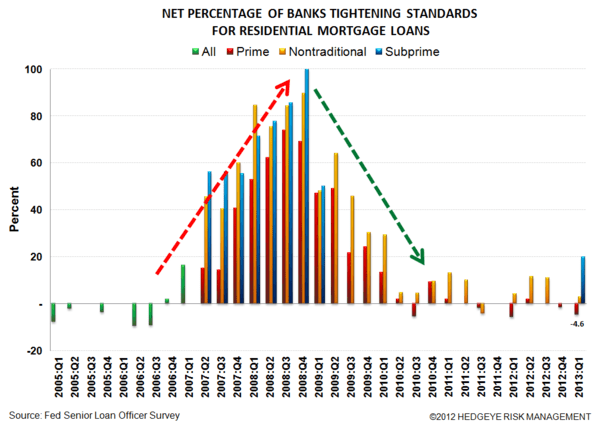

New data shows that banks are easing their standards on prime residential mortgage loans. On balance, 4.6% of banks reported flat to lower standards on prime residential loans, up from 1.6% last quarter. This means that banks are willing to lend to more borrowers as they ease credit standards and that is a positive for the housing market, which is already in the midst of recovery. We are also starting to see subprime loans come back into the picture, albeit not fully yet.

On the demand side, borrowers are showing plenty of interest in mortgages. The first quarter of 2013 marked the sixth consecutive quarter of banks reporting quarter-over-quarter growth in prime residential mortgage demand. Naturally, much of this is refinancing demand.