While I’ve gotten quite bullish on the US retail supply chain, it’s tough for me to say the same about just about any part of Europe. That said, I’m not going to turn a blind eye to data points that suggest that just maybe we’re in the process of hitting bottom.

Several indicators suggest a less bearish trend… the Consumer Confidence report, Consumer Credit Lending, Consumer Household Goods Consumption, and M&S results (Marks and Spencer).

The Consumer Survey for UK Spending Confidence on Household Goods is still ugly by most measures, but marked a bottom in January and has risen moderately over the past two months.

The single largest move in the “Good time to buy” index occurred between November and December of 2008. Consumers’ access to credit seems to have found a bottom in the same time period.

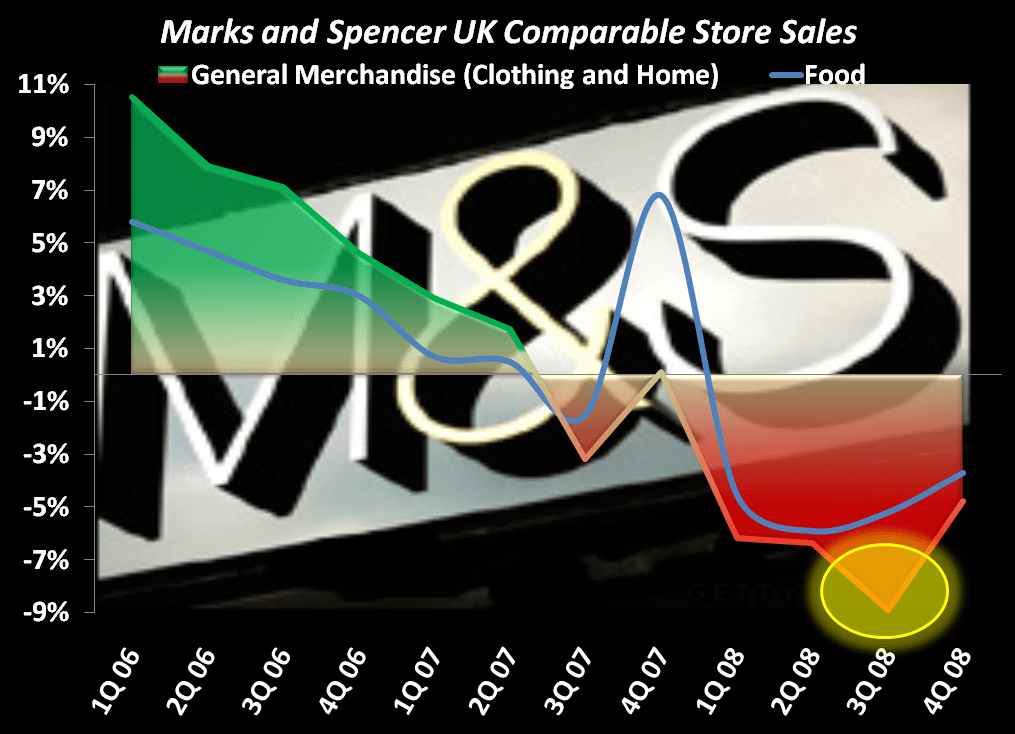

M&S did better than bad with UK sales down 0.3% and same store sales down 3.7% in Food and 4.8% in Clothing and Home.

I’ll go to the mat with anyone that tries to label me a UK bull. But lining up the factors above can’t be ignored.

Zach Brown

Research Edge