Bulls and bears don’t agree on much with JCP, but they probably would agree that the trajectory of the company’s top line is the base-line of success or failure. Even bears focused on (a compelling) liquidity case need to agree that liquidity is not an issue if top line shows up to the party.

That said, we find it surprising that in most discussions we have on JCP (both bulls and bears) the comp assumptions people use are often seemingly pulled out of thin air.

We concur that no one has a crystal ball on comp trends, including us. But the reality with JCP is that we have enough pieces of the puzzle to come up with an algorithm for how aggregate sales per square foot should change simply as higher-productivity shops are layered in over the legacy layout.

When we go through the math, our model suggests the following results:

There are some important modeling variables:

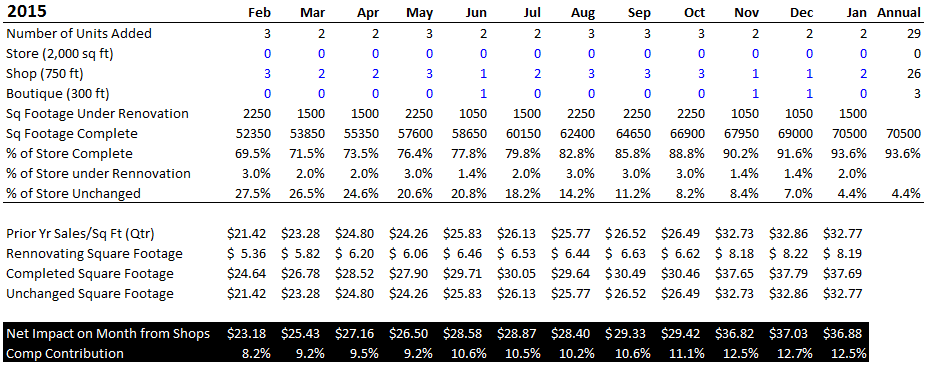

1) JCP end this year with 9 shops, adds 30 next year, and then evenly weights the remainder through the end of 2015.

2) JCP touches 75,000 square feet, or about 69% of JCP’s total.

3) Out of the 100 shops, there are a) 3 ‘Stores’ which measure 2,000 feet, b) 85 ‘Shops’ at 750 feet, c) 12 ‘Boutiques’ at 300 feet, and d) a town square at 2,000 feet.

4) Shop additions are timed by month such that JCP maximizes its floor space during peak times of year. For example, during September and October 3-5% of the stores will be under construction, but only 1-2% will be renovated during holiday periods.

5) As it relates to productivity, we assume that…

- For the full quarter stores under construction, that productivity get cut by 75%. While the space is being worked on, there is actually zero productivity, but on the flip side it is not usually closed down for a full quarter.

- Square footage that is altered gets a 15% comp lift. Remember that out of the eight shops opened thus far, there’s been just over a 30% lift. But this is far from uniform. One space went from $69/ft to $207/ft. Another went from $93 to $160/ft. But you don’t need to be a genius to figure out that to have this kind of productivity change and average out at only 32% in aggregate, there had to be a couple of stinkers bringing down the average. Fortunately, those are the JCP branded shops and Arizona – two incumbents at JCP where the company mis-executed on fashion. From our perspective, we’re not too concerned here. We’re more excited to see the impact of shops from brands that will do the merchandising along with JCP – brands such as Nike, Giggle, Carter’s, Joe Fresh, Martha Stewart, Tourneau, and Bodum. We don’t think it’s too great of a stretch by any means for us to model a 15% lift with concentrated efforts by brands like this coming on.

- Unaltered square footage comps at zero, BUT…

- We add a ‘dysfunctional pricing’ quotient, which allows us to adjust the comp down for a good part of the next year while the company figures out its pricing strategy. Note that our model assumes that the negative impact that we’ve seen – and should continue to see in 2013 – ultimately goes away, but never reverses course and helps the model on the positive side.

6) We know that this might seem like a completely ridiculous exercise today given that the topic du-jour is how the company can prevent using its credit line, defaulting on debt and continue store roll outs while it is comping down 35%. Bears will immediately come back and say that if sales trends persist, then store rollouts need to slow, or halt -- which is a game changer. But if the company can pull through, fund its expansion, and execute on its shop-in-shop strategy as outlined in this model, the math tells us that we could be looking at positive comps in mid-2013, mid-single digit comps throughout 2014, and low-double digit numbers by the end of the rollout.

Again, we appreciate the heated debate on this name, and concur that that there’s a lot that could go wrong (remembering that we were bearish with the stock in the $30s). But regardless as to where you stand on this one, let’s continue to flush out the facts, and keep the debate alive.

Call with any questions.

Brian

Here’s the math behind our ‘shop-in-shop’ accretion analysis.