McDonald’ is set to release January sales tomorrow before the market open and, while management already guided to negative global comparable sales, we will be watching for any indication of how respective markets and menu items are performing in the respective geographies.

Since the company reported FY12 results recently, we will keep this note brief. McDonald’s shares have been performing strongly of late but lag the S&P 500 over the past week as we move close to January sales being announced. We remain convinced that the Street’s projected acceleration in earnings in 2013 is overly optimistic and would avoid buying the stock at these levels.

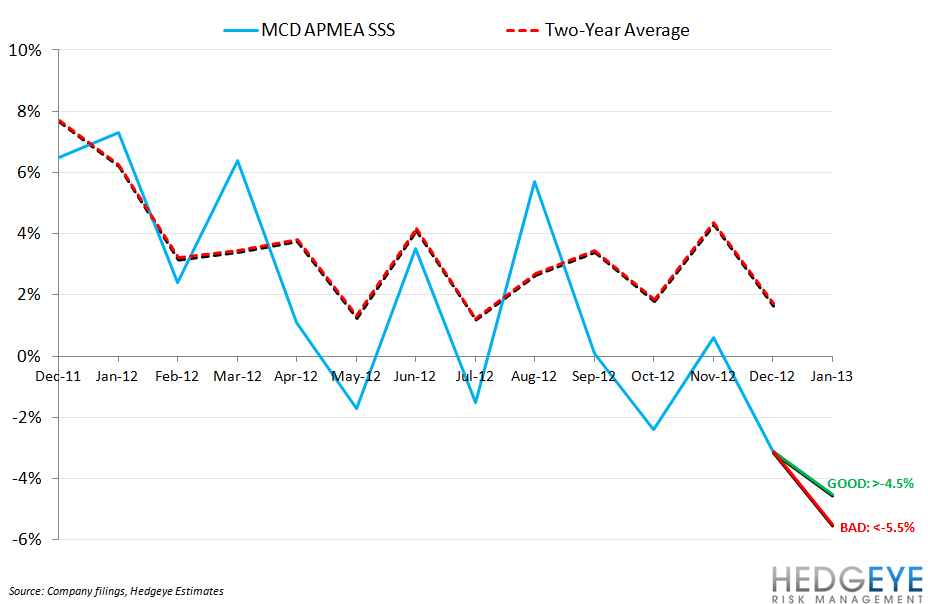

The charts below illustrate what we believe the investment community will perceive as good, bad and neutral results for the US, Europe, and APMEA January sales.

Howard Penney

Managing Director

Rory Green

Senior Analyst