Growth Accelerates Notably in January

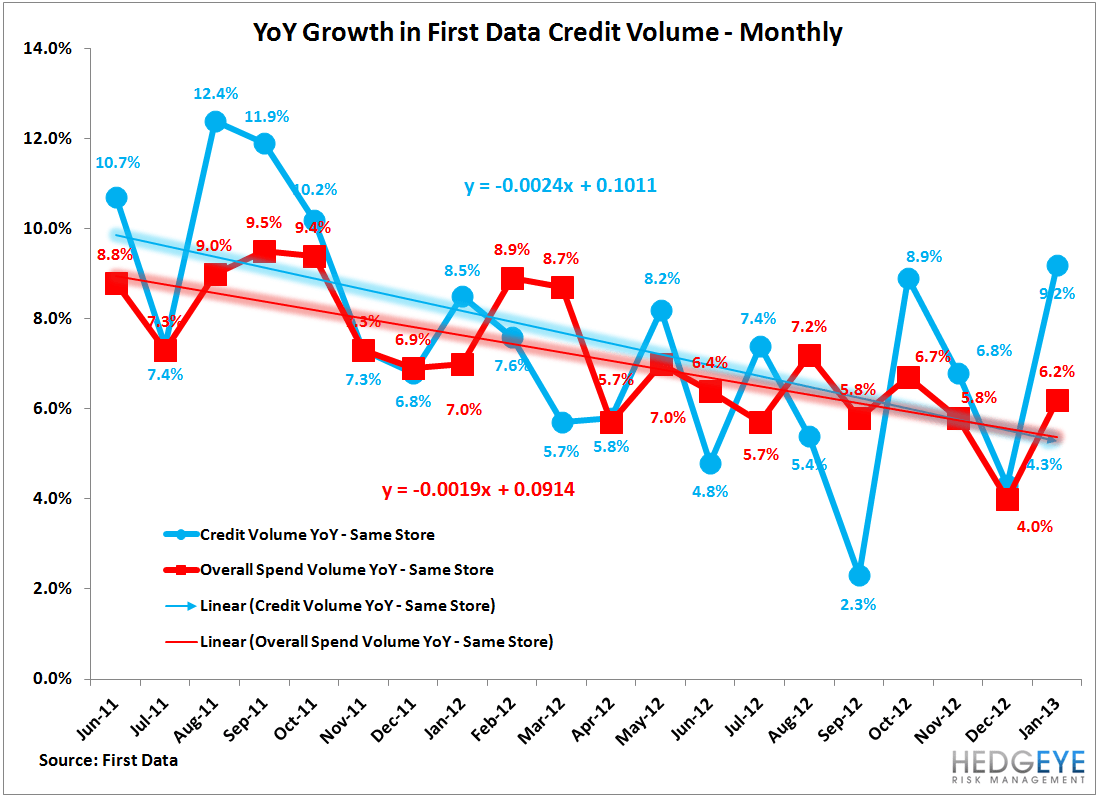

First Data released its January SpendTrend data this morning, which tracks aggregate same-store sales activity in the United States. January showed notable acceleration in credit card volume growth to +9.2% YoY vs. +4.3% YoY growth in December and +6.8% YoY growth in November.

On an overall basis, including credit, debit and check, consumer spending volume growth in January also accelerated to 6.2% YoY, which was up from 4.0% in December and 5.8% YoY growth in November. January's 6.2% YoY growth was, in fact, in-line with the average rate of growth over the last 8 months of 2012.

FirstData flagged the following components as notable contributors to the strength of January's print:

Retail dollar volume growth was the highest growth seen since August 2012. Dollar volume growth in building material & garden equipment & supply dealers and sporting goods, hobby, book & music stores were key contributors to the retail growth.

There also seems to be a bit of time-shifting going on, as consumers deferred some consumption in December over fiscal cliff apprehensions into January. Nevertheless, it's notable that the payroll tax increase as well as the tax increase on high earners appeared to have little impact on consumers' appetite for spending.

We like to use SpendTrend data as a proxy for American Express' intra-quarter momentum. Amex didn't provide a January update, as they normally do, on either their 4Q12 earnings call or at their recent investor meeting. Based on the historical relationship between FirstData's credit volume and Amex' U.S. credit volume, we would expect that January's growth in billed business for U.S. card accelerated to 9.5%-13.3%, up from the 4Q12 growth rate of 6.9%. If this is sustainable, this would support multiple expansion. The stock is currently trading at 13x 2013 estimates. This is the low end of the range (13x - 14.5x) over the last twelve months.

It's also interesting to consider that Amex' international volume growth accelerated meaningfully in 4Q12 to 8.8%, up from 2.7% in 3Q12. With both U.S. and International now accelerating, and the benefits of cost cutting materializing, the company is in position to generate upside surprise to estimates (if they choose to let it flow through).

Our primary concern on Amex had been that the combination of tax hikes on its top tier clients coupled with higher payroll taxes on all its clients would suppress spending meaningfully. That, however counterintuitively, appears not to be happening.

Joshua Steiner, CFA