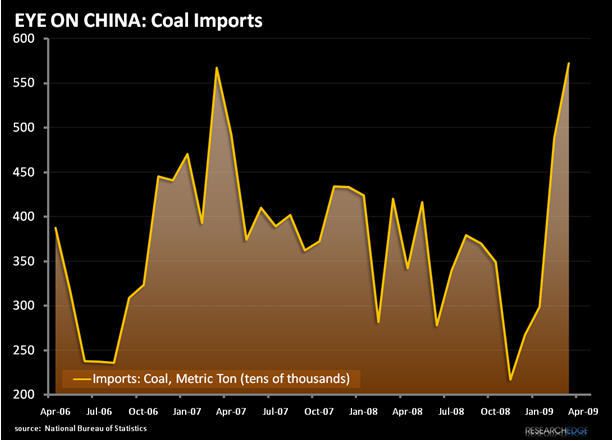

The market for coal in China suggests buyers are anticipating a big increase in power demand

At -4.6%, Chinese PPI for March arrived at the lowest year-over-year change in a decade as contracting demand for exports and lower commodity prices impacted the cost of doing business.

One core commodity component that has still seen double digit inflation levels is coal. Since becoming a net importer last year the PPI breakout has remained in double digits despite global price declines with February data (the most recent available) registering at 18.3% Y/Y.

March imports registered at the highest level in two years, and the divergence between spot prices in China have held at price levels significantly higher than global averages since the end of last year, with some data showing a 50% premium to European and South American prices.

Chinese coal producers’ experienced significant setbacks last year with massive snow storms and the Sichuan earthquake interrupting operations and transportation, while at the same time government programs to modernize the industry and close antiquated, unsafe mines have trimmed capacity. The persistent demand for Thermal coal in the face of the Q4/Q1 Industrial production slowdown and sequential Y/Y declines in reported electric power production over the same period however, would appear to be more than enough to offset these capacity setbacks. This continued rapid demand expansion suggest something that may be significant for our thesis: stockpiling by utilities in expectation for rapidly increased electricity demand for the remainder of 2009 as a stimulus fed recovery picks up steam.

We remain bullish on the ability of China to kick start internal demand with the stimulus measures adopted and will continue to monitor all factors looking for more data to support or challenge our thesis.

Andrew Barber

Director