This note was originally published at 8am on January 29, 2013 for Hedgeye subscribers.

“The world is not the way they tell you it is.”

-George Goodman

That’s easily one of the top opening sentences to any book in my library (The Money Game, by George Goodman). And oh how true does it ring about the game so far in 2013.

You see, so far 2013 is all about you. “You – your identity, anxiety, and money” – that’s what Goodman (under the pseudonym of “Adam Smith”) titled Part I of Chapter 1 in 1968. So what I am about to write this morning is not new. It’s just put another way.

“The successful investors I know do not hold to the way it ought to be, they simply go with what is.” (page 19)

Back to the Global Macro Grind…

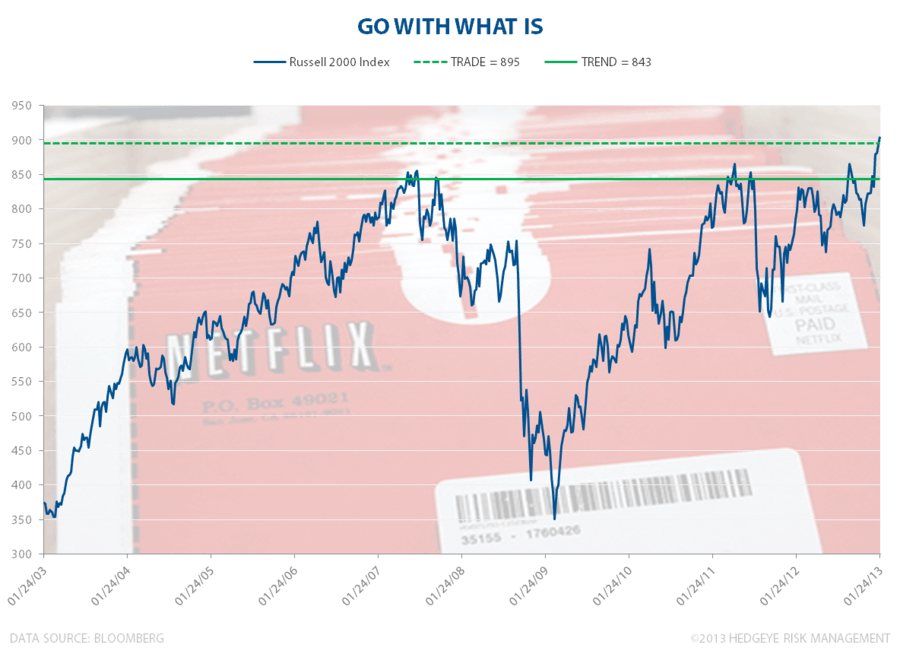

Now maybe people write these sorts of things at all-time highs in markets (the Russell2000 made another all-time closing high yesterday at 906 = +6.7% YTD). Maybe they write them at the lows too. I’d just as soon as think about them all of the time.

One way to contextualize behavior is by using math across multiple-factors and durations. Internally (and at hedge funds I have built and traded portfolios for), we call them STYLE FACTORS.

If you punch in style factors on either Amazon or Wikipedia, you’ll get a promo for the “Otterbox Commuter Series Hybrid Case” (iPhone4) or something about the “Seven Factors of Enlightenment” (Buddhism). So, while I think most quantitatively oriented risk management platforms consider these factors standard, they are far from Jeremy Siegel’s view of portfolio theory.

Style Factors are what are moving your portfolio now – here are some big ones that are outperforming YTD:

- High Short Interest = +6.8% (outperforming low-short interest stocks by almost 1%)

- High Beta = +8.1% (outperforming low-beta by over 4%)

- High Debt/EV = +7.0% (outperforming low-debt/EV by 60bps)

I can also slice and dice your portfolio across geographic, sector, and size (market cap) factors. And I do for our clients who ask us for this custom advisory and risk management work, but for your general reading purposes this morning I guess the bottom line is to take my word for it – it works.

Why does it work? Particularly when you overlay it with a multi-duration (TRADE/TREND/TAIL) price/volume/volatility model, it basically tells you what the machines are chasing. If you can front-run the machines, you are one step ahead of your competition. And that may not sound like what we all learned at school, but it’s the way that today’s game is.

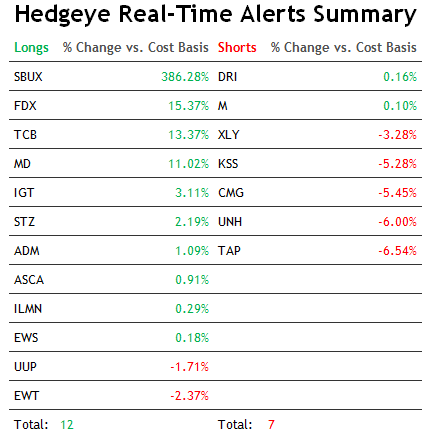

If you own something like Netflix (NFLX):

- You are long High Short Interest

- You are long High Beta

- You are smiling

Combined with a little storytelling from the management team and a catalyst on top (the recent quarter and conference call), that makes for a tasty YTD return. It also drives the fundamentalist who thinks the stock is “expensive” right nuts.

“If thinking of this fascinating, complex, n-person process as a Game helps, then perhaps that is the way we should think. It helps rid us of the compulsions of theology.” (George Goodman)

In other words, don’t play the game you want – play the game that’s in front of you. Modern day math, machines, and real-time signals help augment your go-to-moves. They also help you realize when it’s a good time to just get out of the way.

Yesterday was the 1st down day in the SP500 in the last 8 trading days. Within minutes of the market going down, my contra-stream (I built it on Twitter for my own behavioral observation) lit up like we were about to see the apocalypse. *Note: we didn’t.

I’m as leery about buying high as anyone, but through making many mistakes I’ve taught myself to use the risk of the range (within the context of all aforementioned factors) as my guide instead of my gut.

For the SP500 itself, here are some important Risk Ranges to contextualize and consider:

- SP500 = Bullish Formation (bullish TRADE, TREND, TAIL) with immediate-term TRADE support at 1488

- S&P Sector Studies = all 9 are bullish TRADE and TREND for the 17th day out of the last 18!

- US Equity Volatility (VIX) = Bearish Formation with a Risk Range of 12.04-14.36

In other words, go with what is, until it isn’t. The high-probability hand you keep playing is that US stocks make higher-highs as equity volatility makes lower-lows. If and when that changes (it will, and maybe abruptly), Mr. Market will let you know.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr yield, VIX, and the SP500 are now $1651-1676, $112.28-114.62, $79.61-80.14, 89.69-91.14, 1.89-2.01%, 12.04-14.36, and 1488-1510, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer