What's New?

Yesterday afternoon, the government of Venezuela announced that the fixed exchange rate would change from 4.30 bolivars to the dollar to 6.30. The move was widely expected, even if the magnitude of the devaluation was unknown.

A number of companies across consumer staples have exposure to this event, and we attempt to provide investors some perspective based upon the prior 2010 devaluation (100% devaluation vs. nearly 50% yesterday). The exposure is two-fold – the one-time revaluation of monetary assets in the country will result in a charge, and then an ongoing flow through the income statement where any income earned in Venezuela is translated back into fewer dollars.

A look back at 2010

Back in January of 2010, the Venezuelan government announced its decision to devalue its currency and the official exchange rate went from 2.15 to 2.60 for essential goods and to 4.30 for non-essential goods – the lower rate was abolished in December that same year.

What happened and to whom?

CL - took a significant charge ($271 million, or $0.53 per share) as a hyperinflationary transition charge in 2010, as well as the impact of bolivars translating back into fewer dollars flowing through the income statement. The company also has a significant local currency asset position ($200 million as of end of year 2010).

ENR - took a $0.20 per share charge ($0.03 in ’11) for the devaluation, on an earnings base of $5.60. The combination of the devaluation and economic conditions in Venezuela resulted in a $23.3 million reduction in net sales in ’11, on a base of approximately $4.25 billion.

AVP - took a $81.0 million charge to EBIT in ’10 (on a base of $705.5 million) as well as a $46.1 million charge in “Other expense, net”. Venezuela represents approximately 5% of AVP’s revenue and 8% of operating profit (first nine months of ’12). Further, AVP had $223 million in cash balances denominated in bolivars (total cash on the balance sheet as of September 30, 2012 was $1,095.5 million).

KMB - took a $96 million charge in Q1 2010, net investment (as of year-end 2010) was $175 million. Venezuela represented 1% of net revenues and 1% of EBIT.

GIS – (from 2010 10K) - “During fiscal 2010, Venezuela became a highly inflationary economy, which did not have a material impact on our results in fiscal 2011 or 2010.

K – (from 2010 10K) – “Venezuela represents only 1-2% of our business; therefore, any ongoing impact is expected to be immaterial.”

HNZ – (from 2010 10K) – net asset position of $81 million (subsequent to the 2010 devaluation) –“While our future operating results in Venezuela will be negatively impacted by the currency devaluation, we plan to take actions to help mitigate these efforts. Accordingly, we do not expect the devaluation to have a material impact on our operating results going forward.”

KO – (from 2010 10K) – “During the first quarter of 2010 we recorded a loss of $103 million related to the remeasurement of our Venezuelan subsidiary’s net assets.” As of December 31, 2011, the company’s Venezuelan subsidiary held monetary assets of $300 million.

PEP – (from 2010 10K) - “In 2010, our operations in Venezuela comprised 4% of our cash and cash equivalents balance and generated less than 1% of our net revenue”.

MJN – very small business there resulted in an $8.5 million loss over the initial balance sheet remeasurement.

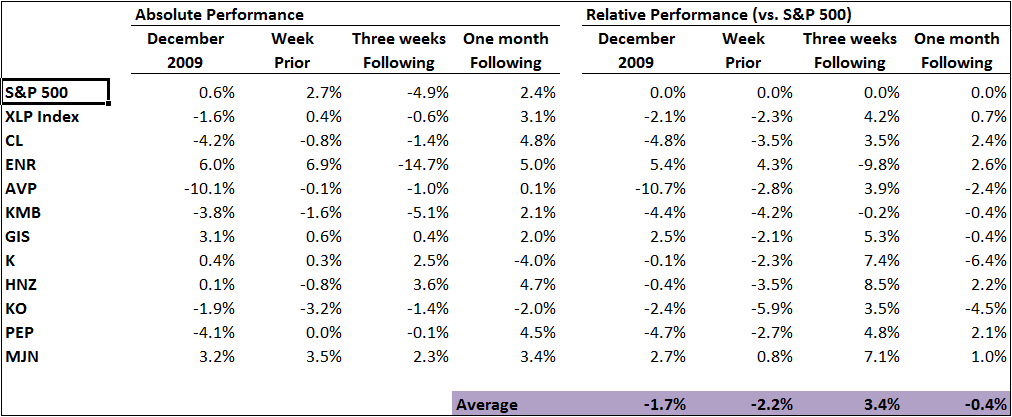

In order to assess how the stocks might trade, we took a look at the absolute and relative performance of the names mentioned above versus the S&P 500 and the XLP Consumer Staples Index for the month before the devaluation (December 2009), the week before (devaluation occurred on January 8, 2010), the three weeks following (until February 1, 2010) and then the next month (from February 1 to March 1). Both the prior month and week before saw meaningful underperformance versus the S&P, that was substantially made up (on average) in the three weeks following.

It appears to us that the setup is a little different coming into this event, as the names mentioned above outperformed the S&P 500 by an average of 2.0% over the last month. Also recognize that the magnitude of the devaluation is substantially less than 2010.

Bottom line for us is that the companies with significant exposure (AVP, CL, PEP, and KO) may see some very, very modest EPS weakness and almost certainly more significant one-time charges as a result of this event.

For those folks in the Northeast - happy and safe shoveling!

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst