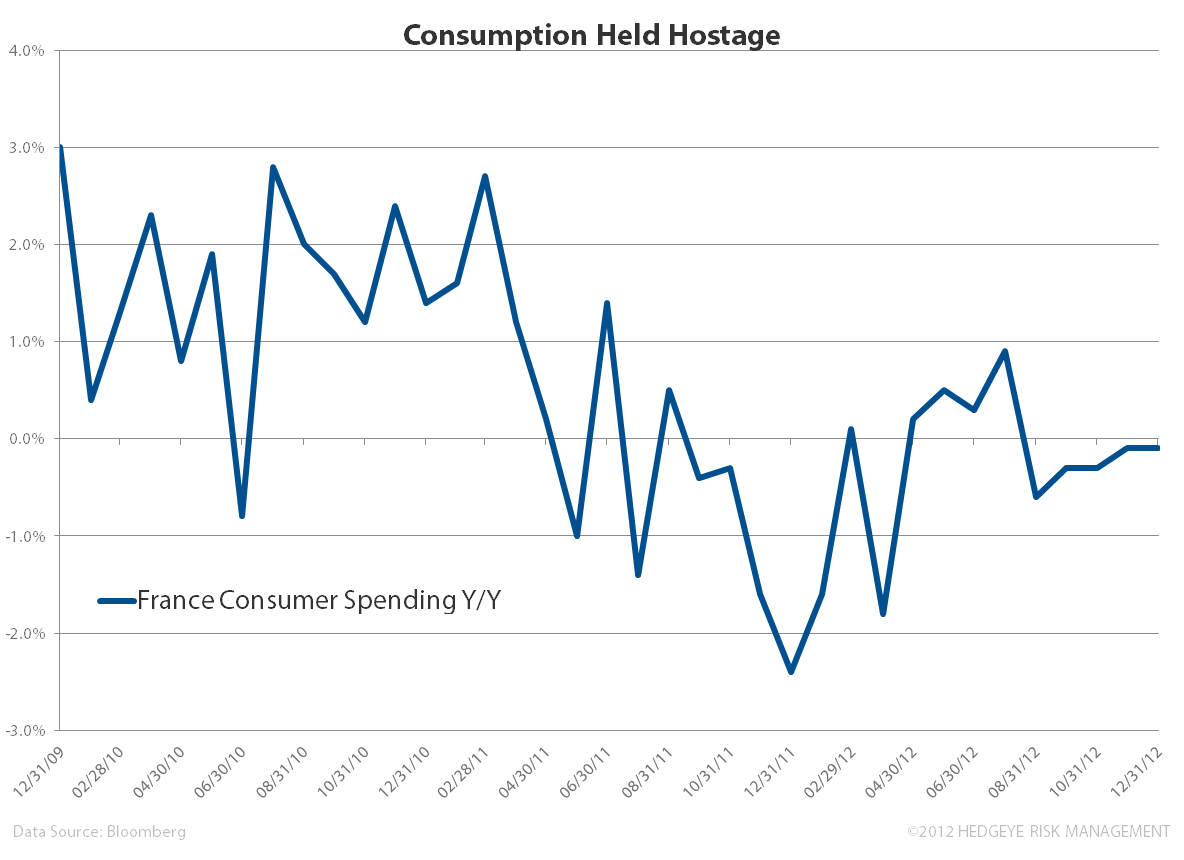

Further, the policy measures that Hollande has implemented are showing up in confidence readings. Business Confidence has rolled down the mountain since a high in March 2012, Consumer Confidence has been flat to down since Hollande’s election, and Consumer Spending has been under 1% since mid 2011 and negative for the last 5 consecutive months.

Given France debt drag, likely misses on 2013 GDP and deficit reduction, and financial and economic constrains, the country is one to watch given the downside risks. From a capital markets perspective the country has been surprisingly resilient, but this could well change. While the wave of sentiment may be more focused on the governments of Italy and Spain currently, we caution that the risks in France could drive a stagflationary set-up in the country for much longer than is currently being priced in. We think the Hollande’s political handcuffs will prevent necessary spending cuts and his decidedly anti-business tax policy will chase good money out of the country. Stay tuned.

Matthew Hedrick

Senior Analyst