Co-chairman/founder’s Eisenberg and Feinstein sold 2.15 million shares on 4/09, the largest sale by insiders over the past five years. The shares represent approximately 20% of their direct and indirect holdings, not accounting for any options. The absolute number of shares is eye-opening by historical standards – even though the entire amount was sold by their trusts with a lesser portion sold by their charitable foundations. Additional executives, including the CEO, also reported sales resulting from option exercises that were all slated to expire by the end of this year.

Overall, the 13 insiders retain a 4% position in the company, making them the 6th largest holders of company shares.

Alright, let’s face some facts. I’m never thrilled to see that level of sales activity. If they are selling, then why should I buy? There are three reasons I’m not overly concerned about the activity.

1) The stock doubled over four months and is up 60% in 6 weeks. If I were them I might sell some stock too.

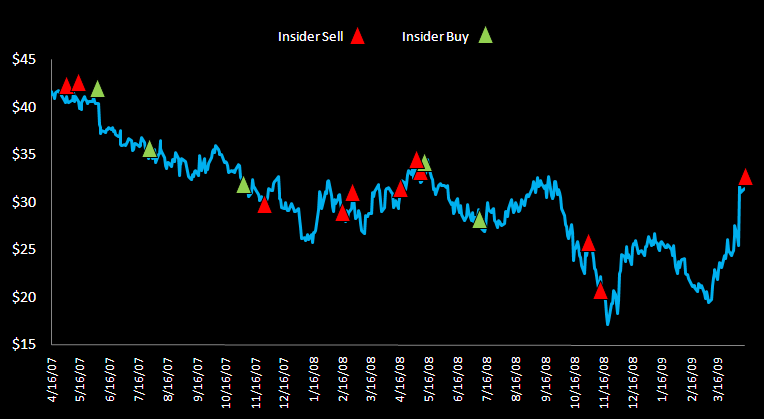

2) History suggests that management has not been particularly good with timing of stock trades (see chart). It’s a good thing that they manage retail stores instead of portfolios.

3) Lastly, and most importantly, BBBY management, like most management teams I know in Consumer, does not ‘do macro.’ These guys are basing their forecasts on bottom-up models with a loose macro beacon set by Wall Street research. Based on the collective work of our industry and Macro teams, we think that the softline retail supply chain will have a tailwind for much of the next year. I don’t think that management appreciates that yet. See our recent research on the topic for more color.

Latest Insights