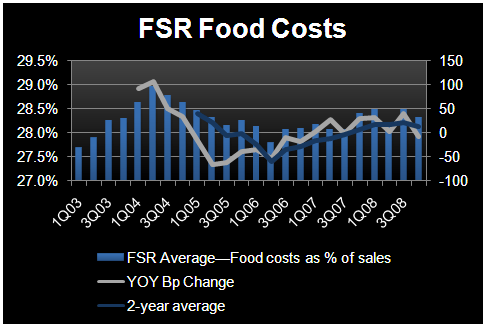

Tracking commodity and labor cost trends is even more important as casual dining companies continue to beat EPS expectations on better margin performance. With top-line trends remaining weak (Malcolm Knapp reported last week that March casual dining same-store sales declined 4.9% with traffic down 6.5%), restaurant operators are focused more than ever on cost management. Although slowing new unit growth and a renewed focus on operating more efficiently have allowed restaurant operators to cut costs, the YOY roll over in commodity costs has been a necessary component of recent margin and earnings outperformance within casual dining. During the fourth quarter, average full-service restaurant (FSR) food costs declined as a percent of sales on a YOY basis for the first time since 3Q07 and declined the most they have since 4Q06. For casual dining margins to continue to improve, it is necessary that commodity prices remain a YOY tailwind in Q1 and Q2 as Q1 same-store sales on average fell 4.3% (according to Malcolm Knapp), and I don’t think we will see a significant improvement in Q2 sales trends from the -3% to -5% levels.

Despite the food cost favorability in Q4 for casual dining companies, QSR companies on average have seen their food costs as a percent of sales increase for seven consecutive quarters. QSR margins have been somewhat insulated from these commodity increases as sales have held up relative to casual dining, but QSR average EBIT margins have started to roll over, posting YOY declines for the last three quarters. This seems less bad when compared to the 17 consecutive quarters of YOY EBIT margin declines posted by the FSR industry on average. Casual dining sales are still declining, but they have improved on the margin, with the Q1 same-store sales decline of 4.3% being better than the 6.0% decline in Q4. As I have said before, these marginally better casual dining sales will take market share from the QSR industry so QSR margins may be less protected from commodity cost variability.

That being said, food costs remain rather favorable on a year-over-year basis with only two commodities (chicken and pork) currently up on a YOY basis. Even chicken prices, which are up 4% YOY, are trending down recently and are down 2% year-to-date. Cattle prices, on the other hand, are still down 1% YOY but have moved up about 5.5% in the last two weeks and are up nearly 4% YTD. Both soybean and gas prices are still extremely favorable on a YOY basis, down 22% and nearly 40%, respectively, but they have recently increased rather significantly. Soybean prices are up 13% in the last two weeks and gas prices are up 27% YTD.