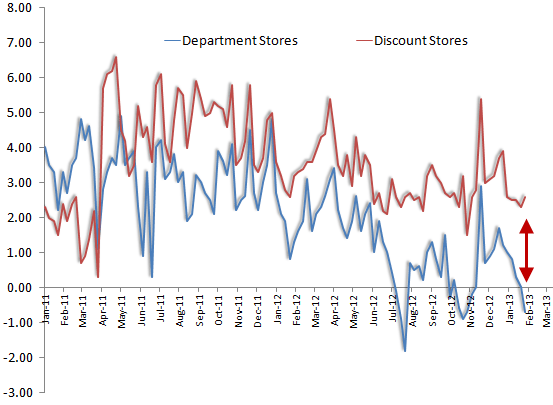

Here’s a nugget for you in advance of Same Store Sales on Thursday. The spread in the growth rate between Discount stores and Department stores jumped by a full point in the final week of January to 3.3%. That marks only the fourth time since October 2011 where this spread was greater than 3 points. For the latest week, Discount Stores grew 2.6% per the Redbook Index, while Department Stores contracted by 0.7%.

Expectations for same store sales in January seem to be universally upbeat. That makes sense to us on the Discount Store side, and perhaps in areas that were helped by the cold weather snap in January. But otherwise, the data is hardly overwhelming.

Johnson Redbook Index: Discount Store Sales vs. Department Stores