“If it’s your job to eat a frog, it’s best to do it first thing in the morning. And if it’s your job to eat two frogs, it’s best to eat the biggest one first.”

-Mark Twain

My Hedgeye mates and I have been over in London for almost half a fortnight. Meeting with European investors and getting entrenched into the British culture has been an interesting experience for us. To be fair, we probably have spent a few more quid at the pub then we would in a normal week, but even that seems to be part of the culture over here.

Since being in the U.K., we have learned a few bits and bobs, and also some new phrases. The most interesting one to me is, “box of frogs.” It is actually used to describe a crazy state of mind, such as: that Keynesian economist is as mad as box of frogs. The point being that if frogs were placed into a box, it would drive someone crazy if they had to hold onto the box. The parallels to our frustration with global monetary policy are quite evident.

I’ve also taken up reading the Irish Times when I have had a break for coffee and biscuits during the day. While I can’t say I totally understand rugby, the hockey player in me obviously has some affinity for the sport. This morning in the Irish Times the Rugby Analyst Liam Toland wrote the following:

“Yes, I was enthralled by England’s application, their maturity, their discipline, and their ever growing belief in negotiating a tough fixture. That’s why I stayed. Remember not so long ago, these guys were throwing dwarfs around.”

I’ve heard, and frankly overused, many sports analogies in my days, but “throwing dwarfs around” is a new one even for me. I’ll have to ask one of the blokes on our restaurant team, Rory Green, about that one.

On a serious note, the trip to London was very fruitful in terms of gauging expectations. Over the course of the week, we probably met with well over 500 billion sterling in cumulative investor capital. From a philosophical perspective, many of the money managers in London describe themselves as thinkers, especially as compared to the traders in New York and Connecticut. And from our view, they are a very thoughtful and strategic group.

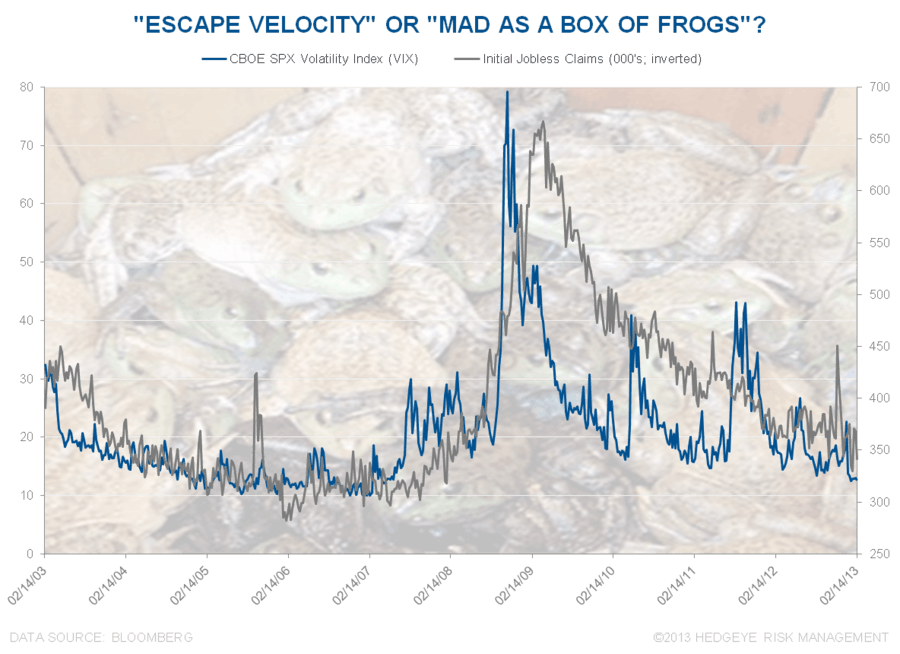

Interestingly enough, we may actually be entering an environment in which thinking is rewarded more than trading. This is certainly not to say thinking is a better risk management strategy per se, but rather that we are in a new environment of low volatility. In the Chart of the Day we actually look at the VIX over the past five years. The interesting point to note based on our models is that upside resistance is what was for the past three or more years the point where we recommended shorting and/or selling stocks (right around 14).

The implication is simply that based on the VIX, it looks to us we may actually be entering a new and lower phase in volatility. This supports our bullish case on U.S. equities, especially if the VIX breaks through its year-to-date lows. In that scenario, our models have the VIX going to 9. This would obviously be a very favorable tailwind for equities, and really risk assets generally. Not so favorable, though, for the end-of-the-world, such as long Treasuries and gold.

A key question many of the asset allocators in Europe are asking us is in regards to what regions of the world we are most favorably disposed to, or vice versa. For us this is less an exercise of whetting our fingers and sticking them up to see which way the wind is blowing, but rather just a function of what our models are telling us. As it relates to countries specifically, we focus on growth, inflation and policy. Our views on some of the key economies are as follows:

- The U.S. economy – The U.S. is currently in Quad 1, which means growth is accelerating, or poised to accelerate, and inflation is decelerating;

- The Chinese economy – China is currently in Quad 2, which means that growth is accelerating with inflation also accelerating.

In terms of being long equities, an investor wants to live in Quads 1 and 2.

Interestingly enough, Europe is actually also currently in Quad 1, albeit growth itself is stabilizing at very low rate in Europe and it is a continent, as usual, with very distinct potential by country. One of the most negative countries being flagged in our models currently is France, the regions second largest economy. (And no, Box of Frogs was not a reference to France!)

One of the lads on our Macro Team, Matt Hedrick, knows his onions as it relates to European economies and emphasized the key risks to France in a note yesterday. Some of the key negative trends include:

- Public debt – pushing 91% (as a % of GDP) - France is above the level of 90% that economists Reinhart and Rogoff have indicated as destructive to growth;

- Credit Rating – Fitch is the only main agency to maintain its AAA status. S&P is at AA and Moody’s at Aa1. We expect all three to be lined up at AA in 2013 and for this reduction in credit standing to weigh on its public finances, and put upward pressure on yields;

- Competitiveness Drag – Hollande’s policy to tax the rich (75% on those making €1MM or more) is not only driving out his countrymen but sending negative investment signals to the business community. Hollande has moved the top rate of capital gains tax from 34.5% to 62.2%. For reference these levels compare with 21% in Spain, 26.4% in Germany and 28% in Britain;

- Hamstrung Spending – we believe that Hollande will not be able to issue additional spending cuts due to push back on the street against austerity; and

- Bank Leverage – French banks remain an outside concern due to their leverage to the periphery.

The research in this instance also supports the price as the CAC is broken in our quant models. It is not totally surprising either, as some of the government policies in France seem a little dodgy.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, and the SP500 are now $1, $117.21-118.92, $80.04-80.77, 92.71-94.48, 1.96-2.05%, and 1, respectively.

Enjoy your weekends and if you want to talk Europe, feel free to give us a bell.

As always, keep your head up and eyes on the blindside of the pitch,

Daryl G. Jones

Director of Research