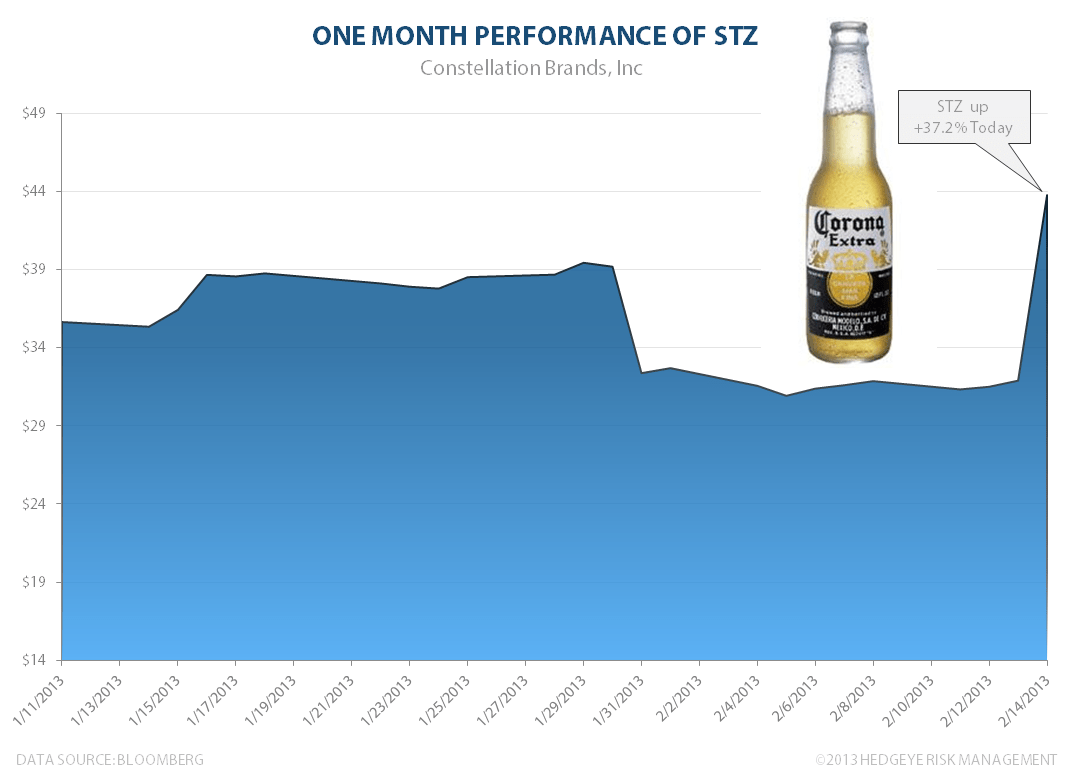

Constellation Brands (STZ) closed up +37.2% today after news that it won full control of the Corona and Modelo brands after Anheuser-Busch InBev tried to salvage its deal to buy Grupo Modelo that was initially blocked by the Department of Justice. Constellation brands will become the third-largest brewer and seller of beer to U.S. consumers.

Back on January 31, 2011, Hedgeye Consumer Staples Sector Head Rob Campagnino noted that STZ had the potential for further upside per the Modelo deal. Said Campagnino:

"Our view remains consistent – this transaction represents significant value to ABI, and therefore we believe that additional concessions are very likely.

While the move down is painful, we continue to see substantial value to Constellation Brands should the transaction close, an event that we continue to see as likely, though delayed."